The Rise of Chinese Biotech

How China created a domestic biotech industry

For decades, biotech investors considered China an innovation deadzone, defined by “me-too” drugs and discounted data.

And then came Akeso’s ivonescimab, a bispecific antibody born from a Chinese lab once dismissed as a “fast-follower.” In a head-to-head trial in 2024, this Chinese molecule outperformed Keytruda, the world’s best-selling drug and one of the most innovative oncology treatments to emerge in decades. The “DeepSeek moment” of Chinese biotech had arrived.

This was not luck. It was the product of massive investment in the wake of the CCP’s identification of biotech as a strategic emerging industry in its 14th Five Year Plan (2021–2025). Pursuing the same strategy the country used to achieve competitiveness in manufacturing, China has attempted to make drug development significantly faster and more cost-effective than in western countries with higher labor costs and regulations.

This strategy has scored some early successes. According to 2026 data, discovery-to-IND (investigational new drug) cycles in China are 50% to 70% faster than in the US or Europe. This speed is coupled with a capital efficiency that sees discovery programs run at one-third to one-half of global costs, resulting in clinical development cost that is 20% to 50% cheaper than US levels.

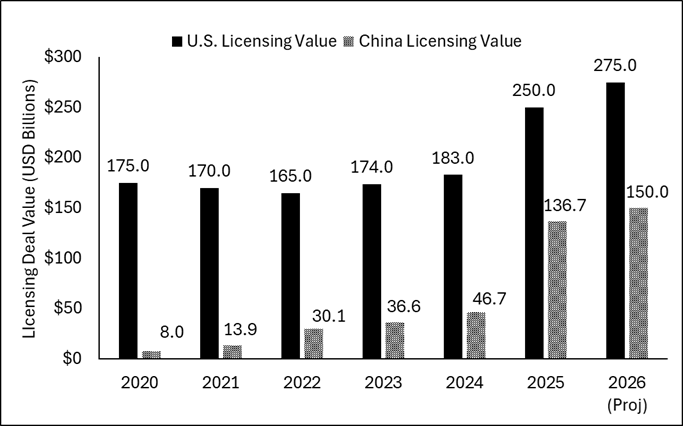

This has been irresistible to global drugmakers facing a historic $200B “patent cliff.” And we have seen a surge in cross-border deals since 2020. The chart below shows the total deal value of Chinese versus US out-licensing deals (selling drug rights to Western big pharma) by year.

Figure 1: US vs. China Biotech Licensing Deal Value (2020–2026)

Sources: PharmCube (China) J.P. Morgan and PitchBook (US)

What is remarkable is how quickly China has gained ground. In 2021, China officially surpassed the United States in total clinical trial volume and has widened that lead in every subsequent year. In 2025, China conducted approximately 7,700 trials compared to roughly 6,250 in the US. China’s share of global innovative drug candidates rose from 8% in 2018 to 30% by 2026, whereas the US share declined from 47% to 36% over the same period.

The growth is also evident in the number of “innovative drugs” submitted for human testing, which rose from 688 in 2019 to 2,298 in 2023. By 2024, China had become the world's second-largest source of first launches for new molecular entities, holding an 18% global share. In 2025, China reached a milestone where it surpassed the US in blockbuster deal (>$1B) origination (35).

But what does this mean for public markets? How have Chinese biotech stocks performed relative to the US? And how do the lessons we’ve learned about investing in US biotech apply to China?

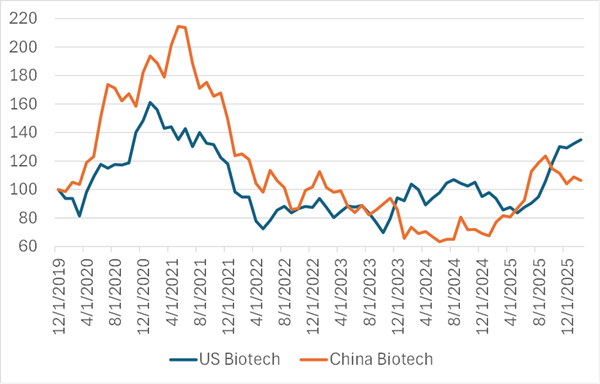

Today there are about 82 Chinese biotech stocks listed in Hong Kong and 520 traded in the domestic Chinese market, as compared to 780 stocks classified as biotech in the United States. The graph below shows the performance of Chinese versus US biotech since 2020.

Figure 2: US Biotech (XBI) vs. China Biotech (2820:HK)

Source: Capital IQ

Despite the massive investment and success in building a domestic biotech industry, the experience of stock market investors has been even worse in China than in the US.

Individual Chinese biotech stocks have had roughly the same loss rates as US biotechs. The process of investing in science projects is just as risky, it seems, regardless of where the research is done. Only 25 of 88 companies had positive annual excess returns, meaning that a Chinese company needed to be in the 73rd percentile (vs 67th percentile for the US) to have an excess return >0.

We also looked at the factors that predicted excess return within the universe of Chinese biotech, drawing from the research we did in the US for our recent white paper, “Biotech Investing.” We found that the Chinese biotech market has rewarded our measure of value (market cap/spend), with the cheapest quintile of stocks outperforming the most expensive stocks by about 18.3% per year from 2013 to 2026. We also found that large size has been strongly correlated with excess returns within Chinese biotech, with the largest quintile of Chinese biotech stocks outperforming the smallest quintile by 26.2% per year. We are working on a full international replication of our paper, and we will share our findings when complete.

Despite some differences in market dynamics, China’s influence on the biotechnology sector continues to grow, and industry and investor enthusiasm for China is on a high. The reality, however, is more nuanced: while the data confirms China’s prowess in discovery, it does not signal investors to immediately go long the Chinese biotech sector. The path for standalone Chinese firms to navigate global commercialization remains fraught with geopolitical and regulatory complexity.

Instead, it may be wiser to focus on the surge of cross-border licensing deals. As Western pharma giants race to fill the $200 billion revenue void created by the impending patent cliff, their ability to integrate these de-risked Chinese assets may separate the winners from the losers in the next decade.

Ultimately, it remains to be seen where the immense value of this ecosystem will accrue. The question is no longer whether Chinese innovation is viable but who will benefit most: the agile Chinese developers creating the molecules or the established pharmaceutical giants who possess the global infrastructure to sell them. For now, the most profitable dynamic appears to be an arbitrage of Chinese speed and Western commercial scale, suggesting that the “DeepSeek moment” might enrich global partners just as much as the domestic innovators.