Family Wealth

Surprising findings on inheritance and intergenerational social mobility

A guest post by: Gregory Clark

“Shirtsleeves to shirtsleeves in three generations” is the folk wisdom about inherited wealth. The Vanderbilts are perhaps the prime example: one of the largest fortunes in America vaporized by excessive consumption.

Former Harvard economist Tuomo Vuolteenaho laid out the math for why this is so often the case. Maintaining family wealth over generations requires splitting the money among children in each generation (3.7% per year assuming three kids), long-term expected real GDP growth (2.5%), spending of at least 1%, and taxes and fees of an additional 2%, all of which adds up to 9.2% real growth. The best performing asset class, equities, has had a long-run real rate of return of only about 7% real, meaning even with a 100% allocation to equities, family wealth is going to shrink over time (with these assumptions, a 90% decline over 100 years). Shift into bonds, cash, or other lower-risk diversifiers and the money will evaporate even sooner.

I am a well-cited scholar on the persistence of social status over many generations, as in my book The Son Also Rises: Surnames and the History of Social Mobility. On wealth inheritance, I bring both good and bad news.

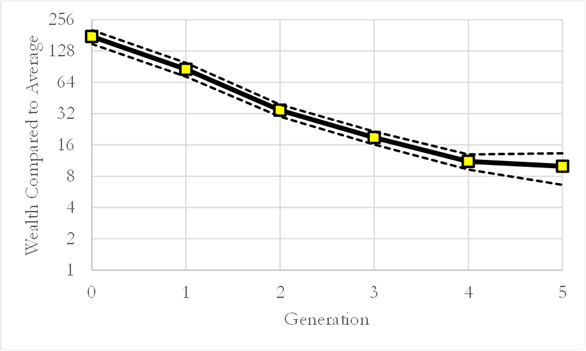

The good news, based on a lineage study of 447,000 English people from 1600–2026: for those with wealth, the “shirtsleeves to shirtsleeves in three generations” story is all wrong. Despite the obstacles laid out above, the descendants of the wealthy remain wealthy after five generations, and can expect to have above-average wealth for 10–12 generations (300–360 years), as the figure below illustrates.

Figure 1: Wealth at Death in English Family Lineages, 1600–2026

Note: Wealth at death, shown relative to the average, on a log scale. The dotted lines show the 95% confidence intervals. Source: Families of England database.

Astonishingly, the rise of public education and health, social security, and redistributive taxation have had no effect on the strength of wealth persistence. Wealth mobility now in England is no higher than in the eighteenth century. And because the data show that social mobility rates in the USA and England are very similar over the last 200 years, the English experience implies even in the USA.

The surprising news from the same study: the persistence of wealth within these families is unrelated to how much wealth children actually inherit. When it comes to inherited fortunes specifically, the “shirtsleeves to shirtsleeves in three generations” story is correct.

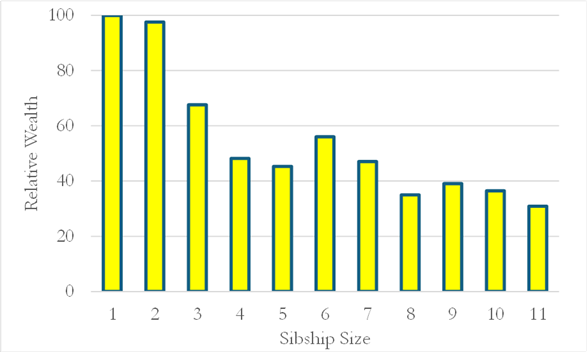

I prove that inherited wealth vanishes over three generations by looking at how variations in family size affect inheritance. Where families had wealth, larger families led to poorer children. A child in a family of 10 would get one-tenth of the bequest of a child in a family of one. Wealth inheritance in any generation for marriages before 1880 was thus subject to large random family size shocks. This is shown in Figure 2. More children implied lower child wealth compared to parents.

Figure 2: Child Wealth at Death Relative to Father as a Function of Family Size, Marriages before 1880

Notes: The horizontal axis shows the number of adult children for each father. The vertical axis shows average child wealth by sibship size, controlling for father wealth. It is normalized to 100 for families of size 1. Source: Families of England database.

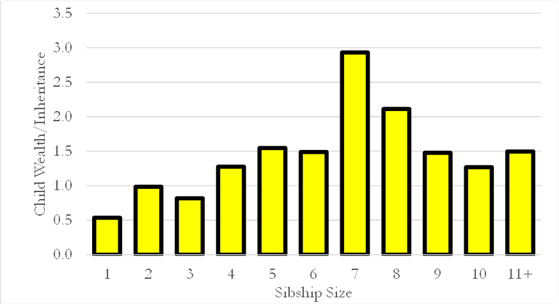

But interestingly, child wealth at death relative to the expected bequest to the child rose with family size, as we see in Figure 3. Children from sibships of 1–3 typically left less wealth than they inherited. But children of families of 7–12 left nearly twice as much wealth as they inherited. Immediately in these families, children adjusted their saving and accumulation behavior in response to bequest sizes. Those who got much, spent more. Those who get little, accumulated more. Wealth adjusted to the social status of the child’s family.

Figure 3: Child Wealth vs. Expected Inheritance, by Sibship Size

Notes: The bars indicate average child wealth relative to expected inheritance from the father by numbers of adult siblings. Source: Families of England database.

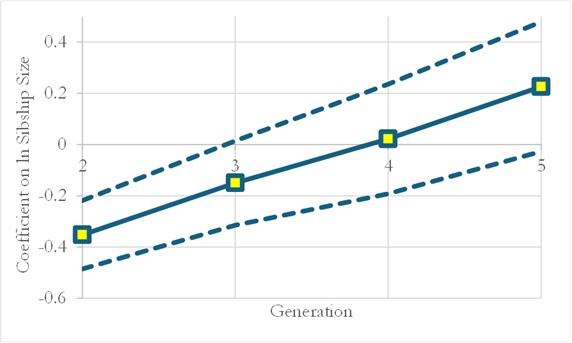

Figure 4 shows the estimated effects of being in a larger family on wealth for children (generation 2), grandchildren (generation 3), great-grandchildren (generation 4), and great-great-grandchildren (generation 5). By the time we observe the great-grandchildren, the estimated effect of wealth shocks from family size is 0. Descendants from families of 1 have the same wealth as those from families of 12.

Figure 4: Effects of Initial Sibship Size on Wealth across 2–5 Generations

Notes: The dotted lines show the 95% confidence intervals. A negative coefficient implies a negative impact of initial family size on later wealth. Source: Families of England database.

Shocks to wealth from variation in family sizes disappear by the generation of the great-grandchildren. Vuolteenaho’s clear math is confirmed in these long-term studies: unexpected inherited wealth does not tend to last more than three generations or roughly 100 years.

This study has fascinating implications for the wealthy in the modern day.

The inheritance you leave to your children upon death will almost certainly be consumed by the recipients and their progeny within 2–3 generations. Your children and their children will get the satisfaction of increased consumption. It is extremely unlikely that the wealth you pass on will reach your great-grandchildren or their descendants. Beating these odds would require some combination of a) unusually high returns, which generally would require a near 100% equity portfolio b) frugality in spending, and c) extremely low drag from fees and taxes. But of course, the biggest reason large fortunes don’t survive three generations is simply that the number of beneficiaries is growing exponentially: the wealth is being divided over and over again.

Gifts to charitable foundations do have the possibility of creating a perpetual endowment. This money does not get divided three ways every generation, has a lower tax burden, and thus has a lower bar for required real rate of return. The 92% of his fortune that John D. MacArthur gave to his foundation will live forever, while the 8% he passed on to his children will be gone within three generations. The Ford Foundation, established by bequests from Edsel Ford in 1943 and his father Henry in 1947, will similarly be around forever. Indeed, with a current endowment of $16 billion, the foundation’s assets dwarf those of William Clay Ford, Jr., Henry Ford’s great-grandson. But the boards governing such charitable foundations are dedicated to social causes, not to the long-term wealth of their founders’ inheritors.

But the most important implication is this: the main mechanism of wealth transmission across generations is not the actual physical transfer of wealth. If what mattered was just inheritance of wealth, then the demographically induced wealth shocks observed from English marriages before 1880 would persist even beyond five generations.

For families with wealth now, even where we can trace that wealth back through inheritance to the nineteenth century, there is no causal connection between their nineteenth century inheritance and current wealth. The wealth holdings of individuals thus stem largely from their social and economic abilities. It is this which links them strongly in Figure 1 across six generations to the wealth of their great-great-great-grandfathers, not the actual wealth that they inherited from those forebears.

This holds true even in extreme cases of political wealth redistribution. A recent paper in the American Economic Review finds that, after the American Civil War, many former slave-owning households rebuilt much of their lost wealth in just one generation, and within two generations most had recovered entirely. Another study finds that, in China, the descendants of the elite who managed to survive the Communist Revolution’s violent land expropriations have re-emerged as key elements of the new wealthy class of China.

Both studies suggest that the human capital you pass on to future generations is as valuable as the financial capital you leave them. Education, connections by marriage and kinship, skills in wealth acquisition: the wealthy families that persist across generations seem able to pass these abilities and values on to future generations to a much greater extent than they are able to pass on the wealth itself.

The deeper implication is that the balance sheet is not the locus of a family’s fortune. Assets will fragment, dilute, and disappear, as they always have. What compounds is the intellectual and moral capital embedded in each generation. Judgment, discipline, curiosity, and ambition: these are the true endowments. Families that endure understand, whether explicitly or not, that where their treasure is laid up is not in accounts or trusts, but in the character and capability of their children and grandchildren and great-grandchildren.

About the author: Gregory Clark is professor of economics at the University of California, Davis. He serves as editor of the European Review of Economic History, chair of the steering committee of the All-UC Group in Economic History, and research associate of the Center for Poverty Research at UC Davis. His research focuses on applied economics and economic history. He is particularly interested in long-run economic growth, the role of human capital and social mobility. He is the author of “The Son Also Rises: Surnames and the History of Social Mobility” and “A Farewell to Alms: A Brief Economic History of the World.”

Appendix:

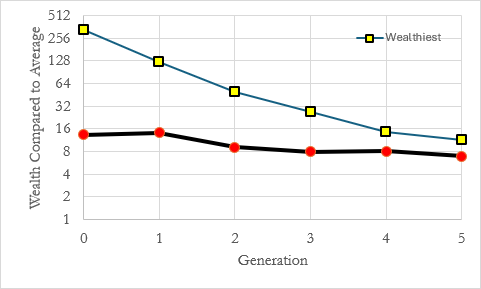

For the purpose of this essay, I also looked at the very wealthiest people: men in the original generation who left at least 50 times the average bequest. On average this group left 326 times as much as the average person. In the chart below, I compare how their wealth transfers over generations relative to the merely normally wealthy.

Figure 5: Wealth Compared to Average across Generations for the Wealthiest

Source: Families of England database.

Here we see that for the wealthiest families, wealth actually moves toward the mean fairly rapidly. At the end of six generations their descendants left bequests which were only 11 times the average. The normally wealthy group started with more modest wealth of only 13 times the average. Five generations later they still had bequests 7 times the average.

In generation 0 the wealthier group had wealth nearly 30 times as great as the modestly wealth group. But generations later they only had about 50% more wealth. In England at least, wealth erodes much more quickly for the super rich, but will persist for the moderately wealthy for even more than 12 generations.