Currency Valuations

The yen looks cheap, the peso expensive

Last week, the US Federal Reserve cut the benchmark interest rate another 25bps, bringing the policy rate range to 3.75%–4%. With US rates falling and tariff threats rattling markets again, it’s worth exploring how the US dollar currently fares against other currencies in terms of its relative attractiveness as an investment.

Thinking about currency valuation can be a little like thinking about special relativity. It’s not immediately intuitive, and it all depends on what your reference point (or currency) may be. Many US investors get paid in dollars, invest in dollar-denominated assets, and don’t spend much time thinking about the relative attractiveness of the dollar versus other currencies. But for investors, the dollar is simply another asset, with a yield and a risk profile that can be compared to other currencies.

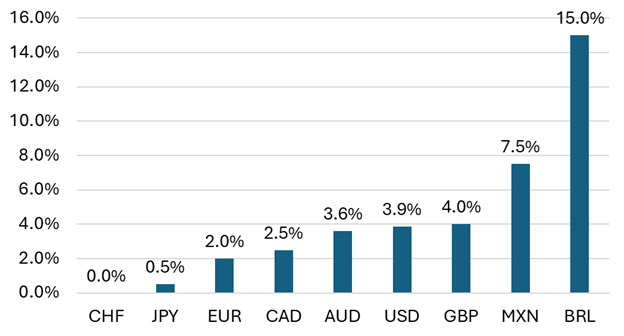

Therefore, it’s useful to have a simple framework for how to think about the USD in relation to other currencies. One way to compare currencies is via their yield, or the respective policy rate that each central bank has set. We can see below that, on this dimension, the USD looks rather middling after the most recent rate cut.

Figure 1: Nominal Yields of Major Currencies

Sources: Verdad analysis, Bloomberg

But nominal yields only tell us a small part of the story. If nominal yields were all that mattered, investors would be max long the Brazilian real (BRL) and max short the Swiss franc (CHF) to capture the 15% carry differential. But that differential exists because of differences in local inflation rates, local economic growth rates, and the relative attractiveness of the currency as a safe haven.

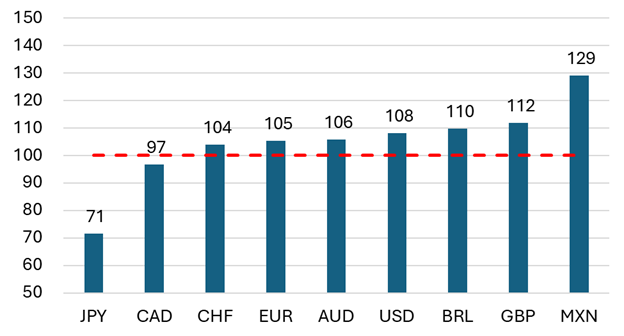

One way to try to account for these differences is with a metric called the real effective exchange rate (REER). This measure captures the weighted average of a country’s currency in relation to an index or a basket of the currencies of its major trading partners. This measure accounts for inflation dynamics, which can help us compare currencies directly.

REER helps measure a currency’s fair value and trade competitiveness. Currencies that trade above 100 are overvalued, and those that trade below 100 are undervalued. Below, we can see the REER of various currencies.

Figure 2: Real Effective Exchange Rates (REER) of Major Currencies

Sources: Verdad analysis, Bloomberg

According to REER, JPY is significantly undervalued, while BRL and GBP are slightly overvalued, and MXN is significantly overvalued.

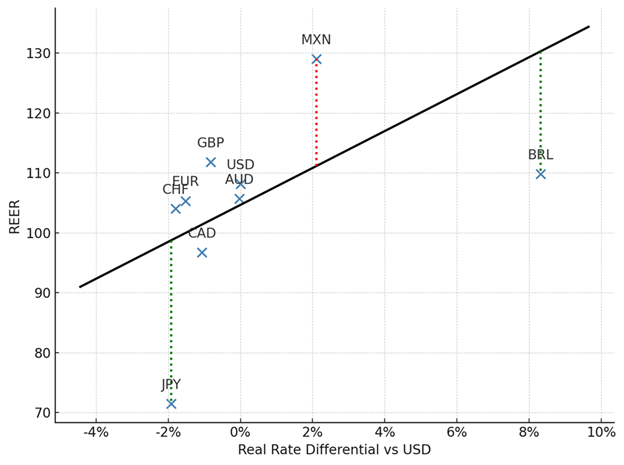

But REER only tells us where things stand today. It doesn’t tell us whether a given currency’s REER is “fair” or not. For instance, perhaps currencies with higher yields should be more richly valued on a REER basis because the higher rates attract capital inflows that appreciate the currency versus trading partners.

To test this hypothesis, we can estimate a “fair” REER with a simple model that only uses real interest rate differentials versus the USD as a predictor. This model can give us a sense of how relative monetary policy (managing real rates via nominal rates) may influence REER.

For this analysis, we ran a single pooled regression of over 76K daily observations of real interest rate differentials versus the USD against each currency’s respective REER since 1998. The regression has an r-squared of 16% and implies that currencies with a 1% increase in real rate differential versus the USD are associated with a ~3% appreciation in REER.

Figure 3: Current and Fitted REER vs. Real Rate Differential

Sources: Verdad analysis, Bloomberg

Relative to our fitted REER, there are a few immediate observations. First, both the Japanese yen (JPY) and Swiss franc (CHF) currently pay near 0% interest rates, but the yen appears deeply undervalued versus the implied REER via its real rate differential. Conversely, the Swiss franc appears slightly overvalued.

The Mexican peso continues to look quite overvalued versus the fitted REER, and the Brazilian real now looks undervalued versus where the regression would expect it to be valued.

This is a very simplistic model that only explains a portion of the variance in REER over time, but it offers a notably different view than either the nominal rates or REER alone. This sort of relative currency valuation is an important part of how we manage currency risk here at Verdad.