Do Treasurys Still Work?

Understanding the drivers of Treasury returns

By: Greg Obenshain

Professional investors are paid to take risks. Owning risk-free Treasurys therefore might seem like an option for the company 401K, not something for professional money managers or institutional allocators. But boring old Treasurys have been a wonderful asset class to own since the 1980s, providing stable income, capital gains, and excellent diversification, consistently rising in times of crisis to offset losses in equities.

Yet with yields barely above zero and inflation fears increasing, many investors fear that the future for Treasurys may look substantially worse than the past. Some even say we are in the midst of a historic bond bubble. So how should investors think about Treasurys? Do they still play an important role in a diversified portfolio?

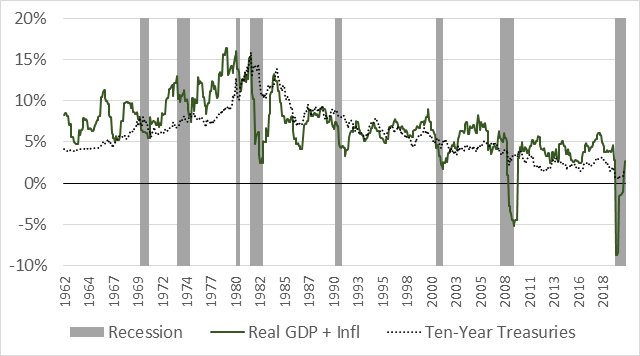

To answer this question, we must first understand what drives government bonds. The great economist Irving Fisher argued nominal Treasury yields are the sum of real interest rates and the expected inflation rate. Indeed, if we simply look at the sum of real GDP growth and inflation over time, the 10-year Treasury yield moves with this series.

Figure 1: Real GDP Plus CPI Inflation versus 10-Year Treasury Yields

Source: FRED

The two drivers of Treasury return, therefore, are growth, which impacts the real rate, and inflation. The real Treasury rate is the opportunity cost of not investing in the domestic economy. If economic growth improves, then the real rates rise and bonds do relatively poorly. If, however, growth falters, then real rates fall and bonds do well. Similarly, if inflation expectations rise, investors will demand a higher premium over real rates, driving Treasury yield up and returns down. When inflation expectations fall, this premium falls and bonds can do well.

Since the early 1990s, real growth and inflation have been highly correlated. Over the past 30 years, we have broadly experienced a period of falling growth and falling inflation, an ideal environment for Treasurys. And in most of the recent recessions, growth and inflation expectations have both collapsed simultaneously, making Treasurys an ideal equity hedge in times of market panic.

But what investors today fear is a repeat of what happened in the late 1970s. During this period, inflation peaks tended to coincide with recessions, offsetting the benefit Treasury investors should have received for holding safe rates. We can see this dynamic in the early years in the chart below.

Figure 2: Annual Real GDP Growth and Inflation

Source: FRED

This is clearer if we further decompose Treasury returns much like we decomposed equity and bond returns. The table below divides Treasury returns into carry return (the return you know you will get because of the yield) and price return (the return you get due to changes in rates). In this table, the price returns best describe how the macro environment has affected Treasury returns.

Figure 3: Decomposed Treasury Returns by Decade, Annualized, Jan 1962 – March 2021

Source: Verdad analysis, Federal Reserve. The yield data underlying this chart comes from a dataset posted by the Federal Reserve that uses the methodology in a paper by Stefania D’Amico, Don H. Kim, and Min Wei that takes the information embedded in TIPS prices, inflation surveys, and Treasury prices to decompose Treasury rates into inflation and real rate components. For data prior to 1983 when their data begins, we use the Livingston inflation survey as the estimate of inflation compensation.

Over the long term, carry has been the main driver of returns, with inflation compensation accounting for a greater share of returns than real rates. Today, the picture is even more dramatic: real rates are negative while inflation compensation accounts for the entirety of the positive Treasury yield. Inflation compensation of 1.6% may be low relative to the long-term inflation rates of 3.4% since 1947, but real rates of -0.6% are the true outlying data point on this chart as real GDP has averaged 3.1% over the same period.

What the Treasury market is saying today, then, is that real growth expectations are very low. And recent correlations suggest that there will not be inflation without growth. This is why the most successful bond investors, such as Lacy Hunt of Hoisington Investment Management, have focused their analysis on trends in secular growth rather than secular inflation.

The key question Treasury investors must therefore ask is whether growth will come in above or below the expectations priced into the Treasury market. Historically, Treasurys have lost money when economic growth prospects have improved and made money when growth expectations have deteriorated. We can see this by comparing Treasury returns to changes in the high-yield spread, which we believe is one of the best leading indicators of economic growth. Below we show Treasury returns by previous three-month movements in the BBB spread. We use the BBB spread because we have a long, consistent history for that spread, and it moves with the high-yield spread.

Figure 4: 10-Year Treasury Returns Following Three Month Changes in BBB Spread, 1962–2021

Source: Bloomberg, Verdad Analysis

When the spread is widening as economic conditions deteriorate, Treasury returns tend to be very positive. When the spread is tightening as economic conditions improve, Treasury returns tend to be negative.

This relationship has not changed. We are currently in an environment where credit spreads have been steadily tightening and real yields are at low levels. The rise in 10-year Treasury yields from 0.91% at the end of 2020 to 1.75% at the end of March 2021 has been linked to inflation in the popular press, but it may have as much to do with improving growth as it does with inflation. Treasuries are doing what they normally do in an environment of improving growth and tightening spreads.

We are arguing that investors in Treasurys should shift their attention from worrying about inflation to worrying about growth—and trading Treasurys based on the direction of the economy. When spreads widen and growth expectations fall, Treasurys provide attractive countercyclical return potential. And when spreads tighten and growth expectations rise, investors should reduce or eliminate Treasury holdings. We believe this paradigm should hold for as long as growth and inflation are positively correlated. They key thing to watch for is signs of this post-1980 paradigm shifting, of inflation and growth decoupling, which would create the conditions for a longer-term bear market in Treasurys and a longer-term bull market in real assets.