The Rise of Alternatives

How consultants shaped institutional asset allocation

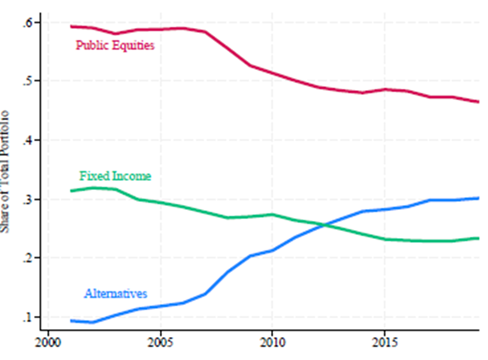

US public pensions have made a dramatic change to their asset allocations over the past decade. Allocators at these pension funds took investments in alternatives—private equity, real estate, and hedge funds—from 14% of their risky investments in 2001 to 39% by 2021.

Figure 1: Asset Allocation of US Public Pension Portfolios

Source: Juliane Begenau, Pauline Liang, and Emil Siriwardane, “The Rise of Alternatives”

A group of Stanford and Harvard academics is out with a fascinating paper making the case that this shift was not the result of shifts in realized performance, liquidity needs, or macroeconomic fundamentals. Rather, argue Stanford’s Juliane Begenau and Pauline Lang and Harvard’s Emil Siriwardane, the driver was a change in the beliefs of the pension funds’ investment consultants.

Their analysis is distinctive because it combines detailed data on public pension portfolios with consultants’ forward-looking capital market assumptions, allowing the authors to directly link shifts in asset allocation to changes in expected returns rather than realized performance. This matched dataset enables a structural analysis of how belief-driven expectations—especially about alternatives—shaped institutional investment decisions.

The authors argue that the consultant community collectively began to believe in—and act on—a consensus expectation about the superior alpha potential of alternative assets.

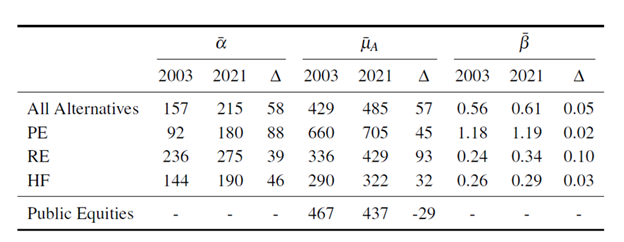

"Our evidence suggests that the rise of alternatives has been fueled by an increase in their perceived risk-adjusted returns relative to public equities," the authors write. This perception is embedded in consultants’ capital market assumptions, which play an outsize role in how public pensions and other asset owners shape their portfolios. Figure 2 shows how consultants’ capital markets assumptions shifted in the wake of the 2008 financial crisis.

Figure 2: Changes in the Average Consultant-Perceived Alpha

Source: Begenau et al.

The biggest shift was in private equity, with an 88bps increase in expected alpha from 2003 to 2021. "Consultant-reported beliefs about the alpha of alternatives relative to public equities have risen steadily since the 2000s," the authors note. These elevated alpha expectations, they argue, explain most of the portfolio shift observed in the data.

Consultants’ capital markets assumptions for alternatives diverged positively from those for public equities over the past decade, despite no commensurate divergence in realized performance. This change in belief was, in many cases, self-reinforcing: as more consultants published higher expected returns for alternatives, their peer firms followed.

This is the type of “correlated belief” that Stanford economist Mordecai Kurz has long warned about as a cause of financial crises. Kurz warned that markets dominated by agents with correlated beliefs can produce coordinated behavior even when fundamentals diverge. “The common economic explanation … is the existence of heterogeneous agents with diverse but correlated beliefs,” Kurz writes. In this case, the “agents” are investment consultants, and the shared belief is that alternatives offer superior alpha. The paper under review is essentially an empirical demonstration of Kurz’s theory in action: as consultants updated their alphas in tandem, institutions reallocated in a highly correlated fashion.

Andrei Shleifer’s work adds a complementary psychological angle. He has described how market expectations, particularly when shaped by narratives or recent performance, can become distorted in predictable ways. Shleifer argues that investors form a mental model of how markets work that simultaneously extrapolates good news and neglects tail risk. The authors of “The Rise of Alternatives” demonstrate that consultants, despite their presumed objectivity, are not immune to these dynamics. Their expectations exhibit clustering, momentum, and peer influence—traits that align closely with Shleifer’s behavioral models.

The sociology of belief formation—rather than pure economics—becomes central to understanding institutional portfolios in this framework. Capital market assumptions are not just inputs; they are persuasive tools. They define the language of risk, frame the boundaries of plausibility, and legitimate allocation changes. Once alternatives were viewed as the higher-alpha option, the allocation shift became not only acceptable but expected. And once enough institutions moved, the belief in their superiority became embedded—regardless of realized performance.

Importantly, the paper does not argue that alternatives are a mistake. The concern is not the destination, but the path. If the shift into alternatives was driven less by data and more by belief—belief that was formed in correlated ways across consultants—then institutional portfolios may be less diversified than they appear. What looks like a broad exposure to uncorrelated return streams may in fact be a concentrated bet on a shared set of assumptions.

“Our results suggest that understanding shifts in portfolio allocations requires understanding the expectations underlying them,” the authors write. That is perhaps the paper’s most important contribution: reminding readers that expectations, especially when widely shared and mutually reinforced, can shape capital markets just as powerfully as fundamentals.

In short, the “rise of alternatives” is not only a structural trend. It is a story of belief coordination. Consultants changed their minds, together. Institutions followed, together. And now we live in the portfolio equilibrium their expectations built.