Improving our Europe Strategy

Quantitative investors are historians. We study the past to learn its lessons. But we are also pragmatists. So we seek to turn our insights into principles and then make those principles turn a profit.

Over the past six months, our quantitative work at Verdad has been devoted to aggregating the research we have done on US and Japanese markets, combining that research with lessons we have learned from trading stocks in our global fund and Japan fund, and testing those collective insights in European markets.

Our goal was to turn these lessons from history into principles for making profitable investments and improve Verdad’s strategy for investing in Europe. In this note, we will share our methodology and results.

Methodology

Our research was conducted on European equity data from S&P Capital IQ over the 21 years between June 30, 1997, and December 31, 2017. We started from the set of signals that we were using to rank stocks in the US and Japan, all of which have met the basic threshold of being logical and supported by empirical evidence.

Then we subjected each of these signals to three tests. First, for each signal, we divided the universe of European leveraged small value equities into deciles to ensure that the highest ranked companies had historically delivered higher returns than the lowest ranked companies. This served as a simple test of whether each signal could spread returns within our target universe. Second, we ran regressions of returns against individual signals to ensure that each factor had a statistically significant relationship with returns on a standalone basis. Third, we tested the significant signals in combination with each other to ensure that none of the factors were redundant. At the end of each step in this process, we eliminated weak signals in order to develop a parsimonious model that focuses on a small number of highly impactful factors.

Results

The signals we found most useful in Europe fall into three main categories: quality, value, and momentum. Our quality signals included a company’s probability of paying down debt and its profitability. Our value signals included EBITDA relative to enterprise value, free cash flow yield relative to equity, and book value relative to market value. And our momentum signal was the prior 12 month stock price return. Figure 1 shows the average annual returns of each decile.

Figure 1: Decile Return Spreads of Individual Signals, 1997–2017

Sources: S&P Capital IQ and Verdad Research. The universe is formed from the cheapest 25% of the market and the 50% most levered stocks in the market each year, excluding microcaps.

As you can see, each of these six signals ranks stocks within the universe by expected return. In each case, there is a substantial spread in returns between the top and bottom deciles. And the tenth decile of each signal has very attractive returns.

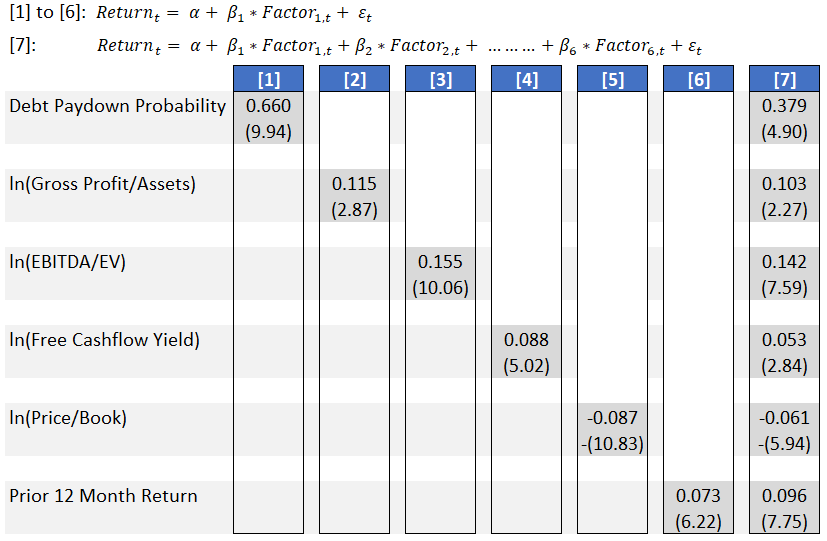

Having found initial evidence that these signals can spread returns, we wanted to test whether these relationships are statistically significant. We achieved this through regression tests, which are presented in Figure 2 below. In regressions 1 to 6, we regressed returns against each signal on an individual basis. The coefficients show the size of the effect, while the t-statistic shows the statistical significance (a t-statistic above 2 is the minimum threshold of significance, while many academics believe higher requirements of 3 or 4 are necessary to feel confident that an effect is significant). Regression 7 tested the six signals in combination with each other. Each of the six signals remains statistically significant when combined with the other five, which suggests that none of these six signals are redundant.

Figure 2: Regressions of Returns Against Individual & Combined Signals, 1997–2017

Sources: S&P Capital IQ and Verdad Research.

We then looked at how a model that combines these six signals would have ranked stocks in-sample between June 30, 1997, and December 31, 2017. This model is applied to the same universe described above, excluding illiquid stocks with low trading volume.

Figure 3: In-Sample Test of European Ranking Algorithm, 1997–2017

Sources: S&P Capital IQ, Ken French Data Library, and Verdad Research.

Figure 3 suggests that a diversified strategy of selecting the 50 highest ranked European stocks in each year would have earned an annualized return of 20.7% with a Sharpe Ratio of 0.94 between June 30, 1997, and December 31, 2017. This European Leveraged Small Value Strategy would have outpaced the Fama/French Europe Small Value Index by 7.5 percentage points per year. Not only did the top ranked stocks have higher returns, they also had higher debt paydown probabilities and actually paid down debt more frequently than lower ranked stocks.

What are the risk exposures of the European Leveraged Small Value Strategy? As we have written about in the past, our strategy is sensitive to investors’ fears of credit default risk, as measured by changes in the high yield spread. In the US, when high yield spreads widen by 1 percentage point, leveraged small value equities decline by around 4.7 percentage points on average. A similar relationship holds in Europe, with the returns of a leveraged small value strategy declining by 4 percentage points on average when high yield spreads widen by 1 percentage point. As indicated by the second and third columns in Figure 4, these spikes in high yield spreads also tend to affect the broader equity market since markets are integrated.

Figure 4: Regressions of European Equity Returns vs. Changes in High Yield Spreads, 1997–2017

Sources: St. Louis Fed, S&P Capital IQ, Ken French Data Library, and Verdad Research. The European Leveraged Small Value Strategy represents annually rebalanced portfolios of the 50 highest ranked European stocks.

Figure 5 evaluates the European Leveraged Small Value Strategy’s exposure to the Fama and French factors. In the first regression, we use the Fama/French Three Factor Model to explain the strategy’s returns. In the second regression, we extend the Three Factor Model to account for momentum.

Figure 5: Regressions of Leveraged Small Value Strategy Returns vs. Fama/French Factors

Sources: S&P Capital IQ, Ken French Data Library, and Verdad Research. The European Leveraged Small Value Strategy represents annually rebalanced portfolios of the 50 highest ranked European stocks.

There are three important takeaways from the analysis in Figure 5.

First, the annualized intercept (alpha) of this strategy has a t-statistic above 4, which is well beyond the conventional threshold of 2. This suggests that the historical outperformance that we observe in the data for the European Leveraged Small Value Strategy is unlikely to have occurred by chance.

Second, the sensitivity of this strategy to changes in the European market return is less than 1, which indicates that the European Leveraged Small Value Strategy would provide diversification benefits to investors who hold the market portfolio.

Third, the European Leveraged Small Value strategy has positive exposure to the size premium and the value premium, as we would expect.

Conclusion

The past can be every bit as difficult to interpret as the future is to predict. And the greatest pitfall to avoid is the temptation to spin the past to fit a favored hypothesis. There’s an old Soviet joke that, under communism, “the future is certain; it’s the past which is unpredictable.” If you’ve never seen a bad backtest, you can understand the relevance to quantitative investing!

We do our best to bring a rigorous empirical approach to investing by carefully vetting each factor we use with a battery of tests. And we share that research in order to find any problems with our analysis and to ensure that our investors fully understand the approach we are taking.

Our goal is to design robust investment strategies that we and our clients can stick with over the long haul. We start by confirming each signal’s sensibility and consistency with financial theory. Then we test these signals over a long series of historical data to confirm that they would have been effective in sorting stocks by expected return. To be comfortable that these factors will continue to be effective in the future, we test them out of sample to confirm that they work in different time horizons and across markets. We believe the end result is an investment process that is robust and built on a solid foundation of quantitative research.

Ultimately, the most important factor for investment success is maintaining a long-term perspective. The future is inherently uncertain, and even the strongest factors can temporarily fall out of favor and produce disappointing results over the short term. We believe the risk of these occasional drawdowns is the reason why long-term investors should expect to be compensated for holding small, cheap, leveraged equities. In our view, as long as people have different tolerances for risk, there will be a premium available to the subset of investors who are willing to hold undervalued securities over the long haul and harness the power of compounding to perform above the benchmark.