Japan's Bank Revival

Value investing in a scale-driven industry

By: Naoki Ito

During Japan’s ultra-low interest rate era, bank stocks were abandoned by investors and generated negligible returns. Almost all banks traded persistently and deeply below book value, reflecting structurally depressed profitability and widespread skepticism that their earnings power would ever normalize.

That regime finally began to change. After 17 years without a rate hike, the Bank of Japan (BoJ) ended its negative interest rate policy in March 2024 and began raising rates. By December 2025, the policy rate had risen to 0.75%, the highest level in three decades. BoJ has signaled that further rate normalization is likely.

Bank stocks have, for the first time in decades, shown signs of revival, driven by expectations of expanding net interest margins in a rising-rate environment. Over the past three years, the TOPIX Banks Index has compounded at 47% annually in yen terms, significantly outperforming the broader TOPIX, which returned 22%.

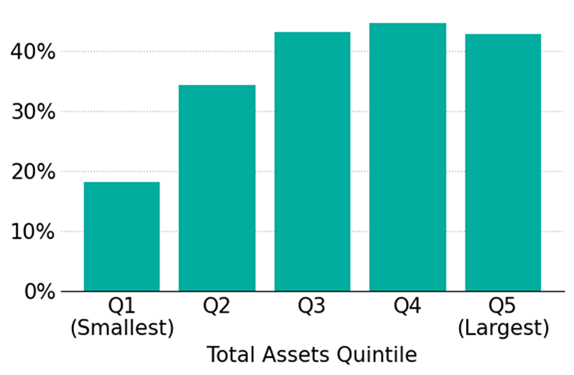

However, performance has been far from uniform. The smallest banks, as measured by total assets, have delivered materially worse results, as shown below. We refer to this as the scale factor and distinguish it from the traditional size factor.

Figure 1: Average 3Y CAGR of Japanese Bank Stocks by Scale (12/1/2022 - 11/30/2025)

Sources: S&P Capital IQ, Verdad analysis. Note: Delisted stocks are excluded.

While the precise drivers of the return spread associated with scale are difficult to isolate, the structural differences between large, internationally active banks and smaller regional banks are unmistakable. Banking is inherently scale driven: the larger the balance sheet, the greater the earnings leverage to net interest margins, which are now expected to expand as interest rates rise.

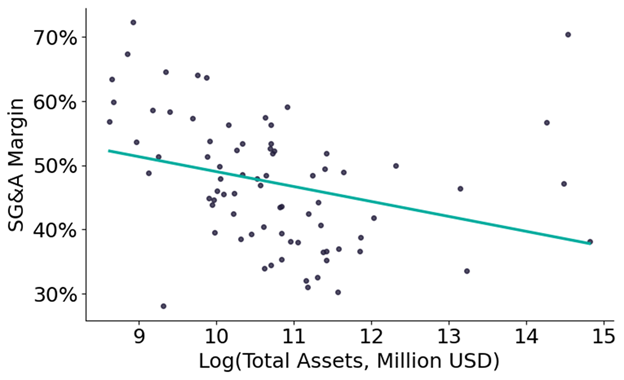

This scale advantage also tends to translate into higher operating efficiency, as fixed costs can be spread over a larger asset base. Banks typically assess efficiency using the overhead ratio, defined as total operating expenses divided by total revenue. Here, we proxy operating efficiency using SG&A margin and plot it against scale below. Efficiency is closely linked to profitability: across Japanese banks, the cross-sectional correlation between SG&A margin and ROE is −0.72.

Figure 2: Distribution of Japanese Banks by Efficiency and Scale (11/30/2025)

Sources: S&P Capital IQ, Verdad analysis. Note: Observations outside 1.5× the interquartile range are excluded.

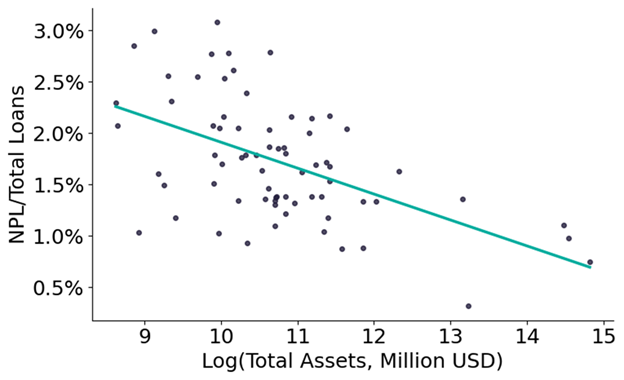

Smaller banks, by contrast, are tightly tied to regional economies, operate with limited diversification, and face a narrower set of lending opportunities. Their growth potential is constrained by demographic decline and limited economic dynamism in their home regions, while many operate under an implicit mandate to support local small and medium-sized enterprises. As a result, smaller banks tend to carry riskier assets, as evidenced by a higher ratio of non-performing loans to total loans (NPL/TL), as shown below.

Figure 3: Distribution of Japanese Banks by Asset Quality and Scale (11/30/2025)

Sources: S&P Capital IQ, Verdad analysis. Note: Observations outside 1.5× the interquartile range are excluded.

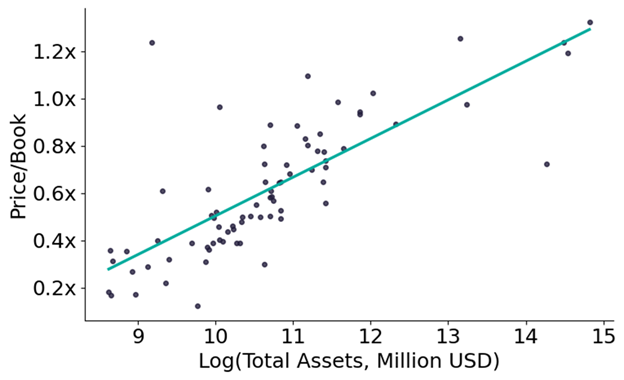

Together, these factors place smaller banks at a persistent disadvantage in profitability, asset quality, growth, and ultimately shareholder value. It is therefore unsurprising that bank valuations are closely tied to scale, as illustrated below using price-to-book (P/B) ratio.

Figure 4: Distribution of Japanese Banks by Valuation and Scale (11/30/2025)

Sources: S&P Capital IQ, Verdad analysis. Note: Observations outside 1.5× the interquartile range are excluded.

The key takeaway is that the scale factor provides an economically intuitive framework for evaluating Japanese bank stocks, as it captures many of the systematic exposures banks face for structural reasons.

While the scale factor has been the dominant driver of recent return dispersion among Japanese banks, other factors remain informative. In particular, the core principle of value investing still applies: attractive returns can be earned by buying inexpensive stocks with strong underlying fundamentals.

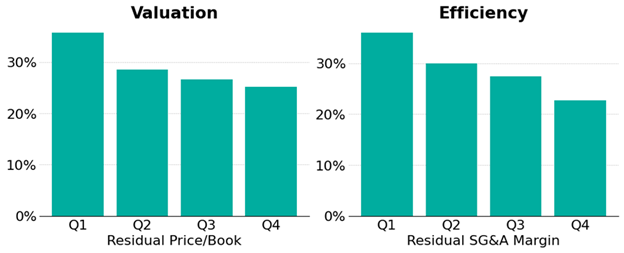

One way to illustrate this is to orthogonalize factors with respect to scale. For each year, we regress these metrics on the logarithm of total assets for listed Japanese banks and examine the residuals—that is, the difference between observed factor values and those implied by scale. Using P/B as an example, rather than asking whether a bank appears cheap on an absolute basis, we ask whether it is inexpensive relative to what its size would predict.

The figure below presents average one-year forward returns by quartile of these scale-neutralized factors. A clear return spread emerges: conditional on scale, banks with lower P/B (lower valuation) and lower SG&A margins (higher efficiency) tend to deliver higher forward returns.

Figure 5: Avg. 1Y FWD Total Returns of Japanese Banks by Factors Conditional on Scale (7/1/2022 - 6/30/2025)

Sources: S&P Capital IQ, Verdad analysis

By incorporating this insight and constructing a composite measure that combines size with the valuation and efficiency factors, we can improve the forward return spread relative to a naïve scale-based long-short portfolio (long the top quintile and short the bottom quintile).

Figure 6: 1Y FWD Total Return Spread Comparison (7/1/2022 - 6/30/2025)

Sources: S&P Capital IQ, Verdad analysis

The rally in bank stocks may continue as monetary policy normalization progresses. Yet it is difficult to assess how much upside remains from further rate hikes or how such changes will affect banks differently, given that Japan is now operating in a macroeconomic environment it has not experienced in more than three decades. It also remains uncertain whether investors in small regional banks—many of which still trade at extremely low valuations—will ever enjoy a true heyday.

That said, bank fundamentals appear to be structurally determined by scale, and those differences are likely to persist. An interesting direction for further research would be to examine whether similarly scale-dominated dynamics exist in banking sectors outside Japan, and how the scale factor performs across different macroeconomic environments, particularly those characterized by changing interest rate expectations. In the meantime, even within this new regime, disciplined investors who understand these industry-specific dynamics may still be able to identify more attractively valued banks based on fundamentals.