The Reflexivity of Credit Markets

Good times make for weak loans

By: Sam Hanson, Greg Obenshain, and Daniel Rasmussen

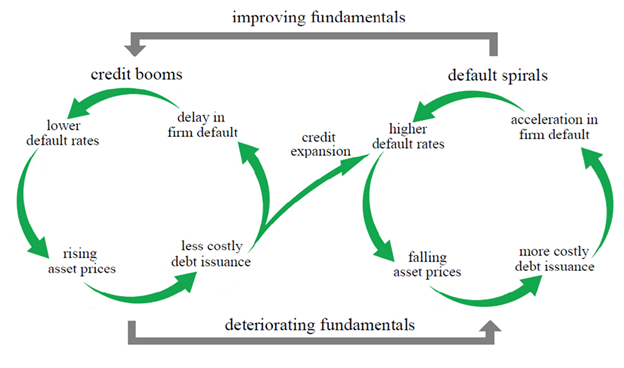

When defaults have been low, lenders revise their expectations. They infer that future defaults will also be low. Credit becomes cheaper and more available. Borrowers refinance more easily. That refinancing activity further reduces near-term defaults. The data looks even better. Lenders become more confident. Lenders loosen their standards again.

In recent work with Robin Greenwood and Lawrence Jin, Sam Hanson formalized this idea in a model demonstrating that lenders extrapolate from recent credit market outcomes. The likelihood of a default is not preordained or given “exogenously.” Instead, the likelihood of a default is influenced by lending conditions themselves. Cheap credit makes it easier for borrowers to avoid default in the near term, which in turn reinforces lenders’ beliefs that default risk is actually low.

As Sam shows, this process is self-reinforcing in the short run. It produces a sequence of observations that appear to validate the underlying beliefs and resulting behavior of making riskier and riskier loans. But over a longer horizon, overly optimistic lenders sow the seeds of their own destruction. Companies respond to the availability of cheap credit by levering up, leading to a build-up in the credit market’s vulnerability to unlucky shocks that will trigger defaults. When an unlucky triggering event lands in this financially fragile state, the cost of credit spikes and there is a wave of defaults by highly indebted borrowers. A credit market system that was calm and appeared to be stable was quite fragile in reality, completely catching optimistic lenders offsides.

Figure 1: The Credit Cycle

Source: Reflexivity in Credit Markets, Greenwood, Hanson, and Jin (2026)

Lender optimism is self-reinforcing in the short run and self-defeating in the long run. What ultimately matters is whether loans are repaid and losses realized, but that verdict arrives years later. During a boom, lenders instead see immediate rewards: higher volumes, more fees, growing AUM, and low defaults often sustained by easy refinancing. The near-term signals can look strongest precisely when underwriting is weakest and future losses are quietly building.

This feedback dynamic rewards behaviors that gradually increase default risk, even as conditions appear healthy in real time.

Over the last century, new forms of credit have often followed the same trajectory: they begin as genuine innovations, expand rapidly, post strong early results, attract capital, loosen underwriting standards, and eventually suffer losses that force retrenchment:

Consumer installment credit and commercial mortgages in the 1920s

Petrodollar loans in the 1970s

High-yield bonds in the 1980s

Collateralized mortgage obligations in the 1990s

Non-conventional mortgages, private-label RMBS, and CDOs in the 2000s

Private credit in the 2020s?

The next question is where those losses ultimately surface. Credit risk rarely stays with the original lender; it migrates to insurers, pensions, reinsurers, and other yield-seeking investors. Many of these institutions are not built to absorb concentrated credit losses. Especially with new and untested products, history shows that credit risk migrates toward investors who either don't fully understand or don’t have a natural advantage at what they are getting themselves into.

For instance, in the 1980s junk bond boom, a group of insolvent savings and loan associations became convinced that junk bonds were the solution to their problems. Michael Milken managed to persuade many insurers that the higher yields on junk bonds were special compensation for liquidity and were more than adequate to compensate for the additional default risk. Insurers used junk bonds to back guaranteed investment contracts (GICs). And lots of wealthy retail investors, drawn by the promises of equity-like returns with only bond-like risks, flocked to mutual funds. None of this turned out well for these investors when the market collapsed in 1990.

In recent years, private capital fund managers have again managed to persuade a bunch of pensions and insurers that the higher yields on junk bonds were special compensation for liquidity and were more than adequate to compensate for the additional default risk. It’s too early to tell, but the “Bermuda Triangle” trade involving offshore reinsurers might prove to be the GICs or the S&Ls of today’s private credit boom, with BDCs and other retail-facing private credit products acting like the high-yield mutual funds of the 1980s.

We will see how all of this plays out. But the rhyme with the 1980s seems just about perfect. So what does this imply for credit markets today?

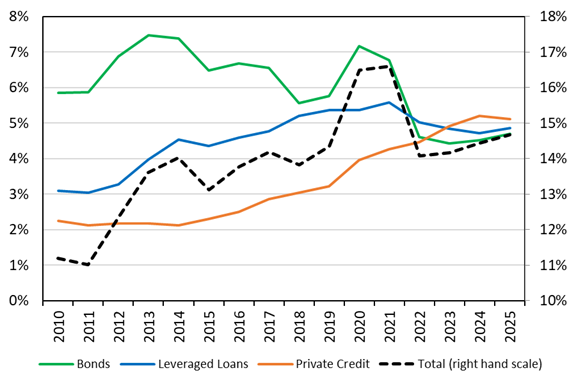

The US has not experienced a broad-based credit boom. The total amount of high-yield debt outstanding has risen somewhat relative to GDP in recent years (this is the black dashed line below), but the current level—equal to roughly 15% of GDP—is moderate. Aggregate corporate leverage has actually declined somewhat since 2020.

Figure 2: US High-Yield Rated Credit as a % of GDP

Source: Morningstar

Aggregate lending levels do not look alarming. What’s alarming is who is doing the lending. As shown above, private credit has grown from roughly 2% of GDP in 2010 to more than 5% in 2025, while the high-yield bond market has shrunk relative to GDP. Default risk has migrated from more seasoned markets—high-yield bonds and leveraged loans—to the far less tested private credit market.

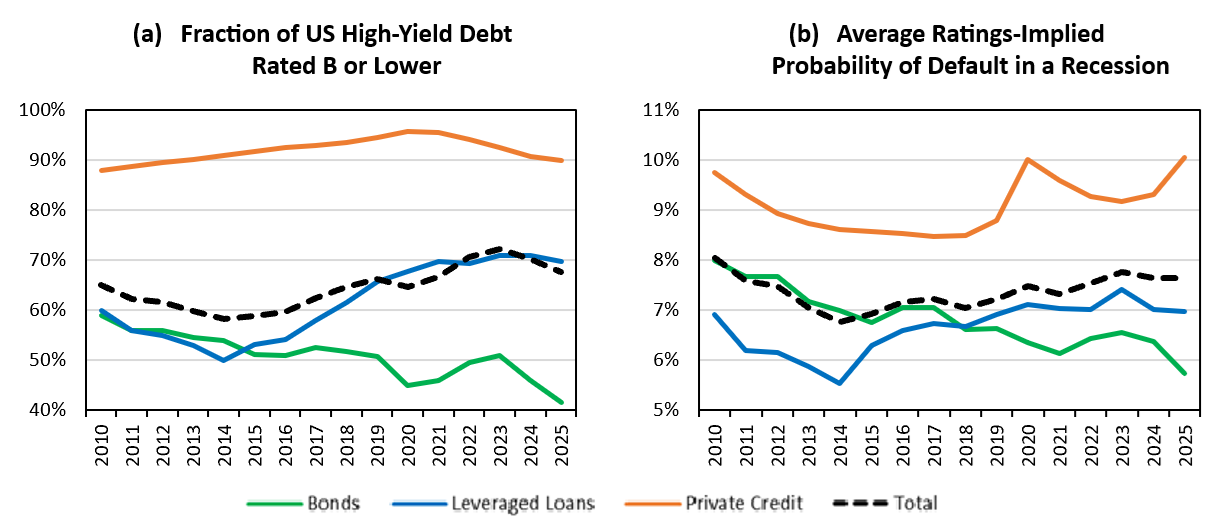

This shift is concentrated among weaker borrowers. Figure 3(a) shows the share of debt rated single-B or lower across bonds, leveraged loans, and private credit, while Figure 3(b) shows the corresponding ratings-implied recession default probabilities for each market and for the combined high-yield universe.

Figure 3: Credit Quality in US High-Yield Debt Markets

Sources: Morningstar for credit ratings in bonds and leverage loans, a variety of data for credit ratings in private credit, and Moody’s for default probabilities. The average ratings-implied probability of default is based on the evolving distribution of credit rating grades for each type of debt and historical default rates for each credit grade during recession years from 1983 to 2024. Some missing data has been interpolated.

Figure 3(a) shows that private credit has long served weaker borrowers, typically those rated single-B or lower. Credit quality has worsened in leveraged loans—the share rated B or lower rose from 50% in 2014 to 70% in 2025—but improved in high-yield bonds, where that share fell from 60% in 2010 to 40% in 2025. Across all three markets, the share of debt rated B or lower has risen only modestly, from roughly 60% in 2015 to 70% today.

Figure 3(b) tells a similar story using ratings-implied recession default probabilities: improving quality in bonds, deteriorating quality in leveraged loans, and only modest overall deterioration in the combined high-yield market.

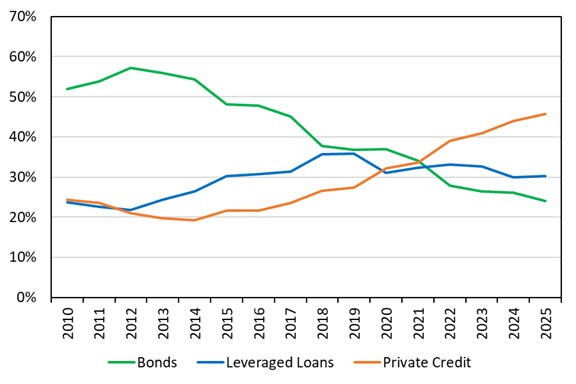

In short, these shifts are less about how much risk exists than about who now holds it. In 2010, roughly half of that risk sat in the bond market, with leveraged loans and private credit splitting the rest. Today, more than 45% sits in the new and largely untested private credit market, with bonds and leveraged loans dividing the remainder.

Figure 4: Allocation of Total Default Risk within the US High-Yield Credit Market

Sources: Morningstar and Moody’s. The contribution of each debt type (i.e., bonds, leveraged loans, or private credit) to the total ratings-implied default probability for all US high-yield credit equals each type’s fraction of total outstanding high-yield debt multiplied by its implied default probability. The total implied default probability is the sum of these three contributions. Each type’s fraction of total high-yield default risk then equals its contribution to the total default probability divided by the total default probability.

History teaches a consistent lesson: when risky credit—especially a newer and less-tested form of risky credit—grows this quickly, caution is warranted. Rapid growth often looks safest in real time. That is precisely when underwriting slips, leverage builds, and risk migrates to holders least prepared to bear losses.