What Higher Oil Volatility Means for Equity Markets

Lessons from historic oil volatility spikes

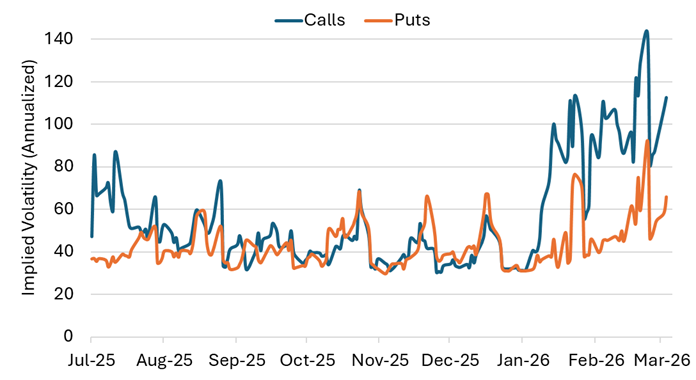

The Iran war created a macro uncertainty shock this week as markets tried to price in the risk of a spike in oil prices. We saw a sharp rise in volatility skew, with the implied volatility of oil calls (big upside moves) moving considerably higher than the implied volatility of oil puts (big downside moves).

Figure 1: Implied Volatility of Brent Futures Options

Sources: Bloomberg, Verdad analysis

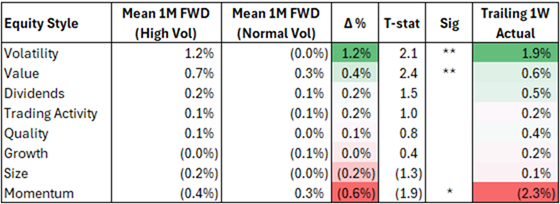

We wanted to understand how this type of sharp rise in oil volatility has historically impacted markets. To answer this question, we examined periods of elevated oil volatility (greater than one standard deviation above the average) and compared forward one-month returns for equity style factors.

We have daily data for factors and oil going back to 1995, which we clustered by month (roughly 360 months). There have been 37 months that experienced a one-standard-deviation elevation in volatility versus the average month and 325 “nonevent” months. We can regress the mean of the event versus nonevent months to see whether there is a statistical difference, as shown below.

Figure 2: Equity Style Factor Performance Event Regression

Sources: Bloomberg, Verdad analysis

As Figure 2 shows, we can see that volatility and value factors tend to perform better while momentum tends to perform worse. On average, volatility performs about 1.2% better while value performs about 40bps better. And momentum performs about 60bps worse than average.

What’s fascinating is that the realized performance of these factors since Friday, February 27, the day before the US and Israel bombed Iran, has spread almost perfectly with what our regression model expected.

We could wax philosophical about why these differentials in factor premia may exist during periods of elevated oil volatility and what the mechanisms behind them are. But the more important takeaway is that these differences in performance can be modeled, predicted, and incorporated into dynamic portfolio construction.

We believe that understanding linkages between and within major asset classes, macroeconomic variables, and risk factors is essential to robust portfolio construction.

As we wrote about in our paper, “Crisis Investing,” factor premia tend to be more predictable during periods of market stress. If we can model the many dimensions of stress and how they impact asset prices, we can increase our odds of constructing portfolios that are robust to macro shocks.