Factors: The Good and the Bad

Evaluating the best and worst performing equity style factors since 1975

By Chris Satterthwaite with Sasha Cafritz

The original CAPM model published in the 1960s introduced investors to the idea of equity factors with the notion of beta to the market. Some equities had higher sensitivity to the market, and others had lower sensitivity. Differences in risk and return could be explained in part by sensitivity to the overall market.

This idea was extended perhaps most notably by Eugene Fama and Ken French’s publication of the “Three-Factor Model” in 1992, which expanded on the original CAPM model and introduced two new factors, size and value. With this paper, investors could now decompose excess equity returns (returns minus the risk-free rate) into beta to the market, beta to the size factor, and beta to the value factor.

This insight resulted in an explosion of research into equity anomalies over the next 30+ years, creating a “factor zoo” of hundreds of potentially meaningful (and potentially meaningless) factors that could help describe and differentiate drivers of equity returns and risk.

Each subsequently published equity anomaly has tended to become more obscure as the more obvious candidates have already been addressed. Here, we want to take a moment to evaluate which broad themes of investment have fared the best and the worst over the last 50 years.

To do so, we scored over 20,000 US-listed companies since 1975 on the following factors:

Value: cheap vs. expensive (P/B, EV/Sales, EV/EBITDA, FCF yield)

Dividend Yield: trailing 12-month dividends per share divided by current price

Momentum: positive trailing momentum vs. negative trailing momentum

Quality: high GP/assets vs. low GP/assets

Profitability: ROE, ROA, ROIC

Leverage: debt/equity, debt/total assets

Earnings Volatility: standard deviation of historical earnings

Growth: trailing five-year growth in sales, operating income, net income

Volatility: trailing volatility of returns

Size: market cap, total assets, and total sales

Turnover: trading volume scaled by shares outstanding

Investment: annual growth in total assets

Once we scored the companies and standardized their exposures with z-scores, we ran monthly cross-sectional regressions to recover the implied monthly factor premium for each factor, controlling for each company’s coincident factor exposures.

Below, we show how these factor themes have performed since 1975.

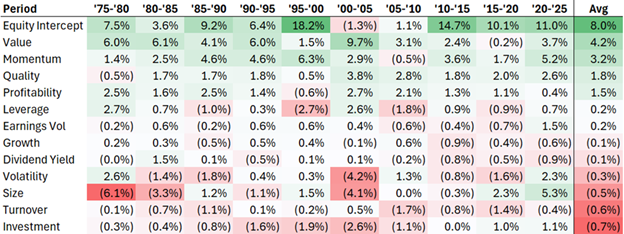

Figure 1: Avg. Annualized Return by Factor over 5Y Periods

Source: CRSP/Compustat, Verdad analysis

Since 1975, US equities have delivered strong performance, with annualized excess returns of approximately 8% over the past 50 years. Over the long run, value, momentum, and quality have been the best performing style factors, while large size, high turnover, and high investment have been the worst performing style factors.

Notably, the most recent 10- to 15-year period has been somewhat anomalous, with historical laggards like high investment, high turnover, large size, high volatility, high earnings volatility, and high leverage all delivering positive returns, while value has been underwhelming relative to history.

Whether the most recent period is the new normal or an outlier remains to be seen, but the five-year snapshots of factor performance over the last 50 years are surprisingly consistent in terms of the relative ranking of equity style factors.

But returns are only part of the story. We can also look at volatility and implied Sharpe ratios to see how these factors have behaved.

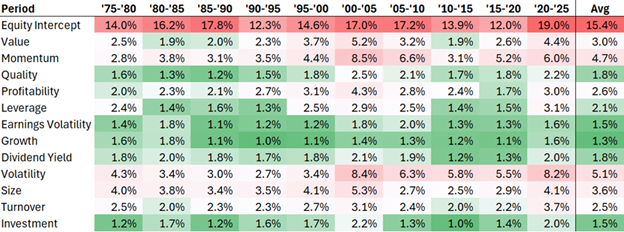

Figure 2: Avg. Annualized Volatility by Factor over 5Y Periods

Source: CRSP/Compustat, Verdad analysis

Unsurprisingly, the equity market has the highest volatility, with volatility, momentum, and size factors as the highest volatility factors, while growth and investment have some of the lowest volatilities. Combining returns and volatility, we can examine Sharpe ratios for each style factor.

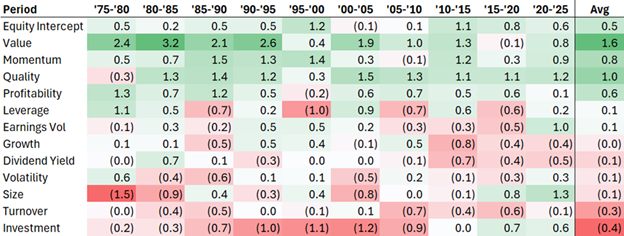

Figure 3: Avg. Sharpe Ratio by Factor over 5Y Periods

Source: CRSP/Compustat, Verdad analysis

This is where investable factors in quant portfolios really stand out. The high volatility of the equity market results in a much lower Sharpe ratio than some standalone factors, despite the high returns that the market earns.

Value is a standout, while quality, momentum, and profitability all have Sharpe ratios above the equity market. Meanwhile, the negative returns and low volatility of high investment have made it an attractive factor to short (albeit painful over the last 5-10 years).

Much ink has been spilled (some by us) about whether the value factor is dead. Undoubtedly, recent history has seen an inversion of the relative ranking of style factors. But the consistency of the historical record for the stalwarts of value, momentum, quality, and profitability and the laggards in turnover and investment is quite striking.

As investors, our best predictions of the future are informed by the past. While recent history has favored large size and high investment, we believe a portfolio that favors exposures to value, momentum, quality, and profitability has precedent on its side.

Acknowledgment: Sasha is a rising sophomore at Yale University, originally from Washington DC. He is a proud alumnus of St. Albans School. He is majoring in Economics and is a rower on Yale’s Heavyweight Crew. Sasha enjoys playing poker, keeping up with the Commanders, and plans to work in investment banking after graduation.