Racing the Bear

Why private equity is likely in worse shape than private credit

By: Greg Obenshain & Daniel Rasmussen

Coverage of the markdown cycle in private credit seems to have focused almost exclusively on the risks posed to private credit lenders. The media has focused less on what sits below the debt: private equity. The majority of private credit goes to funding leveraged buyouts, and 77% of LBOs are financed by private credit. Once private debt is marked down, the private equity it funds—junior in the capital stack—is almost certainly going down harder.

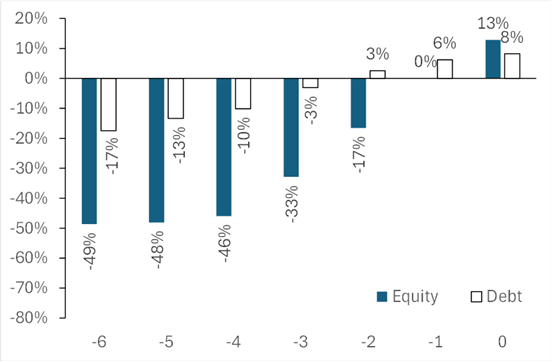

To illustrate the logic, the chart below shows one-year bond and equity returns for companies where credit deteriorated for that year. Each unit step on the x-axis represents a one-notch deterioration in credit quality (BB+ to BB for example).

Figure 1: Return on High-Yield Bonds and Matched Public Equities from Ratings Downgrade

Source: Verdad. Data is 1996–2026, measured monthly. Credit deterioration measured by market-implied credit ratings.

When the debt market downgrades a bond, the equity experiences outcomes that are many times worse. The logic is obvious: if you heard that the bank was marking the mortgage on a property down from 100 cents on the dollar to 80 cents on the dollar, wouldn’t you assume that the home equity was close to wiped out?

The equity and the debt are not distinct economic exposures. They are different claims on the same business and the same stream of cash flows. Private credit and private equity work the same way: one investor owns the senior claim, another owns the junior claim, but both ultimately depend on the performance of the same company.

A very smart friend of ours who works at one of the best private credit firms has made a bet with a friend of his at a top private equity firm that the returns on private credit will be better than private equity over the next five years. His logic: If we’re going through a tough period, equity will bear the brunt of the pain because debt holders are higher up in the capital stack. To him, private equity looks in far worse trouble than private credit.

In the race to escape the charging bear, private credit may indeed have the edge over private equity, but neither is in an enviable position. Whether private credit or private equity wins, however, depends not so much on how bad things are for the losers but on how many winners private equity has.

Let’s say, in a worst-case scenario, that 40% of a private equity fund’s deals go to zero. If the remaining 60% of the fund returns 2x, the fund is still profitable overall. A small number of big winners can make up for a lot of losses. This is not the case for private credit, where the winners just return their yield, but the losers subtract from returns.

We don’t know who will win this bet, but, in our opinion, the competition is now for the least-bad returns.