High Yield, High Volatility

Business development corporations are hyper-cyclical investments

By: Greg Obenshain & Ethan Weinstein

Every cycle we receive breathless warnings of the imminent implosion of the high-yield market, and with good reason. The junkiest bonds tend to sell off much more dramatically than investment-grade debt and often prove to be the canary in the coal mine for the broader economy. This has been true since the earliest days of the high-yield market. The buyout boom of the 1980s led to the high-yield bust of the early 1990s, when the average price of bonds dropped to 70 cents on the dollar and the yield reached 21%. That performance was repeated in the great financial crisis and has been repeated to a lesser extent in every other crisis.

But this time is different. Not because high-yield spreads aren’t vulnerable, but because the greatest risks in credit markets now reside in loans, not bonds. Whereas the early leveraged buyouts were financed by high yield, most buyouts are now financed by loans. As the buyout business has boomed over the last decade, so has the loan market. As we argued in "The Loan Engine," much of the lending in the loan market is risker than in the high-yield market.

For the most part, none of this affects public investors. Most loans are made through private credit funds or through hedge funds. But there is a notable exception: Business Development Corporations (BDCs).

Created in 1980 through the Small Business Investment Incentive Act, BDCs are companies specifically set up to make loans to US small businesses. So long as they distribute 90% of their taxable income as dividends to shareholders, they pay no corporate taxes. And for retail investors looking for yield, BDCs often offer yields in the high single digits and sometimes over 10%.

Public BDCs raise about half their investment funds from public shareholders and the rest through borrowing. Most assets in BDCs are loans to small businesses. In some cases, these are directly originated by the BDC, but, increasingly, these loans are financing the booming buyout market and are loans funding private equity deals. This makes BDCs one of the few ways that retail investors can get access to private equity debt. And because BDCs use leverage, the performance of these vehicles is highly sensitive to the loan sector.

Below we show the average asset composition of 10 large public BDCs.

Figure 1: Asset Composition of Select BDCs

Source: Company filings, Verdad Analysis.

BDCs: ARCC, AINV, HTGC, ORCC, FSK, CION, CGBD, PFLT, PSEC, MAIN

The composition is relatively conservative, with over 70% of assets in secured debt, which is typical of BDCs. But while it is secured, almost all of it is below investment grade (high yield), as would be expected of loans to small companies.

BDCs earn income and gains on their investments, and 2021 was a very good year for BDCs. Below we break down the 2021 investment returns for the 10 large BDCs from Figure 1.

Figure 2: Average Return on Investment for 10 BDCs

Source: Company filings, Verdad Analysis.

BDCs: ARCC, AINV, HTGC, ORCC, FSK, CION, CGBD, PFLT, PSEC, MAIN

The BDCs in our sample earned 7.7% interest on their investments. This is relatively high, considering that the single-B high-yield index averaged a 4.5% yield during 2021. BDCs are earning premium yields for both risk and illiquidity. They earned another 1% yield from fees on transactions and a huge 4.2% on price gains from investments. Of these, interest, dividends and fees are relatively stable, but gains are not. That same number was -4.8% in 2020, so we also show a more normalized gain of 1%. In both cases, BDCs earn a relatively high return of 7-9% on their investments.

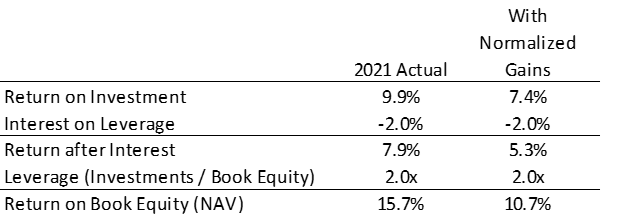

But the dividend yield to the retail investors is even higher because of leverage. Below we show how a BDC’s return on investment flows through to the equity.

Figure 3: 2021 Return on Equity for BDCs

Source: Company filings, Verdad Analysis.

BDCs: ARCC, AINV, HTGC, ORCC, FSK, CION, CGBD, PFLT, PSEC, MAIN

Even if you normalize gains, BDCs return over 10% to the equity. And indeed, the average dividend yield for these BDCs is around 10%, with many paying special dividends this year due to the high gains from 2021.

So far, BDCs seem like a very attractive investment. But high yields very rarely come without risk. As we wrote in "Fool’s Yield," high yields often come with higher losses. And indeed, the higher yields on BDCs do not necessarily lead to higher returns. S&P has tracked a market cap-weighted BDC total return index since December 2004. Over the life of the index, the annualized total return has been 6.2% while the high yield index has returned 6.1%.

Figure 4: S&P BDC Total Return Index vs. Bloomberg Barclays High-Yield Index

Source: Bloomberg. Last data point is June 15, 2022.

The BDC index has barely beaten high yield, despite dividend yields higher than the yield on the high-yield index. The chart above hints at the problem. BDCs are plagued by higher losses because they make riskier investments, and they have leverage that magnifies those losses. When the market gets nervous and high yield sells off, BDCs sell off a lot more. The higher-yielding, less-liquid investments become much scarier in bad times.

Below is the history of the price-to-book value of the S&P BDC Index since data became available in 2014. Despite high dividend yield, currently 9.8% on the index, BDCs tend to trade below the book value of their assets, a convincing sign that the market is pricing the risk of loss.

Figure 5: S&P BDC Index Price to Book

Source: Bloomberg

So how should an investor think about BDCs? As a buy-and-hold investment, they have delivered returns comparable to the high-yield index with far more volatility. And there is good reason to believe that this volatility will continue. BDCs are in the middle of the private credit lending boom and the private equity lending boom. Lending booms are not great places to invest, as that is where mistakes are often made. If we have a credit sell-off, BDCs may suffer more than high yield. But the silver lining is that, in the depths of a crisis, BDCs have proven to be terrific investments. While they may suffer outsize losses, when you buy an investment portfolio of mostly secured loans at 60-70 cents on the dollar, you have a good chance to win.

Using our definition of the business cycle stages, which we derive from the high-yield spread, we can see that, since its inception at the end of 2004, the S&P BDC index has delivered much higher average forward returns starting in recoveries and much lower return across the rest of the cycle.

Figure 6: BDCs Deliver Most of Their Returns in Market Recoveries

Source: Bloomberg, Verdad analysis

The high yields on BDCs come with a cost: huge drawdowns into recessions. But when their blood is in the streets, they can be terrific cyclical investments.

Acknowledgement: Coauthor and Verdad intern Ethan Weinstein is a member of the class of 2024 at Dartmouth, where he is studying both mathematics and economics. He is also involved in the Dartmouth trading club and is the business lead of the Dartmouth formula racing team. Ethan is seeking internship opportunities in finance for next summer.