Got Diversification?

The S&P 500 isn't the only source of returns

Market cycles come and go, but human nature never changes.

The reason we invest is to make money. So it’s quite natural that we evaluate the quality of an investment by how well it’s done at making us money lately. The historical reasons for outperformance crystallize into a narrative that could justify perpetual dominance and, therefore, additional investment.

But no asset class can outperform forever. Inevitably, events occur that make the old narrative defunct. A new asset class begins to outperform, and a new narrative emerges.

We seem, at least from my vantage point, to be at a moment when the narrative is shifting. The “SPY or die” crowd got hooked on perpetually increasing valuations and an ever-strengthening dollar, trends supported by the continued extraordinary growth of large US technology companies.

But now the large US tech companies are moving from an asset-light, nearly infinitely scalable business model to an AI business model that is highly capital-intensive, with high marginal costs. Scared of Trump and tariffs, foreign investors are pulling their money from the United States, hurting both valuations and the dollar.

Larry Summers’ quip that Europe was a museum and Japan was a nursing home was conventional wisdom just a few months back. But between accelerating European defense and infrastructure spending and Japanese corporate governance reform, these two markets are finally generating strong returns on investment and attracting capital as a result.

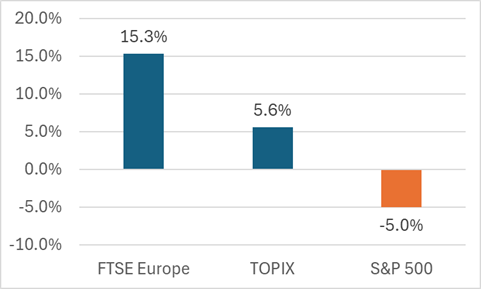

Last year, we wrote a series of articles about the need for international diversification and the likelihood of just such a shift. We even hosted a webinar in November, arguing that investors should strategically overweight Europe. And we have seen returns this year that are in line with our forecasts. The below table shows the returns of major European and Japanese benchmarks relative to the S&P 500 in 2025.

Figure 1: International Index Performance vs. the S&P 500 in 2025

Source: Verdad, Capital IQ

Diversifying equity allocations outside of the United States seems like a prudent move in this macroeconomic environment, and, given valuations, international outperformance is a trend that could continue for years to come.

But in a highly volatile environment where macroeconomic uncertainty and the risk of stagflation might challenge a reliance on equity beta alone, we also believe there are opportunities outside of equity markets.

Over the past few years, we have been investing in building out a technology infrastructure that can support fully systematic portfolio construction and risk management in all tradeable global securities across equities, corporate credit, global Treasurys, currencies, and commodities. After scoring these securities by their factor exposure, we predict returns, volatilities and correlations and build Sharpe-optimized portfolios. And while private markets and passive beta were the asset gathering winners of the past decade, we believe multi-asset, long-short, liquid strategies could be owed their day in the sun.