Revaluation in Japan

Successful reformers dividend aggressively and invest conservatively

By: Naoki Ito

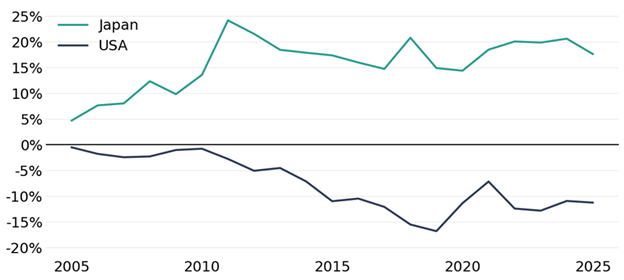

In the period of hyper-low interest rates that followed the 2008 financial crisis, US companies leveraged up their balance sheets. Japanese companies, scarred by the financial turmoil, chose to do the opposite, adopting a conservative approach of building fortress financials.

Figure 1: Median Cash & Investments Minus Debt as % of Market Cap by Region

Sources: S&P Capital IQ, Verdad analysis. Notes: Financials and REITs are excluded. All values are measured at calendar year end.

Though this might seem like prudence, many Japanese companies took conservatism to an extreme, accumulating balance sheet assets far beyond what financial logic would justify. The result is a Tokyo stock market crowded with firms trading below the value of their net assets.

Consider two examples. Chofu Seisakusho (TSE:5946) carries no debt and holds $40 million in cash, $680 million in marketable securities (mostly corporate bonds) and $70 million of rental real estate at fair value, yet it has a market capitalization of only $460 million. TPR (TSE:6463) has $220 million of net cash and $230 million in marketable securities (primarily cross-shareholdings in other listed Japanese companies) relative to a market capitalization of $600 million. We could provide dozens of similar stories.

Such irrational capital allocation policies are no longer tenable. The Tokyo Stock Exchange and policymakers have made it clear to corporate Japan that it’s time to begin deploying these assets that have sat idle on balance sheets for decades. Sub-1x P/B companies need to present credible plans to move above book.

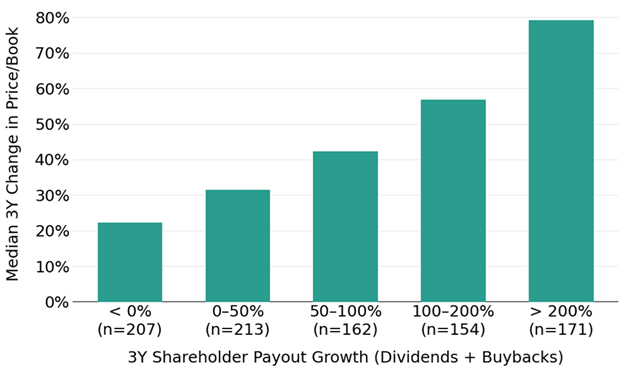

Three years since corporate governance reforms began in earnest, the data is now robust and clear enough to draw conclusions on exactly what companies trading at less than 1x P/B need to do to achieve the bar set by the TSE: increase dividends and buybacks dramatically. The chart below shows that more aggressive increases in dividends and share buybacks were associated with larger median improvements in P/B multiples.

Figure 2: Valuation Change by Payout Growth for Companies with P/B < 1x on 12/31/2022

Sources: S&P Capital IQ, Verdad analysis. Notes: 12/31/2022 – 12/31/2025, LTM values for TSE-listed companies.

For companies trading below book value, dividends and buybacks are the most direct path to value realization.

Even if valuation repair is achievable through an obvious strategy of increasing shareholder returns, many management teams at companies trading sub-1x book continue to emphasize growth investments over distributions. Corporate plans to “improve value” therefore frequently default to ambitious capital investment programs that grow asset scale, even when that growth comes at the expense of capital efficiency.

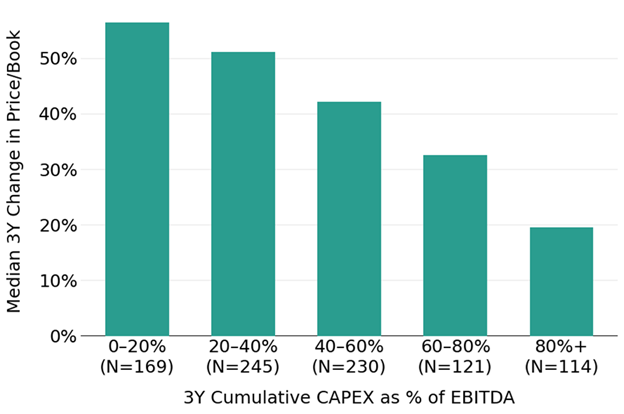

Our analysis shows that, among companies trading below 1x book, valuation re-rating has been associated with capex restraint rather than capex expansion, as shown in Figure 3. Firms with low capex intensity over the last three years saw median P/B gains of 50–60%, while those with high capex intensity experienced weaker revaluation, closer to 20%.

Figure 3: Valuation Change by CAPEX Intensity for Companies with P/B < 1x on 12/31/2022

Sources: S&P Capital IQ, Verdad analysis. Notes: Financials and REITs are excluded. Companies with negative cumulative EBITDA are excluded. Three-year figures are measured using LTM values from calendar year end 2022 to 2025.

For firms trading at deep discounts to book value, investors’ central concern is not insufficient growth but the persistence of low-return assets tied up in trapped capital. Evidence suggests that Japan’s valuation repair among companies trading at deep discounts to book has been driven primarily by capital discipline rather than heavier reinvestment for growth.

As Japan’s reform agenda advances, the revaluation of trapped capital is likely to be most powerful where investor skepticism remains greatest. The largest potential upside may lie among companies trading at the deepest discounts to book despite holding substantial capital reserves—firms where markets have long questioned whether balance-sheet assets would ultimately translate into shareholder value.

For management teams that continue to face low valuations, like P/B below 1x, ambitious growth plans or larger investment budgets are not necessarily the most direct path to re-rating in line with the TSE’s reform objectives. The goal cannot be growth for its own sake but rather capital-light expansion paired with stronger shareholder returns.