Overweight the Mag-7?

The Mag-7 now account for 40-45% of S&P500 volatility

Over the last year, the S&P 500 has had 14% volatility, while the MSCI All-Cap World Index (ACWI) has had volatility of 11%. These numbers are not that notable in their own right, relative to the longer history of each series, but they belie a more complicated story under the surface.

During that same period, the Mag-7 combined has had volatility of 20%, while the “S&P 493” (ex. Mag-7) has had volatility of 12% and the ACWI (ex. Mag-7) has had volatility of 10%.

The Mag-7 currently accounts for 30% of the S&P 500 by market-cap weight, and 17% of the ACWI. Despite their outsize impact on returns, given the significant weight of these seven companies, they have an even more outsize impact on index volatility, given their elevated volatility.

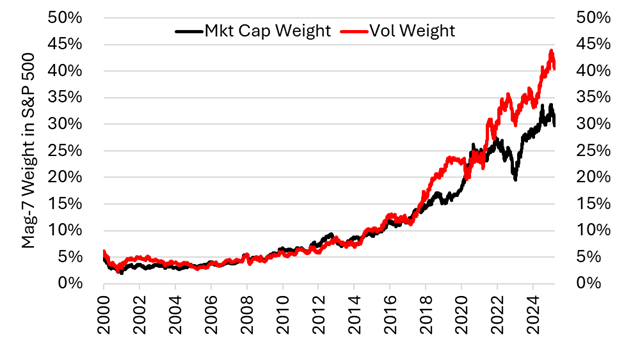

We can estimate the impact of the Mag-7 on index volatility in a couple different ways, which generally give the same answer. The simplest method is to calculate the volatility of the indices excluding the Mag-7 returns and weights, and then scale that volatility by the market-cap weight of the remainder of the index and compare the difference. Astoundingly, this approach suggests that the Mag-7 account for 40-45% of S&P 500 volatility, and 25% of ACWI volatility. This gap between the volatility contribution and the market-cap weight is now at the widest level in 25 years.

Figure 1: Mag-7 Market-Cap Weight and Volatility Weight for S&P 500

Source: Verdad analysis

The growing influence of the Mag-7 on index returns over the last 15 years has been obvious and undeniable. But what has been a little less obvious is the outsize impact that the Mag-7 has had on index volatility, especially since 2020.

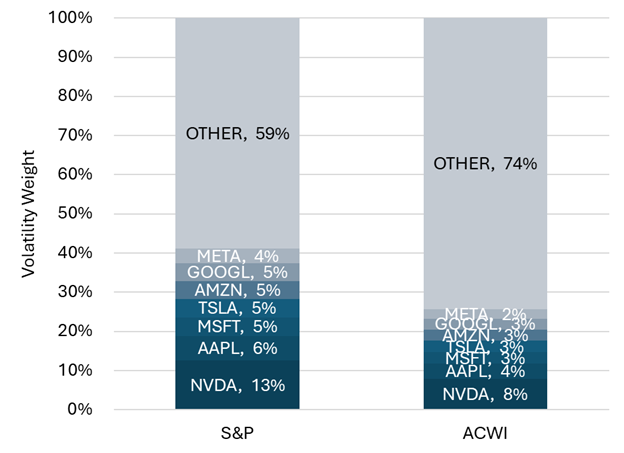

We do not mean to imply that the S&P 500 volatility would be 6-7%. The volatility of the “S&P 493” was 12%. But investors buying the S&P 500 today are getting both the Mag-7 at a 30% market-cap weight and a 40-45% volatility weight. More specifically, we can examine the volatility weight of each constituent of the Mag-7 within both the S&P 500 and the ACWI.

Figure 2: Vol Contribution Weight of Mag-7 Constituents for S&P 500 and ACWI

Source: Verdad analysis

Investors buying the S&P 500 or the ACWI today are getting NVDA at a 13% volatility weight and AAPL at a 6% volatility weight. This isn’t inherently good or bad, but investors buying either index need to be going in with eyes wide open about what they’re getting.

Going forward, index performance may not be determined by whether the US and global economies hum along but by whether the dominant tech leaders of today hold the keys to unlocking the potential of tomorrow’s next great innovation, AI. Until the answer is decided, the major indices will be yanked around by changing perceptions of whether the Mag-7 will win the AI race and reap the rewards.

The phrase "the tail wagging the dog" comes readily to mind—but at this point, it's unclear which is the tail and which is the dog. Is the Mag-7 the tail and the tens of thousands of globally listed equities the dog, or vice versa?