Why Hedge Funds Got Better While Private Equity Just Got Bigger

The Structural Forces Reshaping Alternative Investing

Investment allocators’ perceptions of private equity and hedge funds could not be more different.

Talk to an “endowment model” CIO at a foundation or multi-family office and you’re likely to hear something along the lines of, “There’s no alpha in public markets.” In 2025, the hedge fund industry posted its best returns since the Global Financial Crisis, but after Buffett’s famous bet, the consensus has been that hedge funds are an expensive way to underperform the market.

Private equity, by contrast, maintains a distinguished aura of wisdom, long-term thinking, and value creation. The typical endowment model CIO says something along the lines of, “All our alpha is going to come from private markets.” Many of these CIOs have hired teams focused on finding niche managers and underwriting co-investments and direct deals. Despite years of PE underperformance, enthusiasm remains undiminished.

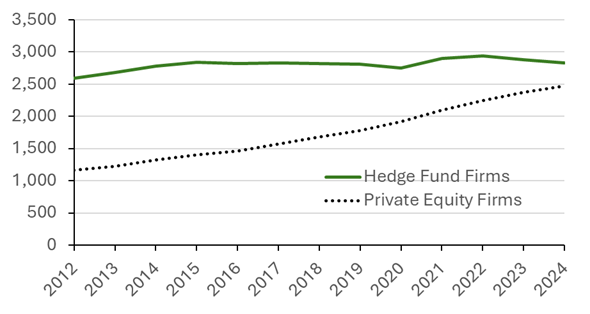

These divergent perceptions are reflected in industry-level statistics. The SEC conveniently aggregates numbers on private equity firms and hedge funds and their assets under management from the data submitted in form ADV. We can see that, over the past decade, the number of private equity funds has doubled while the number of hedge funds has stayed roughly flat.

Figure 1: Number of Hedge Fund Firms vs. Number of PE Firms

Source: SEC

It’s been a boom time in private equity. A massive proliferation of new entrants has benefited from low barriers to entry in a rapidly expanding market. In contrast, the hedge fund industry has been fighting significant headwinds: negative public perception, a ripping S&P 500 index that has made diversification less appealing, and a fundraising environment enamored with private markets.

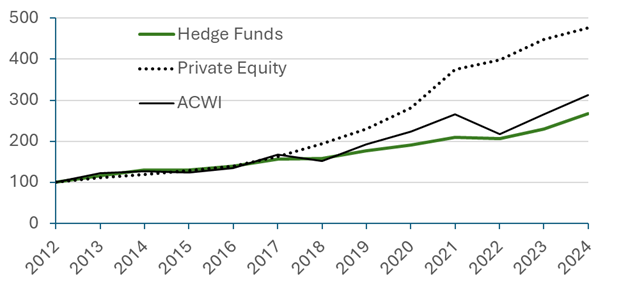

As a result, we can observe significant new assets flowing into private equity while hedge funds have treaded water. “In other words,” reads a recent Bloomberg op-ed, “hedge funds as a whole hardly attracted any new money, and fundraising became a competitive zero-sum game where a few winners take all.”

Figure 2: Indexed Growth in Hedge Fund & Private Equity Assets vs. ACWI Total Return

Source: SEC

This divergence is not random.

Hedge funds and private equity operate under fundamentally different selection mechanisms. Hedge funds are marked to market daily, performance is observable in real time, and allocators can redeem capital quickly. Weak processes, poor risk management, or spurious alpha are exposed and punished rapidly. Over time, this creates a Darwinian environment in which only firms with genuine, repeatable advantages survive and scale.

Private equity, by contrast, is largely insulated from this feedback loop. Returns are reported with long lag and wrapped in narratives about “long-term value creation.” Lockups defer accountability, both for managers and allocators. The “phony happiness” of private equity allows for a far larger number of firms—good, mediocre, and poor—to coexist.

In hedge funds, we have witnessed the emergence of what I think of as apex predators. Pod shops like Citadel and Millenium seed, fund, and discard independent managers with interesting ideas. Quant funds like Arrowstreet and AQR plow their management fees into building ever more sophisticated quant models while hoovering up the best and brightest from finance and economics programs at top schools.

These firms have in common a highly sophisticated approach to risk management, with models that capture the underlying dynamics of how today’s markets move. They can clearly separate alpha from beta. The canonical marketing sentence, derived by ChatGPT analysis of these top funds’ websites, is, “Rigorous/scientific research + data/technology + systematic process → alpha/returns with controlled risk for institutional clients.” The research, the tech, the systematic process, and the ability to control risk all amount to a kind of “arcane knowledge” that forms a competitive moat.

Private equity has no comparable “arcane knowledge” akin to hedge funds’ risk management technology. The canonical marketing sentence, derived by a ChatGPT analysis of the largest PE firms’ websites, is, “We partner with management teams + bring a differentiated platform and operational expertise to create transformational value / long-term outcomes.” How would one create a competitive moat out of “being a good partner” or having “operational expertise?”

These are fluffy, airy concepts. If “operational expertise” or “value creation” constituted a true and durable competitive moat in private equity, we should be able to observe it directly in the underlying fundamentals. In our own research, examining decades of data on private equity–owned companies, we find little evidence of systematic operational improvement relative to comparable public companies. Revenue growth at PE-owned businesses is not meaningfully higher, margins do not consistently expand, and leverage-adjusted fundamentals often deteriorate rather than improve over the hold period. Where returns do appear strong, they are largely explained by financial engineering—higher leverage, multiple expansion, and favorable exit environments—rather than by persistent improvements in operating performance. In other words, the primary sources of private equity returns are well understood and cyclical, not the result of a repeatable, hard-to-replicate operational edge.

This has meant a very different experience for entrepreneurship in hedge funds and private equity. Despite data showing that this area is where growth is lowest and default rates are highest, allocators remain in love with niche mid-market private equity, funding fundless sponsors and new managers with excitement. In contrast, allocators compare new hedge funds to Arrowstreet or Citadel, and they are rightfully skeptical of whether smaller funds can develop the risk management infrastructure or differentiated research process of these much more scaled, well-resourced funds.

The result is a striking allocator paradox. In hedge funds—where leverage is modest, liquidity is high, and risk can be modeled precisely—allocators demand scientific rigor, data, transparency, and demonstrable process differentiation. In private equity—where leverage is higher, liquidity is nonexistent, and business risk is paramount—those standards are relaxed, and storytelling often substitutes for evidence. Capital has flowed away from an industry that has been forced to prove alpha under relentless scrutiny and toward one that has largely avoided it. If history is any guide, it is the former environment, not the latter, that produces durable competitive advantages.

We have built Verdad in this brutally competitive environment. We do not yet pretend to be an apex predator, but we are students of their success. We have taken seriously the lesson the public markets have taught: Durable success increasingly requires deep research, technology that encodes and compounds judgment, and an explicit, internally owned understanding of risk.

Over the last several years, we have poured resources into building these same ingredients, developing a shared research platform, investing in our own technology stack, and constructing in-house risk models rather than relying on vendor abstractions. What has made this possible at our scale is not exceptionalism but timing. Advances in cloud infrastructure, modern SaaS tools, and AI have dramatically lowered the cost of building institutional-grade systems. Using platforms like Snowflake and AWS, a small, focused team can now do work that once required massive organizations.

And we have focused on niche market areas that are too illiquid for larger players to invest, like Japanese micro-caps. We know, for example, that factor investing works better in smaller companies, and we have used our small relative scale as an advantage.

We believe that the next few years will produce an ongoing reckoning in private equity. The hedge funds that have learned to find sustainable sources of alpha and thrive in this brutal market appear to us to be materially better than the hedge funds of 15 years ago. We believe the ongoing revolution in research, technology, and risk management makes hedge funds a much more exciting space than most allocators realize.