The Crisis in Turkey

Evaluating Countercyclical Investment Opportunities in Turkey

By: Greg Obenshain & Dan Rasmussen

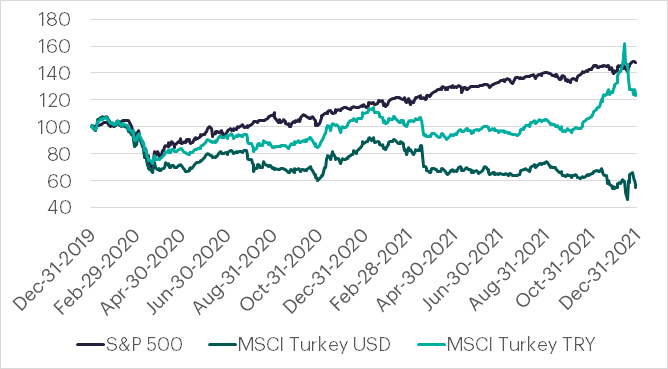

Only a few weeks ago, the economic crisis in Turkey dominated headlines. Even as the US market soared to new highs, Turkey's stock market experienced a brutal >50% sell-off. But the market barely noticed this week as Turkey posted a 54% year over year rise in consumer prices in February. Below we show the performance of the S&P 500 and MSCI Turkey indexes in both local and dollar-denominated currencies since the beginning of 2020.

Figure 1: MSCI Turkey and S&P 500 Index Performance (1/2020-12/2021)

Source: Capital IQ

Turkey is experiencing a crisis that follows what Paul Krugman described as a familiar script for emerging economies: foreign capital pours into a hot emerging market, the debt is denominated in dollars, a small shock hits that causes a “sudden stop” in foreign lending, the loss of confidence causes a drop in the currency, this makes it harder to repay USD-denominated debt, and this hurts the real economy, which further hits confidence in the currency, and so on.

Leaders in this situation face a terrible choice. Either raise interest rates to nosebleed levels to prevent capital flight and depress the economy or allow the currency to depreciate, create runaway inflation, and hope that the eventual export boom saves the economy from climbing debt-to-GDP ratios.

Recep Tayyip Erdoğan, Turkey’s leader, has taken the latter path. He has replaced central bank leaders with political allies, repressed critics, and vowed to battle “the scourge” of high interest rates by lowering them in the face of high inflation.

Figure 2: Turkish Lira vs. US Dollar Exchange Rate (2/2021-1/2022)

Source: Capital IQ, Verdad

How does this end? Typically, some combination of policy actions, restructuring, export increases due to currency depreciation, and IMF help feature in the denouement. In December, Turkey implemented some unique policy reforms that guaranteed domestic savers an interest rate that would at least match the losses incurred through the exchange rate. This directly attacks the problem of capital flight and in the short term seems to have arrested the slide in the Turkish lira.

We don’t know if this is the bottom or if the Turkish crisis will spiral further, but we do believe there is an opportunity for adventurous investors willing to take countercyclical risk to invest strategically in Turkey. In our “Emerging Market Crisis Investing” paper, we analyzed 87 crises across 18 emerging markets. We found that crises are some of the best moments to enter those markets since, after a period of volatility and potential continued drawdowns, investors can ride the recovery just as they would in developed markets. We differentiated between two types of crises: global ones, defined as a 50% drawdown in emerging markets that happen in parallel with a 20% drawdown of the S&P 500, and idiosyncratic ones, where only the local market has drawn down. Our research suggests that value stocks are strong return generators in global crises, but US dollar-denominated government bonds are a more reliable bet in idiosyncratic crises.

Figure 3: 2Y Average Return by Financial Instrument and Type of Crisis (1987-2020)

Source: Verdad. NOTE: Average across 87 crises in 18 emerging markets.

Turkey has experienced so many crises that we can also look at the country’s history as an even more specific source of base rates. Since 1997, when country-level data on government bonds and value stocks becomes available, Turkey has gone through six market crises: three idiosyncratic and three global. Below we show the performance of the dollar-denominated MSCI Turkey Value index, Turkish sovereign bonds, and the S&P 500 during these crises. In our research, we have found that a three-month lag before investing and a 24-month hold period tend to work well. The returns below follow this approach.

Figure 4: 24M Returns by Crisis in USD (1997-2020)

Source: Bloomberg, MSCI, GFD, Verdad

The results largely reflect what we saw in our broader sample: buying stocks works roughly 2/3 of the time, but the upside/downside is only worth it during global crises. USD-denominated Turkish sovereign bonds are consistent performers, never losing money and sometimes offering double-digit returns. These results are all the more impressive considering that Turkish equities earned a compounded annual return of 2.2% over the period from 1997 to 2020.

To evaluate the attractiveness of Turkish sovereign bonds in this crisis, we looked at the spread between the 10-year USD Turkish sovereign yield and the ten-year Treasury yield over time.

Figure 5: 10Y USD Turkish Sovereign Spread vs. 10Y US Treasurys

Source: Bloomberg

The current spread is 6.3%, below the March 2020 and October 2008 peaks of 7.7% and 7.8%, and well below the >9% spread in the early 2000s. But the median level of spread is just 3.0%. Every 1% change in spread leads roughly to a 7% price return on the bond. This is in addition to the 6.9% yield on the USD Turkish sovereigns.

This means that today, whereas 10-year US Treasurys yield 1.8%, Turkish sovereigns yield 8.1%. If spreads normalize to long-term medians over two years, this would imply a 16% annual total return (35% cumulative). We think this is a highly attractive opportunity in a world of near-zero interest rates. To put an 8.1% yield in perspective, the US high-yield market trades at 5.7% and 10-year USD-denominated Brazil sovereigns trade at 4.9%. Other countries with sovereigns that trade at a similar level include South Africa, Pakistan, and Nigeria.

Crises by their nature are hard to predict, but historical experience would suggest that USD-denominated Turkish bonds are at or approaching levels where investors should be paying attention.