The Inferno

How biotech experts can guide us

By: Greg Obenshain, Daniel Rasmussen, and Anton Wintner, M.D.

This is the third installment of our series on biotech. To read the full white paper, click here.

As Dante wandered in confusion until Virgil appeared to lead him, so too do most investors enter biotech in a kind of darkness—surrounded by unfamiliar science, opaque data, and no revenues to anchor valuation.

In the introduction, we told the story of Pharmacyclics. What we did not emphasize was the role of biotech specialist funds as its guides. In 2009, when Pharmacyclics was a $1.28 stock with only early BTK inhibitor data, specialists such as OrbiMed, Quogue Capital, and later Baker Brothers recognized its potential and began buying. Within a year, at least three expert groups had invested, and a few years later the company was acquired for $261.25 per share: a classic example of how great science is often identified first, and rewarded most, by specialist investors who quickly cluster into good ideas.

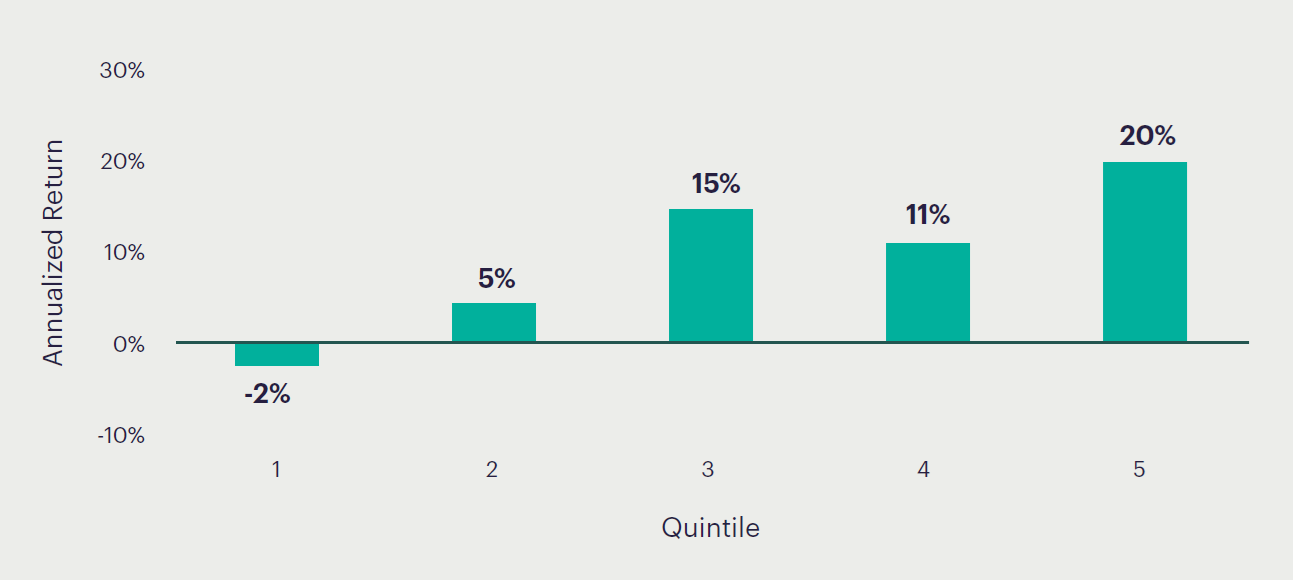

Their collective judgment shows up clearly in the data. When we sort biotech stocks by how heavily they are owned by biotech specialist funds—from the least owned (quintile 1) to the most owned (quintile 5)—a striking pattern emerges. The chart below illustrates how specialist conviction maps directly into returns.

Figure 5: Biotech Company Returns by Biotech Specialist Fund Concentration Quintile

Sources: SEC, S&P Capital IQ, Verdad Analysis. September 2013 – October 2025. Excludes companies not held by any fund.

In general, the higher the concentration of biotech specialist funds, the better that stock performs. Conversely, if no biotech specialist funds own a stock (generally true for quintile 1), returns have been poor.

Because biotech specialist funds typically hold positions for nearly two years—and because the strongest signals come when multiple specialists own the same stock—their activity shows up consistently in 13-F filings. As a result, even with a two-month reporting lag, the 13-F data remains both robust and highly informative.

One interesting twist to our findings on specialist ownership is that 72% of specialist fund exposure is in large stocks. This is likely because multi-billion-dollar funds cannot just invest in small and medium stocks. But specialists are best at identifying return opportunities in small stocks. In the smallest third of biotech stocks, the stocks with the highest concentration of specialist ownership have nearly 30% returns in our historical data versus near-zero returns for stocks with no specialist concentration. The implication is that smaller funds have a structural advantage if they can focus on smaller opportunities.

But biotech specialist funds are not the only specialists we should pay attention to. There are two other sets of investors who also provide expertise: company insiders and short sellers.

Company insiders are the best positioned to understand the prospects of a company. There is a rich academic literature that shows that company insider transactions contain useful information about stock returns. This is especially true if the insider transactions are filtered for high-information trades, such as buys versus sales (most insiders are natural sellers), reversals of previous trade directions, transaction clustering, and purchases by knowledgeable parties such as CFOs.

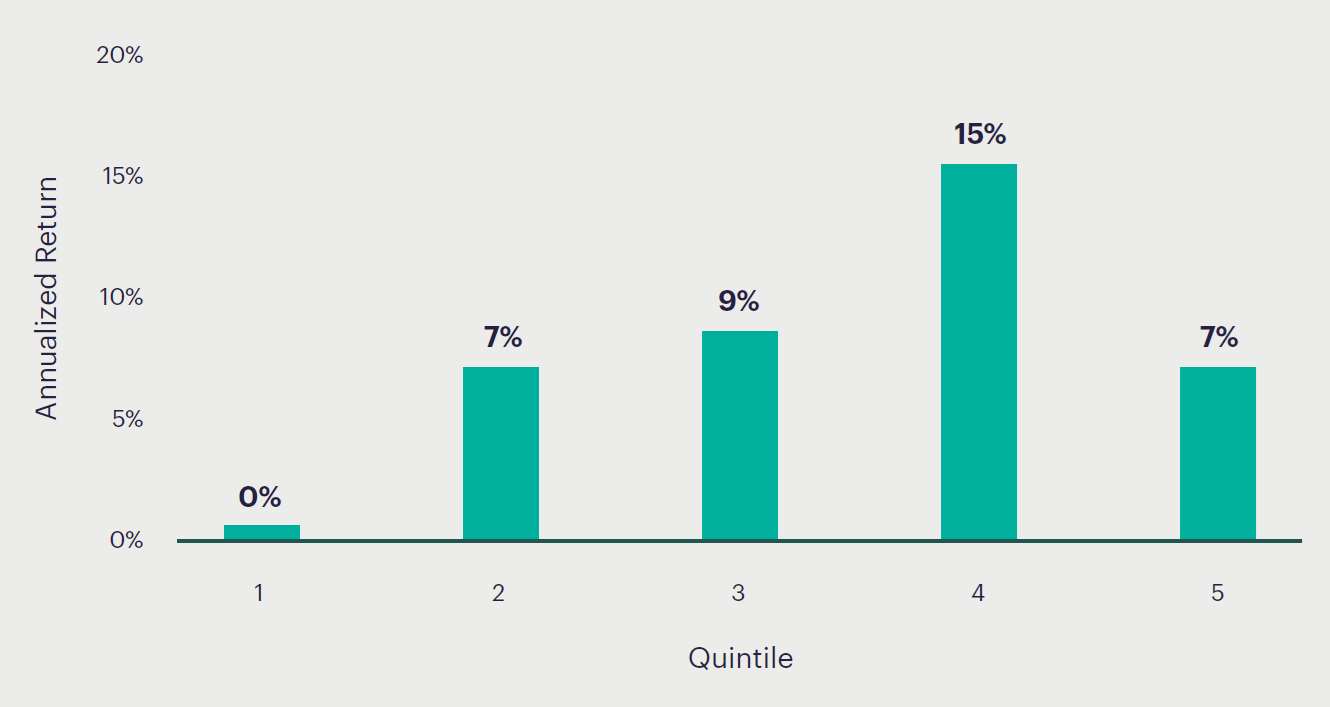

It turns out that insider transactions convey information in biotech as well. Below we show how the strength of insider trade signals spreads returns. Quintile 1 contains the companies where the insider trades are most bearish and quintile 5 contains the trades where the trades are most bullish.

Figure 6: Biotech Company Returns by Insider Trade Signal Quintile

Sources: SEC, S&P Capital IQ, Verdad Analysis. September 2013 – October 2025. Excludes companies with no insider trades.

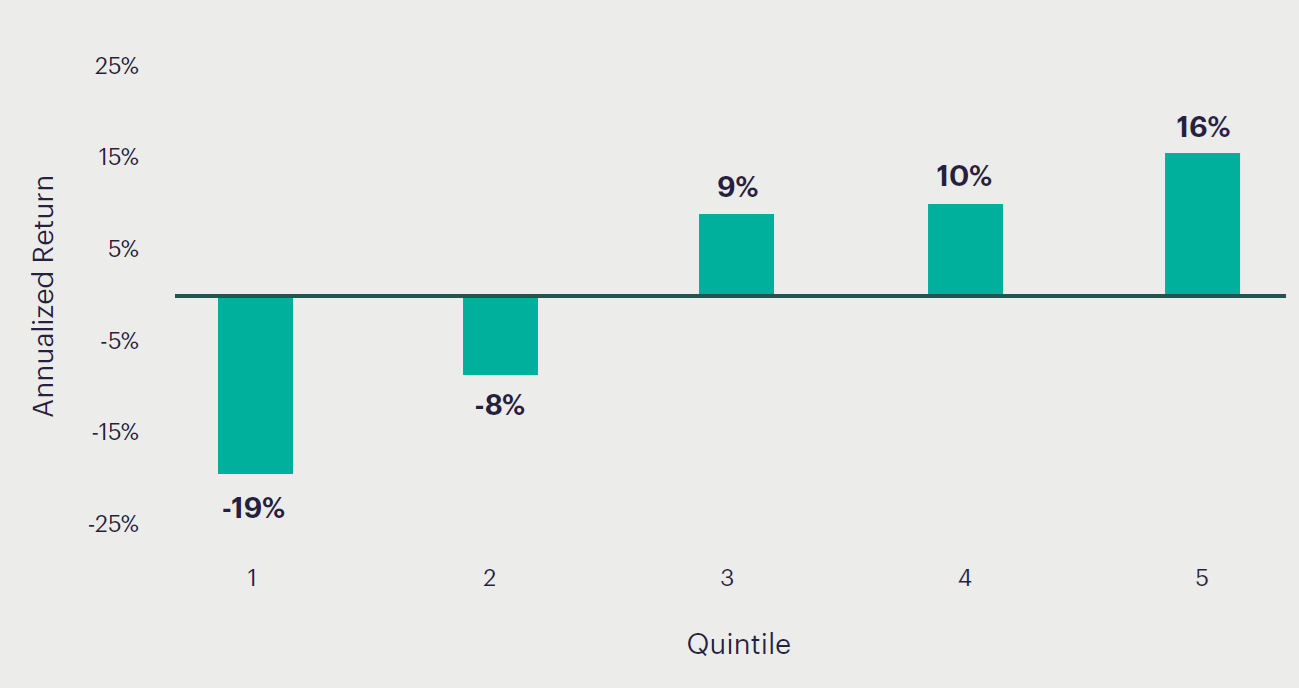

Short sellers, who tend to be very active in this sector, provide another excellent source of specialist signals in biotech. Below we show how our short interest metric spreads biotech returns. In this case, quintile 1 represents the most shorted companies and quintile 5 the least shorted companies.

Figure 7: Biotech Company Returns by Short Interest Metric

Sources: SEC, S&P Capital IQ, Verdad Analysis. September 2013 – October 2025.

It turns out that short sellers are good at identifying potential losers and at avoiding winners. This data is more broadly available for all stocks than insider trading data and more immediately available than specialist data. In a sector where many companies fail, short sellers are guides that prove to be equally valuable to biotech specialist funds as company insiders.

Biotech is a challenging industry, but expertise provides a path—specialist biotech funds, insiders, and short sellers each illuminate part of the terrain. In Dante’s words, after guidance through the underworld, “then we came forth, to see again the stars.” Expertise does not guarantee victory, but it brings investors out of the darkness and closer to the truth.