Global Valuations

Major international stock markets have outperformed the US market over the past year. This is a sharp break with the longer story over the previous 3-, 5-, and 10-year periods, when US markets dramatically outperformed international markets.

Figure 1: US Market Returns vs. International Market Returns through 3/31/2018

Source: Capital IQ for pricing on Vanguard Europe, iShares Japan, Vanguard Emerging Markets, Vanguard Total International Stock Index, and Vanguard Total Stock Market Index

The long stretch of US outperformance has left a significant valuation gap, with the US trading at significantly higher multiples than other countries. Because individual valuation metrics are noisy, in Figure 2 below we compare the US to other major international markets on three different metrics and then rank them by equal weighting for each valuation metric.

Figure 2: International Valuations

Source: Capital IQ for EBITDA/EV, Star Capital for P/S and P/B

International markets trade at lower multiples of EBITDA, sales, and book value than does the US. Today, the top 50 companies on our European screen trade at 5.9x EBITDA, as compared to 5.4x EBITDA in Japan and 7.2x in North America. In our view, Europe today provides a very attractive set of opportunities to discerning value investors.

We believe Japan is the single biggest source of cheap stocks, but opportunities for value also abound in Europe. Some countries in developing Europe—Russia, Poland, and Italy—trade at lower valuations than Japan.

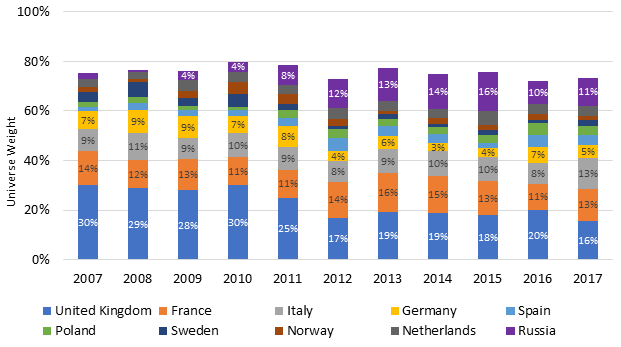

The backtest of our European strategy delivered compelling returns in part by shifting each year into the cheapest countries in Europe, taking advantage of the varying economic conditions in different parts of the continent. Below, we show the 10 largest country weights within our target universe of European leveraged small value equities between 2007 and 2017.

Figure 3: 10 Largest Country Weights in European Leveraged Small Value Universe, 2007–2017

Sources: Capital IQ and Verdad Research

Today, our model sees the greatest number of opportunities in the UK, France, Italy, Germany, and Russia.

The differences between individual country valuations can be substantial at any point in time. In our view, this variation in valuations creates opportunities for globally diversified investors to capture the premiums offered by cheaper markets. Allocating across international markets that have limited correlations to each other could reduce overall portfolio risk.

Figure 4: Correlations of Leveraged Small Value Strategies in the US, Japan, and Europe

Sources: Capital IQ and Verdad Research

It is impossible to predict whether Europe, North America, or Japan will have the best performing market over the next three to five years. But we do know today’s valuations. And if today’s valuations predict future returns, then weighting portfolios more heavily to international equities might be a smart move.