How to Capture Japan's Value Unlock

A simple approach of buying low price/book stocks compares favorably to activism and PE

By: Naoki Ito

Most investment opportunities depend on discounting future cash flows, estimating growth rates years into the future, and assessing the riskiness of the cash flow streams. Not in Japan.

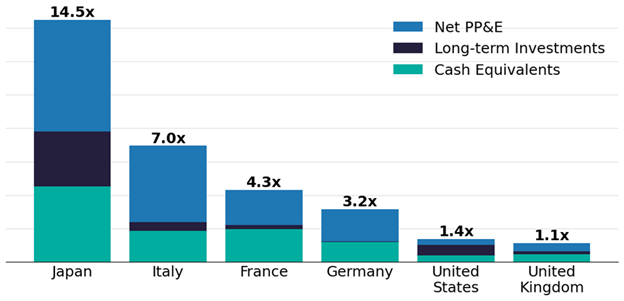

Today, there are about 1,000 public companies in Japan trading at <1x book value (and about 200 trading below 0.5x book). The median company trading below 1x book has 15 years of net income crystallized on its balance sheet, primarily in a mix of cash, cross-shareholdings of other public equities, and real estate.

Figure 1: Global Balance Sheet Comparison of Companies with P/B <1x (September 30, 2025)

Sources: S&P Capital IQ, Verdad analysis. Notes: For each bar, medians of cash/net income, long-term investments/net income, and net PP&E/net income are calculated separately and then combined. Only companies with market cap above $50M are included in the dataset.

The Tokyo Stock Exchange (TSE), together with the Ministry of Economy, Trade and Industry (METI) and the Financial Services Agency (FSA), is forming a unified and powerful front to drive corporate governance reforms among public companies. The central driver of the initiative is the TSE’s directive issued 2.5 years ago, which raised concern that more than half of listed companies were trading below 1x P/B and required all companies to enhance capital efficiency to address the situation. This has led many firms to sell cross-shareholdings, deploy idle cash, and increase shareholder payouts — effectively beginning the process of returning that 15 years’ worth of net income to shareholders.

We believe the best way to bet on the success of these reforms is simple: buy a portfolio of stocks trading at the lowest possible P/B multiple, prioritizing the quality of the assets on the balance sheet and the robustness of earnings and free cash flow generation, and then wait for the repricing. The playbook is crystal clear: as regulators drive companies toward 1x P/B, investors should own those trading at the deepest discounts to book value.

However, that’s not the way most investors, particularly large institutional investors, are approaching Japan. Activism, private equity, and passive beta exposure as a placeholder seem anecdotally to be the most widespread approaches. Here we explore the structural limitations of all three strategies.

Shareholder Activism’s Illiquidity Isn’t Worth the Risk

The most in-vogue approach among the Yale cubs is concentrated activism, where a fund will take large stakes in 20-30 companies and push the companies to make changes to capital allocation and operations. The logic is intuitive: if the issue is corporate governance, then the solution must be investors focused on governance.

But we believe there are potential drawbacks to using activism to bet on Japan’s corporate governance reforms for three reasons:

Activism is not necessary to see a revaluation story. It accounts for only a small part of Japan’s re-rating. Since the reforms were announced, activists have been involved in only 25% of the companies that have improved their valuation from below 1x P/B to above 1x P/B. The majority of reformers were responding to the TSE’s reform pressures without needing activist investors to push them.

Activism is not sufficient to see a revaluation story. The failure rate of activist campaigns is high. Of the 51 companies that received shareholder proposals from activist funds at this year’s June AGMs, only four saw motions approved—an 8% success rate. Among these, three were outright proxy battles where activists controlled as much as 25–40% of outstanding shares.

Meaningful influence requires large ownership stakes. That means taking large, illiquid positions. Our research has found that activists typically own about 37x daily volume in the names in which we see them being active. It’s very hard to exit such large positions, particularly if the investment case sours. And in a concentrated portfolio, having money that’s trapped in a large position that isn’t working means substantial idiosyncratic risk.

Given the intense pressure for reform coming from the TSE and the FSA, we’re not sure activism is as essential to catalyzing value in Japanese equity investing as it might have been in previous years. A simpler, more efficient strategy might be simply to own companies trading significantly below 1x P/B, which have, unsurprisingly, been where activists have found the most attractive and successful investments.

Private Equity Can’t Capture Value Through MBOs

Private equity has been growing rapidly in Japan. In a recent interview, EQT CEO Per Franzen said “Strengthening our presence in Japan sits at the top of EQT's firm-wide priorities.” KKR and others have echoed these sentiments.

PE’s primary way of capitalizing on the public market transformation has been through take-private transactions, often executed as management buyouts (MBOs). But these deals happen at valuations far above the core “value unlock” segment of Japan’s public market.

Since 2020, we have identified 42 take-private transactions involving PE buyers of liquid public companies. Of these, only one had a tender offer with an implied P/B below 1x. The median transaction occurred at 3.0x P/B, and buyers paid a median 40% premium to the share price one month before the tender offer announcement.

Those prices seem likely to only go higher as competition and regulatory scrutiny increase. From July 2025, the TSE has required any buyout involving insiders such as management or parent companies to disclose an independent third-party valuation and justify the tender offer price. This reform aims to prevent unfairly low takeovers that disadvantage minority shareholders. Even when lowball MBO offers are attempted (especially those below book value), other funds often intervene, driving competitive bidding and pushing prices toward fair value. Recent examples include Fujisoft, Taiheiyo Kogyo, Soft99, and Mandom, each of which attracted counteroffers reflecting the company’s intrinsic worth.

Moreover, the cultural and structural barriers to unsolicited takeovers in Japan remain high. Management teams, particularly those presiding over undervalued but profitable firms, often value the prestige of public listing over private ownership. They would rather maintain a 5% dividend yield than leverage their balance sheet at a 1% borrowing cost to take the company private. For such public companies, the TSE’s valuation reform initiative is proving to be the most effective catalyst for self-driven value creation.

Passive Beta Exposure Is Too Broad to Capture Value Unlock

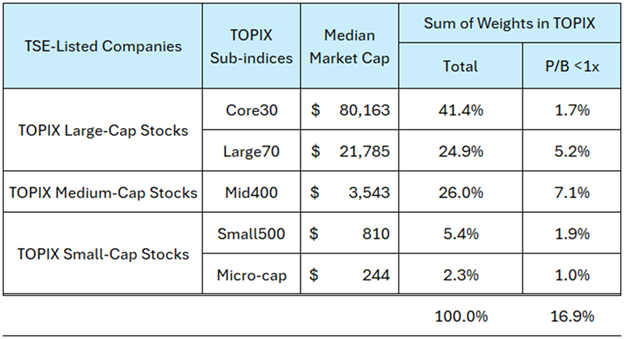

For those less seduced by the siren call of exotic complexity, simply buying a Japan ETF seems like a reasonable placeholder. But these ETFs actually offer little exposure to the corporate governance reform trade. Broad market ETFs, for instance, are dominated by large-cap exposure. In the TOPIX, roughly two-thirds of the index weight sits in the largest 100 companies, where much of the simple valuation re-rating from balance sheet reform has already occurred. Only 17% of the total weight consists of companies with P/B below 1x, as Figure 2 shows.

Figure 2: TOPIX Constituents and Weights (September 30, 2025)

Sources: TSE, S&P Capital IQ, Verdad analysis

The core opportunity—small, under-researched, cash-rich companies undergoing reform—barely registers in passive allocations. Even factor-based ETFs, such as “value” or “small-cap” indices, are rebalanced infrequently and cannot shift capital from companies that have already re-rated to those yet to unlock.

An Alternative Approach to Capturing Value in Japan

Activism, private equity, and passive indexing each capture fragments of Japan’s value-unlock story, but all face structural limits. PE pays too much for control. Activists fight hard for influence but face low success rates and liquidity traps. Passive funds offer breadth but no precision.

If you expect activism and private equity to grow in Japan, we believe the optimal positioning is not to co-invest with them but to front-run their target investments. Instead of pursuing the uncertain success of activism or paying hefty PE premiums, we believe the optimal investment approach for long-term success in Japan is to buy a diversified basket of small, undervalued, high-quality companies with strong cash generation and balance sheets rich in unproductive assets. A diversified portfolio of Japanese companies trading at deep discounts to book value can allow investors can participate in Japan’s reform-driven re-rating and dynamically adjust exposure as the opportunity set evolves.