Resurgent International Value

The international value premium returns after more than a decade in exile.

In teaching the virtue of fortitude while patiently awaiting a reversal of fortunes, the 126th Psalm reminds readers that “those who sow in tears will reap with cries of joy.”

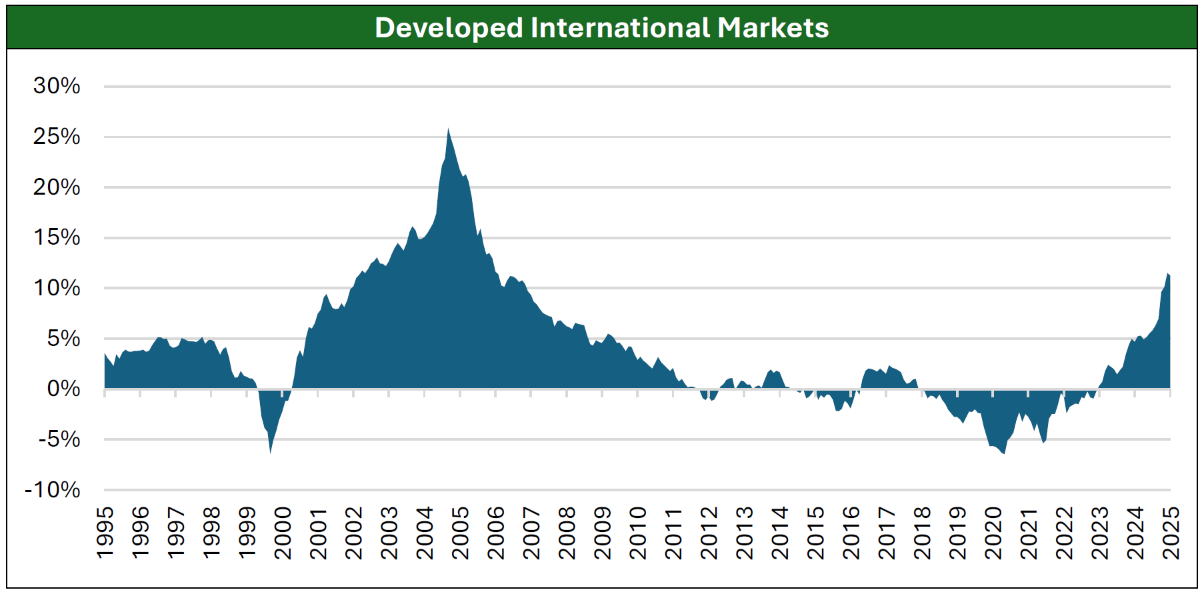

After more than a decade of persevering through a valley of tears since 2010, value investors are finally beginning to reap a fruitful harvest in developed international markets. Over the past five years, the value premium has returned to positive territory in international markets as value stocks have returned to outpacing growth stocks. Since July 2020, value has outperformed growth by 11.6% annualized in developed international markets, according to data from Ken French.

Figure 1: Rolling 5-Year Value Premium (July 1990 – June 2025)

Source: Ken French data library. The value premium is calculated from equal-weight average returns of long value and short growth portfolios.

There are fundamental reasons behind this value resurgence in developed international markets. In Japan, corporate governance reforms and rising shareholder returns continue to propel value stocks that trade at discounts to book value. In the first half of 2025, Japanese firms announced a record amount of total shareholder distributions, building on previous records that were set in the past three fiscal years. While large-cap Japanese stocks have garnered global attention, we believe the most abundant opportunities remain among small- and micro-caps, where most firms still trade at depressed multiples and reform adoption is in its infancy.

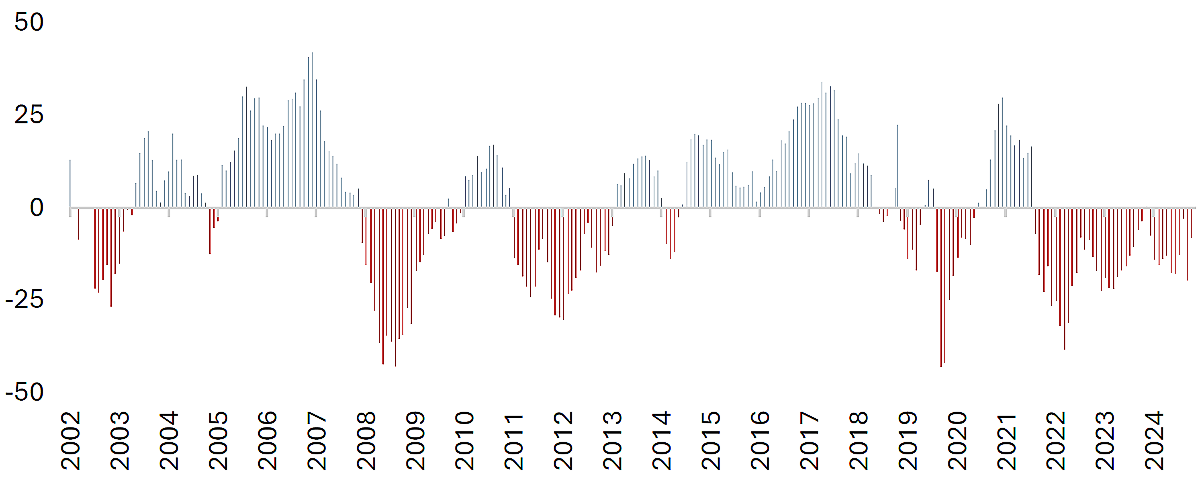

In Europe, improving investor confidence has driven recent inflows into the European market, benefiting value stocks that are priced for pessimism. The Germany-based Sentix Economic Index regularly polls 1,055 investors (including 208 institutions) and measures investor confidence on a scale from -50 to +50, with positive values representing optimism and negative values reflecting pessimism. As shown in the chart below, investors have been consistently pessimistic about the European economy since Russia’s invasion of Ukraine in 2022 triggered an energy and inflation crisis across Europe. However, investor confidence has improved in recent months as Eurozone inflation has returned to the ECB’s 2% target and Germany has approved a €1 trillion infrastructure and defense package. As of June 2025, investor confidence in Europe had improved to a neutral reading of 0.2 in the Sentix Index, after starting the year on solidly pessimistic footing with an index value of -18.

Figure 2: Investor Confidence in the Eurozone Economy (August 2002 – June 2025)

Source: Sentix GmbH (June 10, 2025)

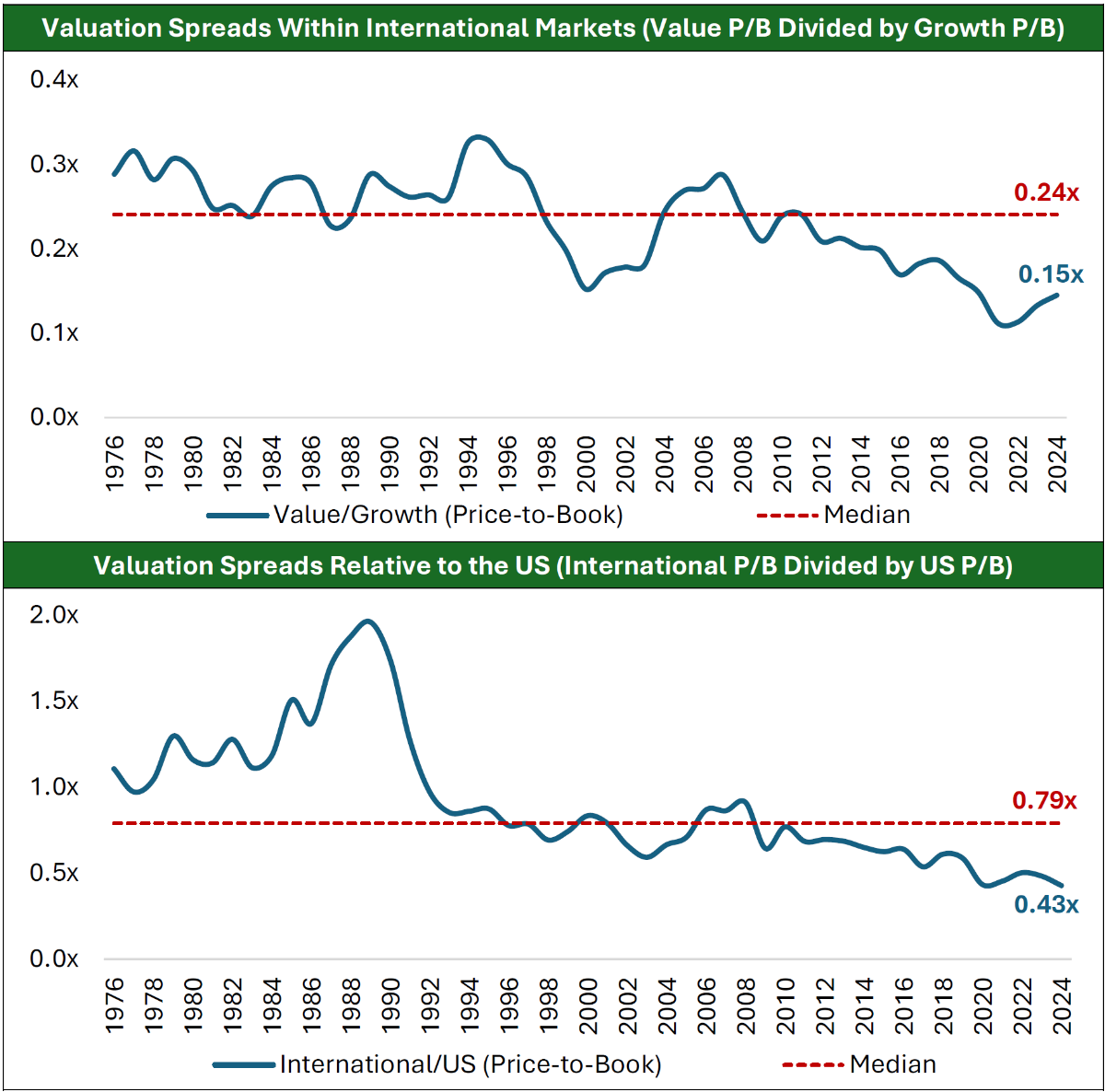

Despite this improving fundamental backdrop and rising investor confidence, international value firms continue to be priced at a “double discount.” Value firms continue to trade near historic discounts relative to growth stocks, and international markets continue to trade at wide discounts relative to the United States.

In the charts below, valuation spreads are measured by dividing the Price/Book of the cheap portfolio by the Price/Book of the expensive portfolio. Therefore, lower ratios signify wider valuation spreads. Within developed international markets, value stocks are currently trading at discounts relative to growth that were last seen during the Dot-Com bubble. And relative to the US, international markets are currently trading at the widest discount on record since 1976.

Figure 3: Price-to-Book Valuation Spreads (1976 – 2024)

Source: Ken French data library

This means that there are at least two potential upside levers for international value stocks going forward. In addition to mean reversion of valuation spreads within international markets, we also believe there is an upside opportunity from narrowing the valuation discount between international markets and the US. We believe that the combination of these two discounts—particularly among small- and micro-cap firms—offers one of the most attractive setups in global equities today.