Narrative Economics

Nobel Prize–winning economist Robert Shiller has just published a major new book: Narrative Economics: How Stories Go Viral and Drive Major Economic Events. Shiller won the Nobel for arguing that markets were not pure utility maximizing machines but rather distinctly human phenomena shaped by culture and opinions.

In his new book, Shiller argues that the economists need to take stories more seriously, that stories shape human action, and that a serious study of those stories is essential to understanding what moves markets.

“The field of economics should be expanded to include serious quantitative study of changing popular narratives,” he writes. “Narratives are major vectors of rapid change in culture, in zeitgeist, and ultimately in economic behavior.”

In college, I studied history and literature. The scholars who pioneered this field argued that to understand history, we had to understand literature—that novels, poems, songs, and art were important reflections of and shapers of historical events. And so, despite being a quantitatively oriented investor, I am deeply sympathetic to Shiller’s arguments.

In fact, I believe Shiller’s work offers cutting insights into today’s financial markets. Shiller advocates textual analysis as a way of quantifying narrative developments, relying heavily on Google’s NGrams and Google Trends applications to data mine and show the rise and fall of historical narratives. Inspired by Shiller’s approach, I reviewed dozens of popular finance terms, many sourced from Twitter, and ran them systematically through Google Trends to see the rise and fall of popularity in these terms from 2004 to the present. I then grouped the terms together to tell a story—a story of the stories driving today’s markets.

Let’s start with the most fun set of terms: the viral ideas driving the most crazed investor excitement and the most extreme valuations. Below, I show charts with data from Google Trends giving the quantity of searches for six terms from 2004 to the present: FAANG, fintech, payments, platform business, recurring revenue, and SaaS software.

Figure 1: The Most Exciting Investing Ideas

Source: Google Trends

Google Trends data suggests these are the darlings of the US growth stock universe: the sexiest, most exciting, most faddish investing ideas. Every day, a major fund company launches a new fund focused exclusively on fintech or SaaS software, and the valuations rise ever higher. And you can see the interest spiking for each of these terms.

Let’s abstract one level higher from types of companies to styles of investing. The charts below show the search trends for five terms that capture approaches to investing: asset allocation, low volatility, passive investing, the S&P 500, and safe stocks.

Figure 2: Changing Styles of Investing

Source: Google Trends

Investor interest in asset allocation has dived since the financial crisis. Investors are much more excited about passive investing, with the S&P 500 as the darling index of the passive investing surge. Aside from passive investing in the S&P 500, investor interest in minimum volatility and safe stocks has risen significantly. Beyond purely passive investments in the sexiest index, investors would prefer their stocks safe and less volatile.

These narratives do, of course, conflict. SaaS software companies and fintech payments businesses that trade at double-digit multiples of revenue are not “safe stocks” nor “minimum volatility.” And as investors in AOL and newspaper stocks discovered, if customer tastes or willingness to pay changes, the fact that the revenue is recurring and subscription based won’t make a whit of difference.

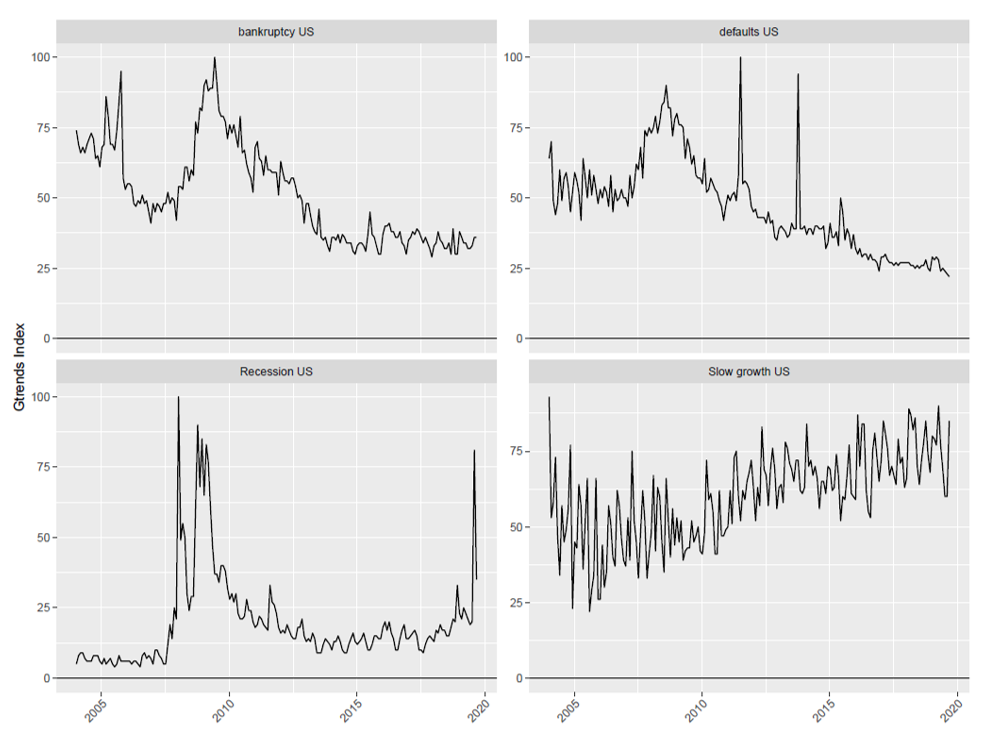

But we can understand why investors are pursuing this barbell approach (minimum volatility, safe stocks and the S&P 500 index on one hand and high-growth, super-sexy software and fintech business on the other) by looking at what search terms tell us about the economy. Below I show four charts: bankruptcy, defaults, recession, and slow growth.

Figure 3: The Economy

Source: Google Trends

Search interest in bankruptcy and defaults is near all-time lows, supported by extremely accommodative monetary policy and a robust economy. Yet investors are very concerned about a potential recession and about a “new normal” of slow growth. Investors have cycled out of “slow growth” cyclical and GDP-dependent companies and cycled into companies that are “recession resistant” or “high growth.” Many of these high-growth businesses are buying revenue growth and taking on large amounts of debt to do so, but the lack of defaults mean that risk is far less salient than the risk of “slow growth” or “recession.”

Shiller observes that it is difficult to determine causality. Do narratives drive economic behavior or reflect it? But he is clear that these stories shift rapidly, that investor tastes and desires fluctuate. In his seminal 1981 paper, Shiller showed that changes in fundamentals can only explain a tiny percentage of market fluctuations, that changes in valuation multiples explain 80% or more, and that those valuation multiples are driven by perceptions and stories about the future.

And so, as a warning to those investors piling into popular narrative stocks, let’s look at one of the narratives of a prior decade: the enormous surge of interest in the 2000s in emerging markets and commodities that peaked in 2007.

Figure 4: Last Decade’s Investing Fad

Source: Google Trends

Will minimum volatility, safe stocks, SaaS software, Fintech, platform businesses and other “in” investing ideas follow this same trajectory? Are they priced to perfection? Is investing as easy as just buying the S&P 500? And are those cyclical and GDP-dependent businesses that are all but forgotten in today’s market really worth so little?