The Real Estate Drag on Corporate Japan

Real estate is held as a corporate buffer, but functions as a capital burden

By: Naoki Ito

Large rental real estate holdings that earn returns well below the cost of capital are a striking feature of Japanese corporate balance sheets. It’s an inefficiency that creates a long-term drag on performance.

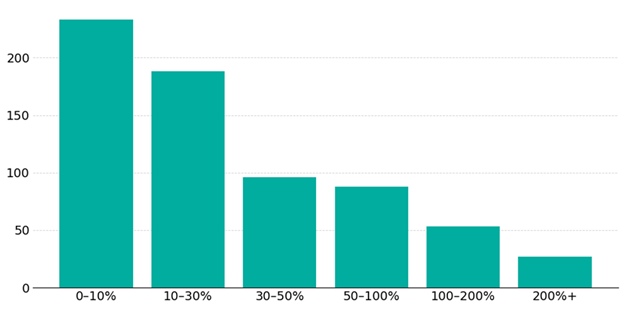

About a quarter of listed companies on the Tokyo Stock Exchange (TSE) hold “real estate for leasing or similar purposes” on their balance sheets. Collectively, they hold rental real estate with a fair value equivalent to 23% of their aggregate market cap.

Figure 1 shows how the fair value of rental real estate compares to market capitalization across the ~800 companies in our study.

Figure 1: Distribution of Rental Real Estate Fair Value as % of Market Cap (June 2025)

Source: S&P Capital IQ, companies’ annual security reports. Note: Includes only companies outside the GICS Real Estate and Financials sectors that report “real estate for leasing or similar purposes” in notes on their financial statements.

To make this more tangible, consider two examples.

Kaken Pharmaceutical (4521.T) owns Bunkyo Green Court, a nearly 10-acre mixed-use complex in central Tokyo, developed on legacy land acquired in 1948. This property houses office, residential, and commercial spaces, generating rental income unrelated to Kaken's core pharmaceutical business. The total estimated fair value of this leased real estate equals approximately 40% of Kaken’s market cap.

Kyodo Printing (7914.T) owns legacy real estate in central Tokyo, originally acquired nearly a century ago. Recently, the company redeveloped part of this land into a gleaming new headquarters building that cost nearly $100M. They have leased another 3 acres to a developer who is building a 500-unit residential complex. Altogether, the fair value of Kyodo Printing’s leased properties represents roughly 40% of its market cap.

Japanese management teams hold onto these real estate assets not because they provide strategic value to core operations but because they generate stable, passive income—a feature much appreciated by risk-averse executives, especially during downturns.

But investors don’t see things the same way: public equity investors want capital-efficient companies that focus on their core businesses. Rental real estate, though boasting strong margins, can tie up large amounts of capital without generating proportionate growth, especially when compared to core businesses that, even with slimmer margins, put capital to more productive use.

Investors allocate capital to manufacturers, service providers, or tech companies for their unique expertise and ability to generate above-hurdle returns, not for passive income from real estate. If investors want real estate income, they can purchase property directly or invest in REITs. REITs offer yields that meet or exceed sector hurdle rates, with better diversification and risk control—benefits that a non-real estate company with a few non-essential properties cannot provide.

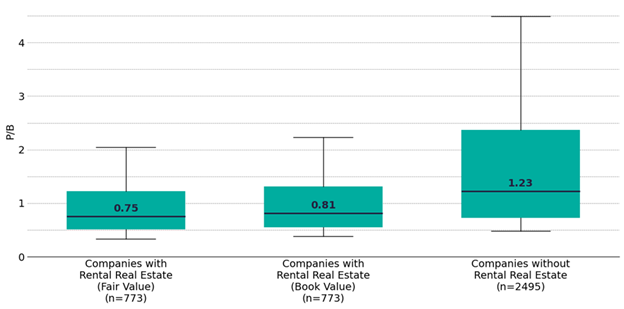

Leasing properties may seem to provide a margin of safety, but they carry an implicit cost: diluting return on capital and eroding valuations. To quantify this cost, we analyzed notes included in the financial statements of these companies, which disclose both book value (historical cost net of depreciation and write-downs) and fair value of these properties under Japanese GAAP.

Among the ~800 companies with rental real estate, 62% trade below book. This is 20% higher than the 42% of companies across all TSE-listed companies that trade below book. When we adjust book values to reflect the disclosed fair values of rental properties, capturing their price appreciation over time, the share of companies trading below book rises further to 66%.

Figure 2 illustrates the divergence in price-to-book (P/B) valuation distributions between companies with and without rental real estate holdings. For companies holding rental real estate, P/B ratios are calculated based on both the reported book values and adjusted fair values of these properties.

Figure 2: P/B Distribution: With vs. Without Rental Real Estate (June 2025)

Source: S&P Capital IQ, companies’ annual security reports. Note: Includes only companies outside the GICS Real Estate and Financials sectors. The P/B of “Companies with Rental Real Estate (Fair Value)” is calculated based on the fair value of rental properties, instead of their accounting book value. Whiskers represent 10th and 90th percentiles.

This is not coincidental. We believe non-core real estate holdings represent a significant drag on corporate valuations. To illustrate this, we calculate leasing operating profits from disclosed rental revenues and associated expenses. Dividing this figure by the fair value of the properties provides an estimate of the return on rental real estate. As leasing costs under Japanese GAAP include depreciation, these returns are slightly lower than the cash-based net operating income typically used in traditional cap-rate analyses.

We view the operating return on rental real estate and the company-wide EBIT/EV as comparable metrics, as both represent pre-tax returns relative to asset fair values—one measured at the property level, the other at the enterprise level—each inclusive of depreciation and independent of capital structure.

The median operating return on rental real estate is just 3.6%, while the median company-wide EBIT/EV is 9.1%. EBIT/EV exceeds the rental real estate operating return in 80% of cases, with the median company generating returns 2.4x higher from its core operations than from property leasing.

This disparity highlights the opportunity cost of capital tied up in these assets. If rental real estate generates only a 3–4% return, whereas core operations deliver more than twice this rate, the performance drag is evident. Low valuations, therefore, are not a mystery; they reflect investors' rational response to capital inefficiency.

The solution is clear: divest unnecessary real estate and redeploy capital into opportunities that deliver higher returns for shareholders. Whether reinvesting in core businesses with higher operating yield than property leasing, repurchasing shares, reducing debt, or distributing cash to shareholders, any alternative is more productive than leaving capital tied up in low-yielding properties.

Companies can easily sell these real estate assets, as demand from global investment funds eager to acquire properties held by Japanese firms continues to grow. Bloomberg reported that Bain Capital has acquired more than $5 billion in Japanese real estate and is currently negotiating multiple additional transactions, explicitly targeting undervalued, non-core corporate properties. Similarly, BentallGreenOak (BGO) plans to deploy approximately $11 billion in equity investments into Japanese real estate over the next two and a half years, focusing specifically on corporate-owned properties pressured onto the market by shareholder activism and governance reforms. These well-funded buyers indicate a clear opportunity and viability for divesting non-core real estate assets for corporate Japan.

Crucially, rental real estate represents just one category of non-core assets. The same rationale extends to idle factories, peripheral commercial spaces, and oversized or unnecessarily expensive headquarters.

Some companies are taking action, and investors are responding positively to their shift toward core operations and improved capital efficiency. Consider two examples:

SAXA (6675.T) announced the sale of a retired factory that had been leased out. The sale proceeds exceed the company’s pre-announcement market cap, and SAXA plans to use them for growth investments like strategic M&A while returning some as special dividends over five years. This year’s dividend per share guidance is nearly 80% higher than last year’s, and the price has surged by more than 30% since the announcement.

Sapporo Holdings (2501.T) is in the process of selling a landmark shopping mall in central Tokyo, with bidders including Bain Capital and KKR. The sale is projected to fetch over $2.8 billion, potentially making it the largest real estate deal in Japan this year. Sapporo plans to reinvest the proceeds into its alcoholic beverage business and has explicitly stated its intention to exit the capital-intensive real estate sector.

While some companies are setting the standard, hundreds still hesitate. The TSE’s corporate governance reform agenda has ignited attention on capital inefficiency, and investors are increasingly vocal. Ongoing investor engagements pushing for real estate divestments include Strategic Capital at Wakita (8125.T) and Dalton Investments at Fuji Media Holdings (4676.T).

True value creation comes from innovation, operational excellence, and disciplined management—not from hoarding underperforming real estate. Treating properties merely as financial buffers undermines capital efficiency and valuation. Divesting these assets is an essential step toward unlocking shareholder value and rebuilding investor trust.