The Acquirer: Hiroshi Nojima, Nojima Corporation

The story of how Hiroshi Nojima turned a sleepy family business into one of the top performers on the Tokyo Stock Exchange

By: Dan Rasmussen and Naoki Ito

After the 1980s bubble, the Japanese equity markets stagnated. Few stocks made money, and most CEOs got used to watching their share prices languish on the Tokyo Stock Exchange.

But a few Japanese CEOs were able to buck this trend, to find a bold way to make money for shareholders and make their stocks defy the gravity of the Japanese markets. These are their stories.

Inspired by Will Thorndike’s book The Outsiders, we looked at every Japanese company with a CEO who had served over 15 years and delivered exceptional stock market returns during their tenure. We studied their values, their actions, their philosophies, trying to distill the essential lessons that defined greatness among these leaders.

These CEOs might not be household names. They might not be talked about in the halls of the stock exchange. But they should be. For they each achieved greatness where thousands struggled to achieve anything better than mediocrity.

And today, as the Tokyo Stock Exchange pushes reforms to encourage better returns for Japanese equities and cure the chronic undervaluation of corporate Japan, we believe these stories offer valuable insights into effective strategies for creating shareholder value.

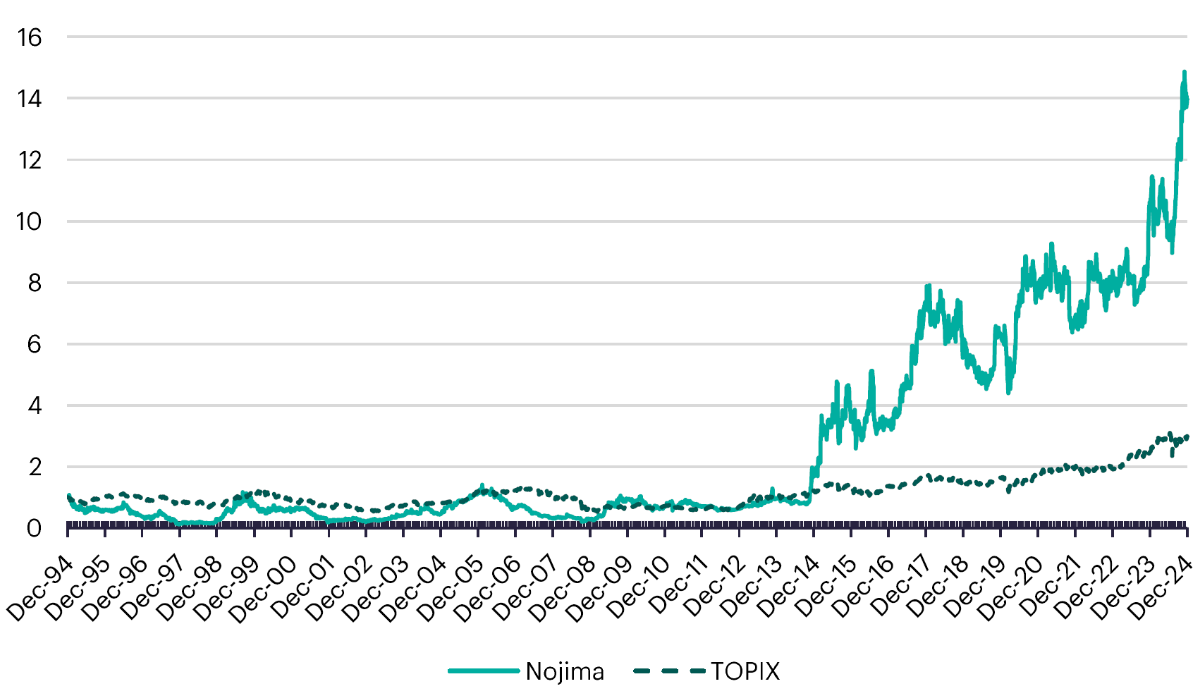

We start our project by profiling Hiroshi Nojima, who has been leading his family company, Nojima Corporation, since its IPO in 1994. Over the past decade, Nojima’s stock price compounded at a staggering 25%, making it one of the best-returning stocks in the Japanese market under the driving vision of Hiroshi.

This is the story of how he turned a sleepy family business into one of the top performers on the Tokyo Stock Exchange. Perhaps the most interesting part of the story is that Hiroshi wasn’t always good at making money; rather, for the first 20 years after the IPO, his company’s stock returned no better than the TOPIX index. But Hiroshi broke out of this stagnation, changed the fate of Nojima, and set a standard for value creation that deserves to be legendary.

Figure 1: Full History of Cumulative Total Return of Nojima and TOPIX (1994-2014)

S&P Capital IQ, Bloomberg

What sets Hiroshi apart is his bold yet disciplined investment approach. When competitors scaled back expansion amid caution during the financial crisis, he seized the opportunity to acquire prime retail properties at favorable prices, expanding Nojima’s total sales floor area by 30%. When the prospective return from investing in Nojima’s existing business appeared insufficient, Hiroshi took calculated risks by acquiring struggling companies in adjacent industries and improving their cash flow, aiming to quickly recover the invested capital for further reinvestment.

Hiroshi bet that acquiring companies through substantial debt—leveraging Japan’s low-interest rates—would generate more cash flow than investing in organic growth or hoarding cash on the balance sheet. Hiroshi’s success underscores an opportunity for Japanese companies to pursue transformative acquisitions, particularly given the abundance of firms trading below book value. Acquiring established businesses with scalable earnings potential offers a faster and more capital-efficient path to growth compared to investing in new ventures from scratch, especially when these targets can be purchased at attractive valuations.

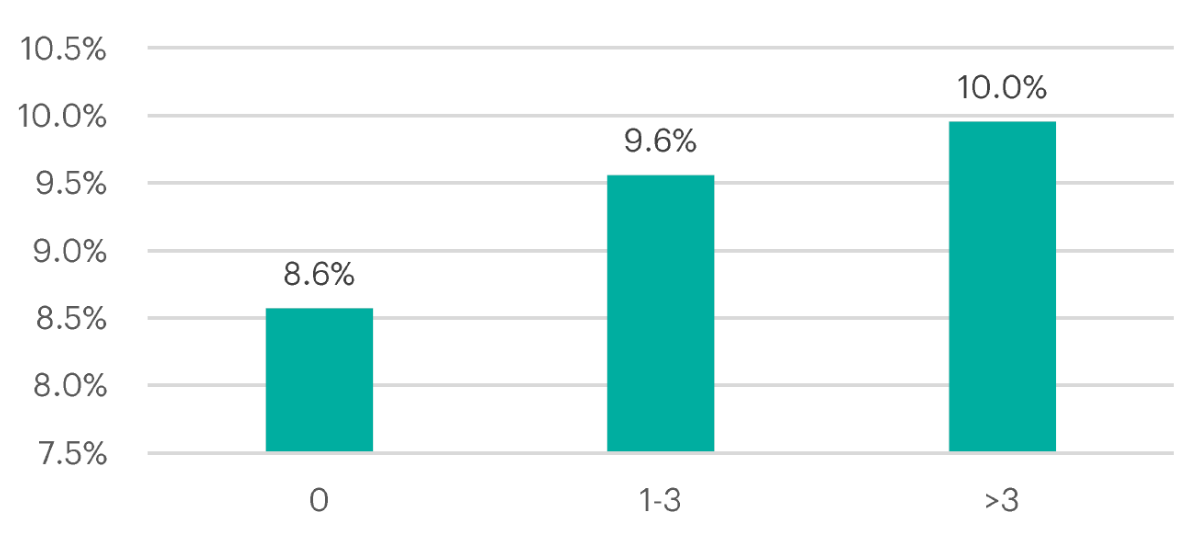

Across Japan, serial acquirers like Nojima have outperformed companies that do not engage in acquisitions. The chart below illustrates the average compounded annual growth rates of stock prices, categorized by the number of acquisitions Japanese companies made between 2015 and 2024.

Figure 2: 10Y Average Compounded Annual Growth Rate by the Number of Acquisitions (Japan, 2015-2024)

Source: S&P Capital IQ, Verdad Analysis

Over a decade, the annual difference of 1.4% between companies that made more than three acquisitions and those that made none compounds to a difference of approximately 30% in total returns.

Hiroshi’s leadership also demonstrates the importance of discipline in shareholder returns. Despite facing struggles during the first half of his tenure and financial challenges associated with major acquisitions, Hiroshi never cut dividends. Instead, he consistently increased them in line with earnings growth. This unwavering commitment to rewarding shareholders cultivated long-term trust and underpinned the company’s robust stock performance.

For CEOs grappling with low growth and stagnant stock prices, Hiroshi Nojima’s journey offers actionable lessons. It’s never too late to make a bold move—Hiroshi was in his mid-60s when he made the largest acquisition of his career. Strategic acquisitions, when made at the right price with strong return potential, can reshape a company’s trajectory. By embracing risk, reinvesting with discipline, and prioritizing shareholder returns, Japanese companies can unlock new growth avenues and fulfill the fundamental promise of public companies: delivering exceptional and sustained value to shareholders.