The Price of Borrow

How a retail-friendly broker may have cracked the opaque stock-loan borrow system

Shorting can be one of the most powerful tools in investing—essential for hedging, market-neutral portfolios, factor investing, and academic long–short research. Yet unlike the clean return series used in academic factor models, implementing a long–short portfolio in the real world has frictions.

Borrow rates—paid by the short seller to the lender—represent a hidden but significant drag on performance, and they are notoriously opaque. They are also an important part of the reason academic long–short portfolios routinely outperform implementable portfolios: the “true cost” of borrowing securities can materially erode returns, particularly in small caps or crowded shorts.

Given the economic importance of borrow costs, the opacity of the securities-lending market poses a real problem for allocators—especially smaller firms or individuals without the leverage of a large prime brokerage relationship.

In 2017, the Iowa Public Employees' Retirement System sued a consortium of banks, including BofA Merrill, Goldman, Morgan Stanley, JPMorgan, UBS, Credit Suisse, and their joint venture EquiLend. EquiLend is a joint venture of the major prime brokers, responsible for the central plumbing in the securities lending market, and the plaintiff alleged that the consortium “coordinated boycotts of [new electronic] platforms to keep the stock-loan market ‘in the stone age,’ preserving opaque pricing and supracompetitive fees.” In 2023 the defendants ultimately settled for $580M without admitting any wrongdoing.

If the Iowa Public Employees Retirement System feels taken advantage of by Wall Street, what chance does a small investment firm or a retail investor have of getting a fair shake? It turns out, thanks to Interactive Brokers, maybe a pretty good one.

Interactive Brokers (IBKR) is a global electronic broker built from the ground up around automation, cost efficiency, and direct electronic market access. A very convenient (and intentional) feature of IBKR is that they provide much of their data as a self-serve model. We aggregated IBKR’s borrow rates for US equities to compare against S&P Global's Securities Finance (formerly Markit) data—the industry standard benchmark for market-wide securities-lending transactions. S&P Global’s dataset is widely used in academic research and was central to damages modeling in the 2017–2023 antitrust litigation.

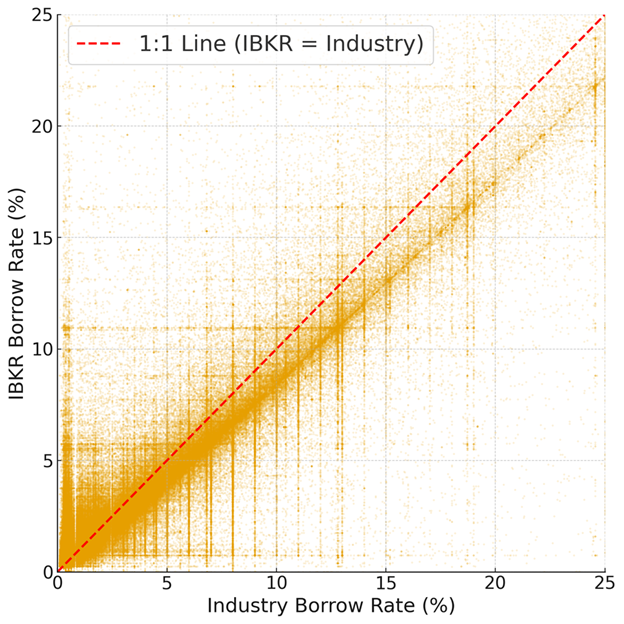

To see how IBKR compared, we regressed IBKR’s borrow rates against the benchmark data, matched by security and month.

Figure 1: IBKR Borrow Rates vs. Industry Borrow Rates

Source: S&P Global’s Securities Finance, Interactive Brokers, Verdad research

We can see a pretty noticeable trend that most of the data lives below the 45° line, fit through the origin. The regression has a beta of 0.96 and an r-squared of 0.8. Put simply, across all securities and all months, IBKR’s borrow rates tend to be slightly lower than the industry reference. In fact, if we exclude borrow rates below 1% (which generally indicate it is freely available to borrow), IBKR is cheaper than the industry rate about 72% of the time. This suggests IBKR’s pricing is at least competitive with, and often slightly better than, big-bank prime brokers. Which means IBKR is offering institutional-grade borrow pricing to even very small funds—something that would have been unthinkable twenty years ago.

This is great news for smaller investment firms, retail investors, and frankly shareholders of Interactive Brokers. And this story goes a long way to explaining why IBKR’s stock is up 380% over the last five years.