The Economic Recovery in Japan

What happens now that value has started growing like growth?

By: Verdad Research

Market crises are special opportunities for value investors. Sudden economic shocks are particularly painful for cyclical value stocks, as falling revenue and margin compression brutalize profits and investors flee. But as the economic recovery begins, these same cyclical value stocks tend to lead the market in profit growth and share price returns. As we wrote about back in October, these are some of the few times in market history when the cheapest stocks have grown their earnings faster than the most expensive stocks in the market.

The Japanese economy, with nearly 50% of public companies in the cyclical industrials and consumer discretionary sectors, experiences these economic cycles no less than the United States, which has only 20% of public companies in these sectors. Over the last few years, Japan has experienced trade wars and then the COVID lockdowns back to back, driving a 53% decline in corporate earnings from Q2 2018 to Q2 2020, as shown in the figure below.

Figure 1: Aggregate Japanese Quarterly Profits

Source: Japan’s Ministry of Finance

As in past recessions in Japan and elsewhere, the recessionary punishment was concentrated in the cheapest stocks that experienced the deepest margin compression. The LTM revenue, operating profit, and net income of the cheapest half of the Japanese market (right figure below) is down 10%, 52%, and 82% respectively on the latest earnings, while the financials of the most expensive half of the market have barely taken a hit (left figure below).

Figure 2: LTM Financials of Growth and Value Stocks vs. 2018 Peak

Source: Verdad, Compustat. Aggregate financials on all listed Japanese stocks above $25M in market cap, excluding REITS and financials. Growth stocks are those above the 50th prercentile breakpoint on P/B, and value stocks are those below.

The cheaper the stocks, the worse the margin compression in LTM financials and the greater the short-term rebound we began to see in Q4. In these recent earnings, value began to grow a lot more than growth did last quarter. After losing the greatest amount of earnings over the last year, the cheapest 20% of stocks started to dramatically outpace the growth rate of growth stocks in the last quarter as margins began mean reverting.

Figure 3: Net Income Growth of Japanese Stocks, LTM vs. 2018 Peak, 2020 Q4 vs. Q3

Source: Verdad, Compustat. P/B quintiles.

Despite one quarter of value outpacing growth, LTM EBIT margins are still 52% below their 2018 peak. Because of this, upward pressure on stock prices should depend very little on multiple expansion. Simply getting back to 2018 operating income is a ~100% return if these value stocks can hold their current multiples.

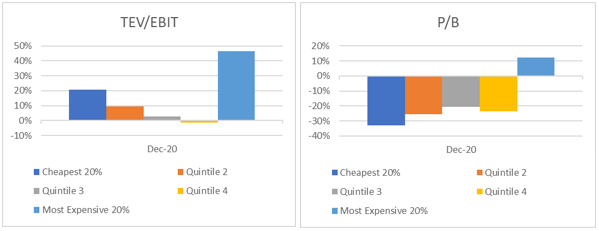

However, the market typically anticipates these recoveries for value stocks, and some multiple expansion on trough earnings is quite normal. But though small value has staged a dramatic recovery in Europe and North America, the market has not yet bid up Japanese small value stocks. Compared to before the recession, on these 50% trough margins, the cheapest stocks in Japan are only about 20% more expensive as a multiple of their LTM EBIT and are 33% less expensive on book value.

Figure 4: Multiple Expansion/Contraction of All Japanese Stocks, Trough vs. 2018 Peak

Source: Verdad, Compustat. P/B quintiles for both.

Valuation multiples have not risen nearly as much for value stocks in Japan as they have in other developed countries, and margins are still at roughly half of their 2018 precrisis levels. The “rotation to value” that is far along in North America and Europe has yet to happen in the same dramatic fashion in Japan.

But it will not take much in terms of fund flows to trigger a relatively large revaluation in Japanese stocks. The cheapest stocks in Japan are extraordinarily small: the aggregate market cap of the entire cheapest quartile of Japanese stocks is just under $250B, or about one third of Tesla’s valuation.