Peer Momentum

An introduction to indirect effects

Momentum—buying recent winners and selling recent losers—remains one of the most robust and persistent premia in global equity markets, more than thirty years after its initial documentation by Jegadeesh and Titman (1993). Unlike many published factors that fade after discovery, momentum has continued to deliver positive abnormal returns across geographies and asset classes.

At its core, a momentum strategy operationalizes a simple intuition:

Assets that have outperformed tend to continue to outperform, and assets that have underperformed tend to continue underperforming.

A leading explanation for this phenomenon is limited attention: markets adjust slowly to new information, especially when information is complex or arrives gradually. Traditional stock momentum relies exclusively on a firm’s own trailing returns as the proxy for “new information.” This is a direct effect.

But focusing only on a firm’s trailing performance misses a substantial portion of the information set. Firms compete, interact, and evolve within economic networks of suppliers, customers, complementors, and competitors. News affecting one firm often spills over to others. If markets incorporate these indirect signals with delay, then a firm’s future returns should be predictable from the performance of its peers. This insight motivates what we call peer momentum, a member of a broader class of indirect effect signals.

Industry Momentum: The Simplest Peer Set

To illustrate the concept, we begin with the simplest and most intuitive form of peer momentum: industry momentum. Instead of ranking firms based on their own trailing returns, we rank them based on the trailing returns of their industry peers.

For each stock, we compute traditional momentum over 3-, 6-, and 12-month windows (excluding the most recent two weeks to avoid short-term reversal), identify all firms in the same GICS industry, and compute the equal-weighted (EW) or cap-weighted (CW) average of their momentum scores. The composite peer momentum measures shown below blend the 3-, 6-, and 12-month windows together.

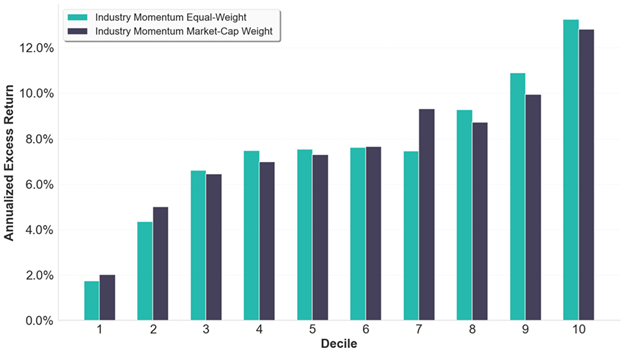

Figure 1: Decile Return Spread of Industry Momentum

Source: Verdad analysis. Note: Decile spreads report the average annualized 30-day forward local excess return of each decile. Universe: ~11K global equities (as of 2025). Sample period: 1996–2025. Industry Momentum Equal-Weight (EW) = equal weight given to each industry peer. Industry Momentum Market-Cap Weight (CW) = cap-weight given to each industry peer.

The spread between the top and bottom deciles is 11.4% (EW) and 10.8% (CW)—substantial evidence that a simple industry-peer momentum signal can predict future returns. These findings are consistent with early work by Moskowitz and Grinblatt (1999) and Asness, Porter, and Stevens (2001).

Crucially, industry peer momentum is largely uncorrelated with stock-level momentum. Even after residualizing on individual-stock momentum, the peer signal spreads returns in a comparable fashion.

Beyond Industry: Alternative Peer Definitions

Industry membership is only one way to define a peer set. A broad literature documents information spillovers along multiple types of linkages:

• Customer–supplier networks (Cohen and Frazzini, 2008)

• Production complementarities (Lee et al., 2024)

• Technological similarity (Lee et al., 2019)

• Shared analyst coverage (Ali and Hirshleifer, 2020)

• Text-based product similarity (Hoberg and Phillips, 2016)

The central intuition is consistent across settings. Firms connected through real economic or informational relationships are exposed to similar news, risks, and shocks, and markets incorporate these indirect signals only gradually.

A More Sophisticated Example: Biotech Peer Networks

A more sophisticated example comes from biotechnology, where traditional industry codes provide little insight into the true economic relationships between firms. In biotech, value is determined not by broad sector labels but by what a company is researching, which diseases it targets, and which technological modalities it employs. For instance, two companies classified under the same GICS biotechnology code may share no scientific overlap—one might focus on oncology while another works on metabolic disorders—while two firms placed in different GICS sub-industries may both be developing GLP-1–based therapies and therefore share similar scientific risks and regulatory pathways.

Over the last year, we have constructed a comprehensive clinical trials database. Using this data, we can construct a measure of similarity along two dimensions: therapeutic focus (condition) and technological approach (intervention).

The method considers the entire R&D portfolio, not just the most recent trials, weighted by clinical relevance, recency, and phase progression. Firms pursuing similar therapies with similar technologies tend to be exposed to the same scientific developments, competitive dynamics, and regulatory events.

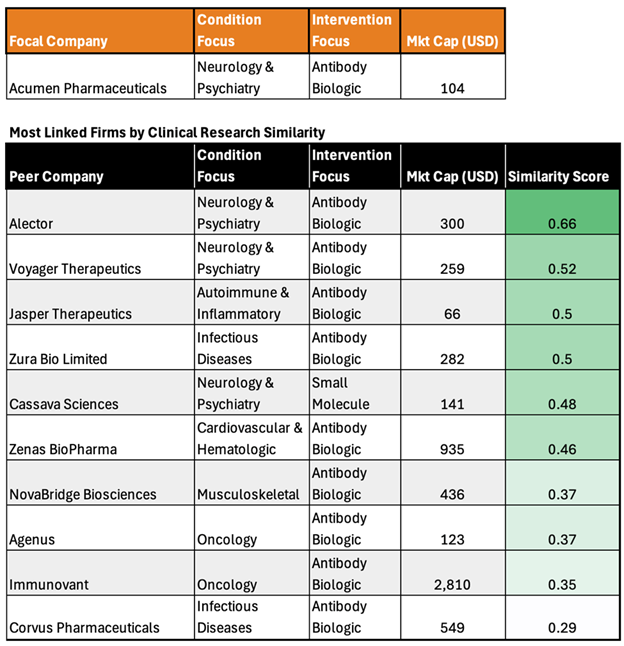

The table below illustrates the peer set for a representative focal company. “Condition Focus” and “Intervention Focus” denote the program that scores highest under our pipeline weighting scheme, while the similarity score itself is computed from the full distribution of R&D activity.

Figure 2: Biotech Linked Firms

Source: Verdad Biotech Database. Similar firms identified by comparing clinical research pipelines. Analysis includes US-based biotech companies. Condition Focus and Intervention Focus are derived from the most significant product in each company’s pipeline, with priority given to products in more advanced clinical phases and with more recent results.

By constructing peer momentum using clinically defined relationships rather than broad industry codes, we better align the peer set with the underlying economic reality of how information and value are created in biotech.

Traditional momentum and peer momentum can be used in combination to spread returns. Within biotech, we find that peer momentum adds predictive power beyond stock-level momentum, strengthening forecasts and improving signal robustness in a domain where traditional financial metrics are often uninformative.

As industries become more interconnected through shared technologies, supply chains, and regulatory decisions, capturing indirect effects becomes increasingly essential. At Verdad, we are extending this research across sectors using richer datasets and applying machine learning and natural language processing to quantify how information travels between firms.

Peer momentum is not a replacement for traditional momentum. It is a practical extension that fills the gaps created when economic relationships are complex, intangible, or evolving and when information propagates in ways standard classifications fail to capture.