Diverging Destinies in Corporate Japan

Stock market rewards companies responding to TSE’s request with tangible plans

By: Naoki Ito

Two years have passed since the Tokyo Stock Exchange (TSE) issued its directive urging listed companies to improve capital efficiency and raise their valuations, particularly for those trading below a 1.0 price-to-book (P/B) ratio. Since then, the number of companies responding to the request has steadily increased, with more than 70% of the targeted firms having now issued a response.

As the initiative progresses, a clear divergence has emerged between companies that responded proactively and those that offered only perfunctory disclosures. To better understand the effectiveness of these reforms, we conducted a comprehensive review of all companies listed on the TSE’s Prime or Standard markets that had a P/B ratio below 1.0 at the time of the TSE’s announcement.

We used natural language processing tools to automate the analysis of companies’ disclosures in their Corporate Governance Reports. In addition to the main text of the reports, we examined linked materials—such as relevant website pages and PDFs—and used OpenAI’s GPT-4 model to interpret the content. This allowed us to systematically categorize each company's response based on the specificity and substance of their disclosures.

Despite near-universal rhetoric around improving shareholder value, companies varied widely in their approach. Some laid out detailed, time-bound plans to increase dividends, repurchase shares, or reduce cross-shareholdings—measures explicitly linked to improving capital efficiency and share price. Others offered vague assurances of long-term profits growth and efficiency gains without committing to concrete steps.

For analytical consistency, we considered only those plans that specified a measurable target—such as raising the dividend payout ratio from 30% to 50% for the next year, repurchasing shares worth ¥10 billion in the next three years, or reducing cross-shareholdings to 10% of net assets within five years—as tangible. By contrast, we classified generic or open-ended statements—such as maintaining stable dividends, repurchasing shares “as necessary,” or making efforts to reduce cross-shareholdings—under vague commitments.

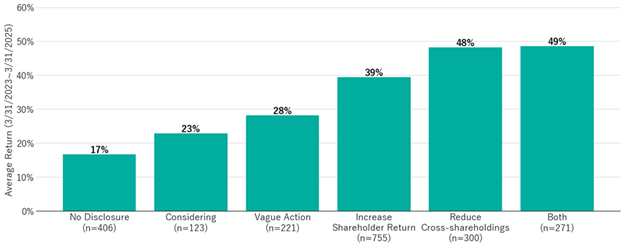

The chart below illustrates how differences in the actions taken by companies with a P/B ratio below 1.0 affected their stock performance over the two years following the TSE's request.

Figure 1: Stock Price Return by Reform Plan

Source: S&P Capital IQ, TSE, Company websites, Verdad analysis. “Increase Shareholder Return” includes companies with tangible plans in either dividends or buybacks.

The market has rewarded clarity. Companies that disclosed specific and actionable reforms saw their stock prices rise sharply—on average, more than double the gains of peers that offered no disclosure. Moreover, compared to the companies with vague actions, companies with concrete plans to increase shareholder returns or reduce cross-shareholdings led to higher returns.

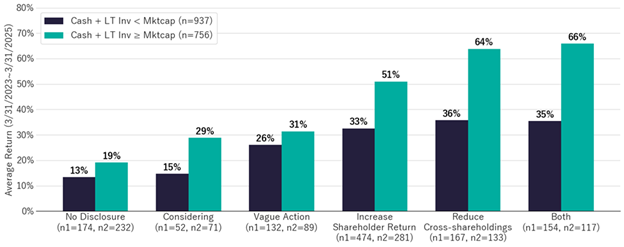

The contrast becomes even clearer for companies with bloated balance sheets. In our previous report about Nishikawa Rubber’s achievement, we highlighted how many Japanese firms hoard excessive cash and long-term investments like cross-shareholdings, and how a simple reallocation of such capital to shareholders can drive performance. The chart below shows a further categorization of Figure 1: whether a company has more in cash and long-term investments than its market capitalization. The share price performance of the companies with bloated balance sheets who announced reforms is even stronger than the averages.

Figure 2: Stock Price Return by Reform Plan and Balance Sheet Efficiency

Source: S&P Capital IQ, TSE, Company websites, Verdad analysis

Investors value companies that demonstrate transparency, decisiveness, and accountability. And companies with more cash and long-term assets on their balance sheets benefit more from pursuing reforms than those that are already lean. This raises a fundamental question—why have hundreds of companies, especially those with idle capital, still failed to take meaningful action?

In our conversations with company management teams, a common refrain emerges: boosting the stock price for its own sake is not a priority, and short-term price movements do not reflect long-term strategic value. Others emphasize the need to retain cash for future growth investments, arguing that returning excess capital to shareholders through special dividends or buybacks would constrain their financial flexibility.

From a risk-averse management perspective, hoarding cash or maintaining legacy cross-shareholdings may seem prudent. But increasingly, such practices are seen as economically inefficient—and even detrimental—from a broader societal viewpoint. At the macro level, stagnant capital trapped in underperforming companies stifles economic dynamism. It prevents capital from flowing to sectors with greater potential for growth and returns, effectively becoming a bottleneck in Japan’s ongoing struggle to break free from its deflationary mindset and reignite sustainable growth.

If a company lacks viable internal reinvestment opportunities that can generate returns above its cost of capital, then the responsible course of action is not to sit on excess cash but to return it to shareholders. Doing so allows capital to be reallocated—whether by institutional investors, pension funds, or individuals—to more productive use elsewhere in the economy. This is not merely a shareholder-centric argument: it is a governance imperative.

This capital recycling function does not rest solely with shareholders. Companies themselves have the agency—and arguably, the duty—to redeploy capital beyond their existing operations. Strategic M&A, for example, is a legitimate and often value-creative lever in Japan for companies with strong balance sheets to reallocate idle cash toward growth, innovation, or synergies in adjacent markets. But such moves require a shift in mindset: from preservation to performance, from caution to calculated risk-taking. As highlighted in our previous article, Hiroshi Nojima of Nojima Corporation exemplifies this approach with a boldness that deserves lasting recognition.

Japanese companies must begin to think more like investors. The principle is elementary—“buy low, sell high”—but its application within corporate Japan has often been lacking. If an external investor saw a business trading well below its intrinsic value, they would likely see an opportunity to buy. The same logic should apply internally. Share buybacks, when executed at depressed valuations, allow the company to invest in itself—concentrating ownership among remaining shareholders.

If companies dismiss dividends as a poor use of capital, then they should embrace buybacks—especially when their shares are discounted. Buybacks can enhance per-share metrics and provide a mechanism through which the company, not just the shareholder, participates in future upside. For companies that publicly proclaim confidence in their future growth prospects, failure to buy back their own discounted shares raises questions about alignment between rhetoric and capital allocation.

Japan’s corporate governance reforms, which began with Abenomics about a decade ago, have made notable strides. But the TSE’s recent directive signals a meaningful shift—from procedural compliance to outcomes-driven accountability—and the momentum is clearly taking hold. The durability of this corporate renaissance now hinges on whether more companies are willing to break from outdated norms and adopt a capital allocation mindset aligned with shareholder value.

Ultimately, the TSE’s initiative isn’t about valuation multiples for their own sake. It’s about prompting a reckoning in Japanese boardrooms—about what it truly means to be a public company, the responsibilities that come with access to investor capital, and the role listed firms play in the broader allocation of financial resources across the economy. The P/B ratio may be a blunt instrument, but it remains a telling one. And the market has made clear: it stands ready to reward those who rise to the challenge.