Weaponized Risk Models

How pod shops and quants turned risk management into a profit center

By: Daniel Rasmussen, Chris Satterthwaite, and Lionel Smoler Schatz

For most investors, risk management conjures images of risk-averse, neurotic bureaucrats. But that image is out of date. Today, risk models have become the key weapon in the arsenal of the apex predators of the hedge fund world. For pod shops and quant funds, they are the central nexus through which capital allocation is coordinated across strategies, assets, and asset classes.

Both pod shops and quant funds use risk models to neutralize unwanted risk factor exposures while constructing portfolios that blend dozens of idiosyncratic alphas. In pod shops, these alphas are generated by small teams of portfolio managers (“pods”), each tasked with extracting incremental alpha within tight risk constraints. In quant funds, alphas are generated by algorithmic signals used to rank stocks and other assets. The risk models then blend these return streams into portfolios with tightly managed volatility that are largely uncorrelated to traditional asset class betas.

We have spent years building our own risk model because we view this as essential to competing in today’s ever-shifting markets. Building our own risk model has made clear just how effective these tools can be—and the role they’ve played in the astonishing success of top quant firms and pod shops from Arrowstreet and AQR to Millenium and Citadel.

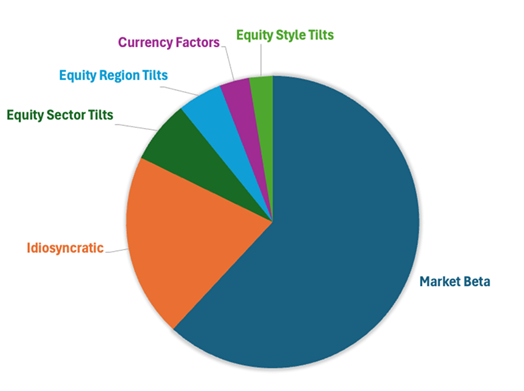

To understand today’s markets, investors must understand these models and how they’re used. Let’s start with the basics. A risk model takes a portfolio of tickers and translates it into a common set of risk factors. These quantitative factors can explain a large share of return variance. Take, for example, the current star concentrated manager, Chris Hohn at TCI. Here’s how his portfolio looks to a risk model.

Figure 1: Chris Hohn’s Portfolio Sources of Risk (2025)

Sources: Capital IQ, Verdad analysis. Holdings of TCI compiled from 13F disclosures and exchange announcements as of 2/5/2026. Verdad SAGE model used for attribution.

In TCI’s case, roughly 80% of total portfolio risk is attributable to common factors. Market beta alone accounts for approximately 60%, with the remainder coming from regional tilts (overweights to the US and Europe), sector and industry exposure (notably aerospace), style factors skewed toward large, profitable companies, and currency exposure.

That’s the risk reporting function of a risk model, but the true “arcane knowledge” that top hedge funds possess today is how to weaponize that risk model and turn it into an offensive tool for alpha generation. If Chris Hohn ran a pod for Citadel, they would likely hedge out all of those tilts and run only his idiosyncratic exposure. If a quant fund sought to replicate his returns, they would build a portfolio that matched his factor exposures and seek to explain his idiosyncratic selection through a more highly specific alpha model. Both approaches would also likely conclude that his idiosyncratic risk is insufficiently diversified.

These platforms use risk models not just to observe exposures but to engineer them. The key requirement for producing this type of portfolio is breadth: a wide variety of return streams that can be blended together.

Pod shops source that breadth from the idiosyncratic alpha of individual portfolio managers, as described in our earlier piece on pod shop alpha.

Quant funds take a different approach. Rather than managing pods of discretionary stock pickers, they conduct academic-style research to identify systematic sources of return and then express those alphas across the broadest possible opportunity set.

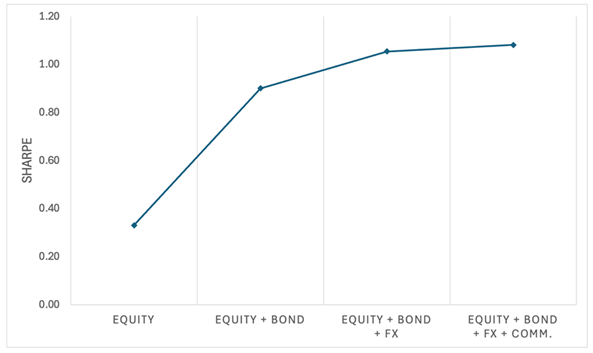

The power of this approach lies in a different kind of breadth. Even when individual asset classes exhibit only modest standalone performance, combining them under a unified risk model can materially improve risk-adjusted returns. Figure 2 illustrates this effect by showing how a portfolio’s Sharpe ratio increases as additional, imperfectly correlated asset-class return streams are added while total portfolio risk is held constant. The effect is amplified when true alpha sources are layered on top of this diversified foundation.

Figure 2: Impact of Increasing Diversification on a Quant Strategy

Source: Verdad analysis. Results are illustrative and based on stylized assumptions intended to demonstrate the structural impact of diversification under a unified risk model.

When risks are managed along common dimensions across all assets, portfolios can be assembled that would be impossible to understand—and could not survive—without a model. Risks can be aggregated and evaluated across tens of thousands of liquid instruments. Hundreds of independent alpha streams can coexist without unintentionally stacking the same macro or factor exposures. The result is a return stream that is smoother, more resilient, and far more scalable than traditional discretionary portfolios. Stable, high-Sharpe returns are not the product of better stock picking alone but of superior risk engineering.

For allocators the implication is simple: the world that produced the endowment model is gone. That model emerged in a time when markets were less correlated, information flows were slower, and portfolio outcomes were still dominated by individual security selection. In that environment, it was reasonable to believe that exceptional stock picking, combined with patience and diversification, would capture the non-systematic slice of return that mattered.

Today’s markets operate on a different clock and a different dimensionality. Risk is continuous, pervasive, and woven through every asset, sector, and geography. The question is no longer whether a manager can pick the “best” names in a concentrated sleeve but whether they understand, measure, and control how exposures aggregate across hundreds of cross-cutting drivers of return.

Humans may be good at pattern recognition in low dimensions—one market, one sector, one thesis at a time. But the human brain hits capacity limits when it comes to holding tens to hundreds of interacting drivers in mind and judging their combined effect on portfolio outcomes.

The consequence of that cognitive boundary is structural. Managers who rely primarily on intuition or narrative conviction tend to accumulate hidden risk: exposures that feel benign until they aren’t. These portfolios look concentrated because most of the capital sits in a small number of names, but in risk space they are often diffuse and poorly measured. Allocators who equate concentration with conviction are not necessarily capturing skill; they are often accepting risks that are neither intentional nor well understood.

Public markets are interesting precisely because they allow risk to be decomposed, recombined, hedged, and expressed across assets, directions, and time horizons in real time. Long and short positions, multiple asset classes, and rapid feedback create a landscape where high-dimensional risk management is not a complication but the core challenge. The rise of pod shops and large quant platforms reflects this reality. These firms were not drawn to risk models out of academic preference. They were forced there by the structure of modern markets, and they survived by learning to think explicitly in risk space.

Our own work on risk models has followed the same logic. Engaging seriously with these tools has changed how we think about portfolio construction, diversification, and where incremental returns actually come from in liquid markets.

The question is no longer whether risk models matter. That debate has been settled by results. Risk models allow us to engage public markets as they actually are—liquid, multi-asset, and inherently high-dimensional.