Japan's Big Equity Bet

How Japan has created a sovereign wealth fund with borrowed money

By: Naoki Ito, Kosuke Mikitani, Yasumasa Suzuki

Japan’s government debt exceeds 230% of GDP, by far the highest ratio among advanced economies, the product of having run primary deficits for decades. An aging population with rising pension and health care costs adds to the fiscal problem.

But our friend and Stanford professor Hanno Lustig has coauthored a new paper arguing that Japan is far better off than this scary statistic sounds as a result of a brilliant policy move by former prime minister Shinzo Abe. Starting in 2012, the Bank of Japan began buying domestic equities at scale. In 2014, the Government Pension Investment Fund (GPIF), the world’s largest public pension manager, doubled its equity allocation target to 50% of its portfolio.

Japan also built something few countries have ever attempted: a de facto sovereign wealth fund financed at near-zero borrowing costs. “Japan funds itself cheaply at short-duration, floating-rate liabilities and uses the public balance sheet to hold long-duration, risky assets,” Lustig and his coauthors write. Japan has created a “sovereign wealth fund fueled by borrowed money.”

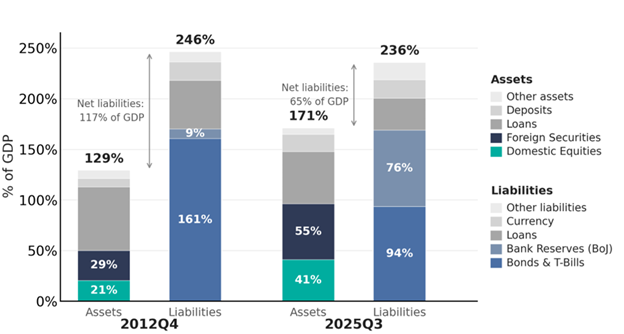

This strategy has been an enormous success, as both domestic and foreign equity markets surged. Today, the consolidated public sector holds financial assets worth 171% of GDP as of 2025, with more than half in equities and foreign securities, as shown in Figure 1. The authors estimate that from 2013 to 2023 the public sector earned roughly 4.6% above its funding costs annually—equivalent to about 6% of GDP per year—substantially reducing net liabilities.

Figure 1: Consolidated Public Sector Balance Sheet Composition (2012 vs. 2025)

Sources: Japan Flow of Funds, National Accounts of Japan, Chien/Du/Lustig, Financial Times

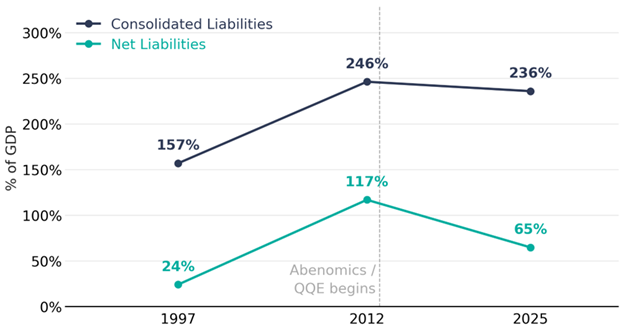

The authors estimate that, without the shift to risky assets, net liabilities would have exceeded 180% of GDP by 2024. Instead, Japan’s net liabilities fell from 117% of GDP in 2012 to 65% in 2025, even as Japan ran primary deficits in every year of that period.

Figure 2: Gross vs. Net Consolidated Public Liabilities (% of GDP)

Sources: Japan Flow of Funds, National Accounts of Japan, Chien/Du/Lustig, Financial Times

That improvement came from the return spreads on assets accumulated through a carry trade run at a national scale. Of course, the trade cuts both ways: higher funding costs or a major equity bear market would weaken the same balance sheet that rising asset prices have repaired.

The Japanese government thus has a massive incentive to keep the domestic equity market booming. Japanese equity returns seem to provide a direct solution to the country’s fiscal problem. The public sector holds domestic equities worth 41% of GDP as of 2025, distributed across public pension funds (14%), the BoJ (13%), and other public institutions. If Japanese companies raise returns on capital and equity valuations improve, the state’s asset base strengthens alongside its fiscal revenues.

This is why corporate governance reform, led by the government and the TSE, is macroeconomically significant. In March 2023, the TSE requested that listed companies adopt management “conscious of cost of capital and stock price,” asking boards to assess profitability, market valuation, balance-sheet efficiency, and capital allocation, and to disclose improvement plans where needed.

That is the right pressure point. Japan’s traditional corporate model tolerated excess cash, cross-shareholdings, low returns on equity, and valuations persistently below book. These are not merely corporate inefficiencies. In Japan’s fiscal context, they are a drag on the state’s own balance sheet. Idle capital inside corporations can simultaneously suppress productivity, wages, tax revenues, and the market value of the public sector’s equity portfolio.

Japan’s corporate governance reforms are often described as micro-level housekeeping: unwind cross-shareholdings, raise returns on equity, deploy excess cash, improve disclosures. But they are better understood as macro policy. When the state owns a large slice of the market and funds itself cheaply, higher equity prices are not just good for shareholders—they strengthen the sovereign balance sheet itself. In that sense, Tokyo is not merely reforming corporate Japan. It is managing one of the world’s largest leveraged national investment portfolios.

Acknowledgements:

Kosuke Mikitani is a junior at Brown University studying computer science and economics. His experience as an engineer at several technology companies and as a private equity analyst at Blackstone has shaped his interest in both technology and finance. He enjoys discussing macroeconomics, the Japanese corporate landscape, soccer, and golf.

Yasumasa Suzuki is a senior studying economics at Keio University and Sciences Po Paris. He interned with Blackstone’s private wealth team and will intern with Bank of America’s investment banking division this summer. He is interested in Japan’s economic dynamics, particularly corporate governance reform, and plans to pursue a career in finance.