March Madness

How markets shifted during the Iran war

Only a few days into ceasefire, it’s perhaps premature to write a post-mortem on the Iran war’s impact on markets. But the macroeconomic moves were interesting enough that we wanted to share some early lessons from the data.

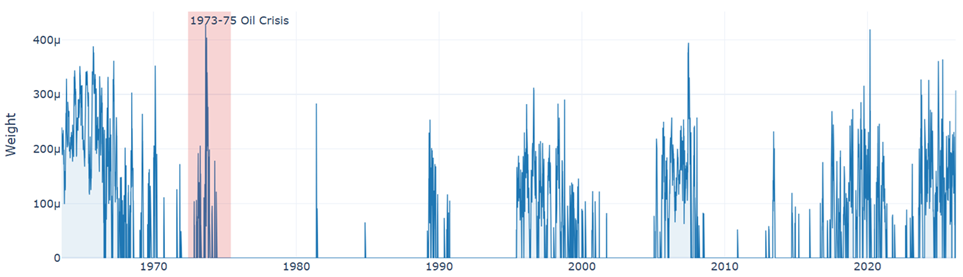

We look at markets through the lens of relevant historical analogues. March had some similarities to recent crisis periods in 2008 and 2020, but the most relevant historical moment, unsurprisingly, was 1973–1975 during the oil embargo.

Figure 1: Historical Macro Relevance

Source: Verdad analysis

The 1973 period was unusual in that inflation fears were spiking, high-yield spreads were rising, but short-term rates were elevated and the yield curve was flat to inverted. This type of environment is stagflationary because the Fed can’t raise rates further to deal with inflation without hindering economic growth.

Both the oil embargo years and today’s Iran crisis saw similar asset class returns: sharp upward movement in oil prices and the USD, with a sell-off in equities and bonds. The major difference is that gold rallied significantly in the 1970s but sold off in March.

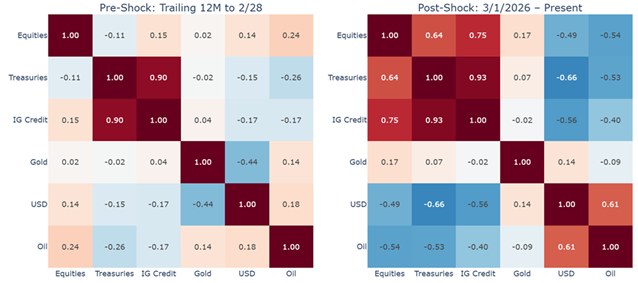

Looking at how correlations changed in March is also instructive. Equities, fixed income, gold, and foreign currencies all became more correlated while oil became negatively correlated to almost everything. The change in the correlation structure of these assets before and after March 1 is evident.

Figure 2: Major Asset Correlations before and after March 1

Sources: Bloomberg, Verdad analysis

Traditional diversifiers for equity risk like gold and Treasurys came up short in March.

The ceasefire announced last week might well return markets to more normal functioning, but we think there are some lessons to be learned from March Madness:

Value offers safety in times of market stress. Value outperformed (+2.6% on a long-short sort) in March, while stalwarts like momentum (-1.0%) and quality (-1.2%) lagged. To be sure, value benefited from an energy sector tilt, but beggars can’t be choosers.

Demand-side shocks are not the same as supply-side shocks. In demand-side shocks, when uncertainty is rising, pro-cyclical assets like equities, high-yield credit, and oil tend to sell off while safe havens like Treasurys rally. In supply-side shocks, the impulse tends to be more inflationary, and equities and fixed income tend to move together.

Diversification is regime-dependent, not structural. Correlations can change quickly, and the right asset mix for diversification depends on the forward-looking correlation matrix. Treasurys did not help an equity investor in March, but they may in the next crisis.

Like most things in life, March Madness came and went. In the midst of every market panic, it can be tempting to parse every headline and oversteer. Most asset classes are now roughly back to where they started the year, with the exception of oil.