The Efficacy & Cost of Hedging with Options

The Price of a Good Night's Sleep

By: Verdad Research & Thatcher Gearhart, Ames Lyman, Neelay Trivedi

Few people can say they were prepared for COVID or its impacts on society. But a small group of people looked prepared indeed for the sudden shock that hit markets in March of 2020. These were investors who had bought tail risk protection and saw their portfolios soar by nearly 60% at a time when most other investors saw theirs slashed by 30%.

These spectacular returns, and the associated media attention, prompted us to revisit our earlier work on tail risk hedging. Over the last few months, we talked to industry experts, read all the available materials on options hedging, and crunched 25+ years of daily options data. As market volatility picks up this week, now is perhaps a good time to take a look at what we learned about options-based hedging.

And while we would like to say we discovered a great novel strategy to achieve amazing returns and protect your portfolio, unfortunately we discovered only that options-based hedging strategies—at least the simple, passive ones—are pricy and unreliable and would historically have detracted from investor portfolios. That is not to say that good tail risk strategies don't exist, or that there aren’t practitioners with real skill. In fact, in our research, we came across one or two firms with stellar records. Rather, we would say that the most basic implementations of options-based hedging are not good tools.

Backtesting options hedging strategies is not an easy feat. Most of the literature we read on the topic relied on backtesting synthetic data series, allowing authors to create and attribute a price to synthetic options for any moneyness and duration parameters. While some methodologies used in the existing literature seemed robust, we wanted to rely on realized historic options prices to make sure we captured nuances, such as liquidity or bid-ask spreads, as they would have been reflected in an investor’s actual portfolio. To do that, we used OptionMetrics for daily data on all S&P 500 over-the-counter options since 1996. OptionMetrics is the premier provider of historical options data for use in empirical research and econometric studies. We focused on S&P 500 options because they dominate options trading volume and have a long historical series.

The Efficacy of Options-Based Hedging

We first began evaluating the efficacy of options-based hedging by using a common strategy from academic and practitioner literature: monthly roll of 3-month, 30% out-of-the-money (OTM) put options on the S&P 500. This option has a strike price that is 30% below the current trading price of the S&P 500, which means that, at the end of three months, it will be worthless unless the actual S&P 500 has fallen by 30% or more of its current value. However, until it expires, the options are still worth something, given that there is always some probability that the S&P 500 will fall by 30%. This is why these options are “rolled,” meaning that investors sell the options one month after purchase and buy new three-month, 30% OTM put options. They are thus able to recover some of the premium initially paid while maintaining continuous exposure to the S&P 500. We assume a 60bps monthly allocation because, on average, it would have covered 100% of a buy-and-hold equity portfolio. In doing so, we follow the lead of Corey Hoffstein and his own evaluations of options-based hedging.

Below we show an index of running this options strategy as a standalone (i.e., not part of a portfolio).

Figure 1: Standalone Options Hedging Strategy Index (1996–2020)

Instrument: 3-Month 30% OTM Put Options

Source: OptionMetrics, Verdad. Assumes 60bps monthly allocation to options.

Like insurance, such a strategy would constantly incur small losses but prove itself useful during major downturns. In practice, however, a hedging strategy would never be implemented on a standalone basis but rather as part of a broader portfolio. For the purposes of this research, we assumed hedging is applied to an all-equity portfolio (i.e., S&P 500 buy-and-hold).

Below we compare the performance of the S&P 500 during the COVID-19 crisis hedged with 30% out of the money put options. We show a variety of different approaches to rebalancing or rolling the options: rebalancing at the end of each month, rebalancing daily, rebalancing weekly, and rebalancing mid-month. We do this to illustrate the sensitivity of the hedge’s performance to seemingly minor changes in timing.

Figure 2: S&P 500 Peak-to-Trough Returns in COVID-19 by Hedging and Rebalancing Strategy (Jan 2020 – Mar 2020)

Instrument: 3-Month 30% OTM Put Options

Source: OptionMetrics, Capital IQ, Verdad.

As shown above, options hedging is dependent on timing, as a number of other academics and practitioners have concluded. To eliminate this “luck-in-timing” problem, we assume a daily implementation of the strategy for the rest of the piece, despite the administrative and operational challenges associated with executing such an approach.

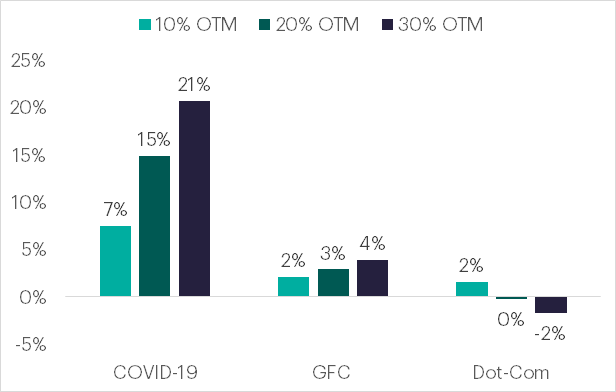

Let’s look at how the same strategy would have fared during other large drawdown events: the dot-com bubble (a 47% decline) and the Great Financial Crisis in ’08 (a 52% decline). Below we show the excess returns (or foregone drawdowns) from hedging. We also added two other “moneyness” thresholds to the analysis: 20% OTM and 10% OTM. We kept the same approach: monthly roll of three-month out options rebalanced daily.

Figure 3: Peak-to-Trough Excess Returns over Unhedged Strategy by Crisis

Source: OptionMetrics, Capital IQ, Verdad.

Options hedging seems to have been effective during COVID-19. However, when tested in other crises, the strategy did not seem to provide nearly the same level of protection. So what was different in the 2020 drawdown?

The answer seems to be “speed.” When overlapped with the speed of the drawdown (see below), these results reveal an interesting pattern: the efficacy of the hedge seems inversely proportional to the speed of the drawdown. In addition, deeper OTM options were more efficient in sudden crises (COVID) compared to crises that unfolded more slowly (dot-com). This makes intuitive sense: the faster the drawdown happens, the higher the option convexity, given higher implied volatility and speed with which the S&P 500 approaches the strike prices. And the curve is most convex for deeper OTM options.

Figure 4: Days from Peak to Trough by Crisis

Source: OptionMetrics, Capital IQ, Verdad

This supports the argument that options-based hedging seems to be most useful in black swan events, but only two such sharp and sudden drawdowns have happened in the past 50 years: Black Monday in 1987 and COVID-19 in 2020. We do not know if tail risk hedging would have worked in 1987 because of lacking data, but even if our hypothesis holds true, investors that hedged after Black Monday would have had to wait 33 years for their hedges to work again.

Option Hedging Costs

If the next black swan event is to happen in the 2050s, the annual cost of insurance becomes critical. Below we show returns for hedged and unhedged S&P 500 buy-and-hold strategies. The number in the oval represents the implied annual cost of the strategy (i.e., the return differential between the hedged and unhedged buy-and-hold strategy).

Figure 5: S&P 500 Returns by Hedging Strategy (1996–2020)

Instrument: 3-Month Out 30% OTM Put Options

Source: OptionMetrics, Capital IQ, Verdad.

Investors would have incurred an annual average cost of 260bps to avoid the volatility in March 2020! Options-based hedging strategies seem to have been an effective instrument to hedge in black swan events such as COVID-19. And with the pandemic still vivid in investors’ minds, paying 260bps annually to avoid two-thirds of the drawdowns seems acceptable at first glance, so putting this in context might be helpful. The 21% excess returns during the March 2020 drawdowns translate into approximately 80bps compounded annually since 1996. In other words, an investor would have had to pay a 3x lower annual cost over the past quarter of a century to break even in March 2020.

We should, of course, caveat this analysis by noting that we are testing the most simple, passive approach to options-based hedging, that investors might reasonably expect higher volatility and therefore more benefits in the future, and that this simple analysis is the most negative potential view of options-based hedging given that we were only really testing out-of-the-money puts as a stand-alone strategy. Despite significant research, we were unable to identify a simple options-based approach that both protected against black swan events and did so at an acceptably low cost - achieving this goal requires either a complexity of strategy or a robust active approach that goes beyond our basic quantitative efforts.

Acknowledgments: Our friend Thatcher Gearhart, a former colleague at Bain Capital, directed this research project. Ames Lyman and Neelay Trivedi interned with us this summer and worked with Thatcher and Igor on this project. Ames Lyman is in his final year of a dual MBA-MPA degree program at MIT Sloan and the Harvard Kennedy School. After graduation he will work in management consulting and is interested longer term in public and private investing. Neelay Trivedi is a junior at Stanford studying philosophy and economics with a minor in Chinese. He is interested in pursuing opportunities in private investing, particularly in emerging markets and Asia.