Accosting Transactions

Trading costs are a barrier that limit every manager's ability to exploit arbitrage opportunities at scale.

By: Brian Chingono

In small-cap equity markets, rising scale brings trading cost disadvantages. This makes smaller players (often newer entrants) better able to capture systematic factor premiums. Yet we don't often spend time talking here about the actual brass tacks of investing in the stock market.

While reading about transaction costs in equity trading might seem a bit dull to some, we believe that understanding how trading costs impact fund strategy is actually key to understanding the market structure of fund management, which is quite important for investors in funds to digest.

In our opinion, discipline with assets under management and trading costs can be one of the most determinative influences on long-term strategy performance. And unlike much of the financial literature consumed on nearly wholly unpredictable portfolio influences, this influence is relatively knowable today. As one of the world’s leading experts on market friction, Andrei Shleifer once remarked, “We understand a lot more about the limits of arbitrage than we do about investor sentiment.”

Trading costs are a barrier that limit every manager's ability to exploit arbitrage opportunities at scale. Yet there appears to be little consensus in the research community about how restrictive those costs are when managing large sums of money.

On one side of the spectrum, AQR’s Frazzini et al. (2014), after studying proprietary data from a large institutional investor covering 19 developed markets from 1998 to 2011, found that actual trading costs were less than one-tenth as large as previous research had suggested. They concluded that, on account of trading costs, “the main anomalies to standard asset pricing models are robust, implementable, and sizable.” They estimate approximately 10 to 20 basis points of realized trading costs for large and small caps, respectively, for a large institutional investor.

Dimensional Fund Advisor’s Robert Novy-Marx (2019) found similar, though slightly higher, estimates when analyzing effective bid-ask spreads from 1975 through 2016. For him, microcaps have generally traded at about 50bps of one-way costs, small caps around 30bps and large caps around 20bps since 2000.

That doesn’t sound like a lot (at least for lower-turnover strategies), and in both studies trading costs declined dramatically for small and microcap stocks after the introduction of decimalization and widespread adoption of electronic trading at the turn of the century. Both studies suggested that there are various methods practitioners use to effectively reduce trading costs below the theoretical levels implied by bid-ask spreads.

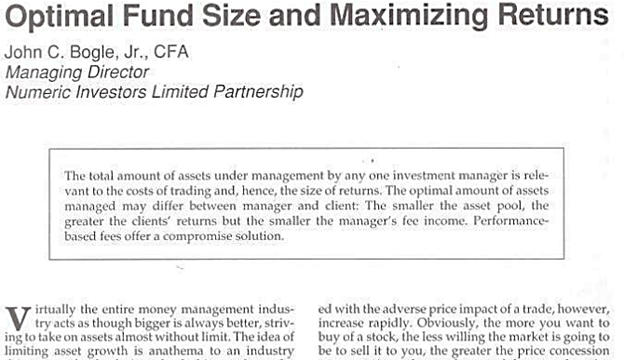

For a different perspective that emphasizes more problematic trading costs at large scale, one must troll through older studies of the Australian exchanges or find research from John C. Bogle Jr. (the Vanguard founder’s son) explaining why passive had outperformed active management back in the mid-1990s:

Figure 1: Bogle on Trading Costs and Optimal Fund Size in 1996

Source: Bogle 1996 via internet archive.

For us, Bogle Jr.’s research doesn’t seem that theoretically controversial. To the extent a manager incurs any trading costs at all in a fixed strategy, those costs will increase as AUM increases. As a manager gets larger, they need to trade bigger quantities of the same stock. This mechanically pushes prices in an adverse direction as order sizes get larger.

If the larger manager slows down their trading to reduce their market impact while targeting the same turnover, they risk chasing a runaway stock as the price continues to move away from them.

If instead the manager changes their strategy, concentrating on larger and more liquid stocks (or runs a less concentrated portfolio), they water down their exposure to favorable factors, like value, that are historically associated with premiums. This is because value has quite persistently been inversely correlated with stock liquidity and size.

As Bogle Jr. noted, it seems almost “unavoidable.”

Small value is particularly sensitive to this. And to illustrate the dilemma, below we calculate the estimated trading costs for a standard definition of small value that is relatively AUM-permissive: the capitalization-weighted Ken French 2x3 portfolio which includes the ~700 stocks in the US market that are simultaneously in the smallest half and cheapest third of all listed stocks. We model no more than 10% of the median daily trading volume of the stocks is traded by the manager in a single trading session. And at that trading pace, the realized market impact costs are assumed to be one quarter of those published by Novy-Marx in 2019 (50bps for microcaps and 30bps for small caps). The one-quarter figure assumes there is some favorable short-term reversal of the trader’s prior-session market impact when trading occurs over multiple days. In the analysis below, we assume 20% annual turnover and show the two-way trading costs (the buys and associated sells) of the turnover. We also show how many days it took to complete 80% of each rebalance turnover at that AUM level, but we do not include any “runaway” costs for the slower turnover speeds.

Figure 2: Forward-Looking, Cap-Weighted Small Value Trading Cost Estimates

Source: Compustat. Volume characteristics extracted for all listed US stocks above $25M in market cap, excluding REITs and financials. 20% annual turnover and adverse market impact of one-quarter of the bid-ask spread assumed.

This market impact estimate does not include any brokerage commissions for firms that outsource their trading (typically 10-20bps), and it does not include management fees or any administrative costs. But even with just these transaction cost assumptions, turning over $5B in a Ken French cap-weighted small value strategy of the ~700 cheapest and smallest stocks had transaction costs of about 1.73% per year for a 16% lower value of investment after a decade. And this is before penalizing the returns for the fact that it took 61.4 trading days to execute that turnover each year. Portfolios with over $20B in AUM (at 246 or more days to complete) didn’t even have enough trading days in the year to achieve a 20% rebalance without pushing the 10% of median daily volume limit in the model.

Another way to estimate this is to take the size and volume characteristics of this portfolio historically and backtest the costs in a similar way. We performed this test over the last 20 years and found similar results.

So how do these cost estimates compare to the gross premiums for the factor portfolio? Below are the gross returns for the Ken French Small Value Portfolio in order of least sensitive to trading costs to most. The leftmost blue bar below is the portfolio strategy for which trading costs were estimated in Figure 2 above.

Figure 3: Small Value Factor Returns by Trading Cost Sensitivity (1926–2022)

Source: Ken French Library. US portfolios sorted on P/B and market cap.

Gross of all costs, it made a lot of sense to tilt toward small value for the last 95 years. However, the strategies that were least sensitive to trading costs as AUM increased also had significantly less room for costs to beat the market. On the 2x3 small value portfolio, there was only a 2-3% gross premium above the market.

The good news is that strategies managed well within their capacity limits seem to have a significantly higher probability of outperforming the market net of costs without having to bet the whole boat on manager skill or beta clairvoyance. And a more disciplined manager is frequently well positioned to take the other side of any price impact introduced by less capacity-constrained and cost-concerned managers in similar strategies.

There is perhaps a level of redistribution of returns from the haves to the have-nots already embedded in our capital markets. This theory and the cost simulations would be in line with the empirical track record of hedge and mutual fund performance by AUM controlling for strategy style.