Drivers of Deep Value: International Evidence

Evaluating the components of deep value returns in Europe and Japan

By: Brian Chingono

Value is the proverbial “buy low and sell high” strategy, but how does it actually work? There are two sides to every trade, so why would a trader sell a company at a bargain-basement price, only to see another investor reap the reward over time?

In their seminal paper, “Factors from Scratch”, our friends at OSAM analyzed US equity data from 1964 to 2017, drawing the following conclusions about value:

Companies generally fall into the “value” category because of some underlying uncertainty in their earnings trajectory. This uncertainty is reflected in a lower stock price, and hence a lower valuation.

An annually rebalanced value strategy systematically buys into this uncertainty, anticipating that the companies’ underlying fundamentals are more stable than the pessimistic views embedded in the cheap price.

As value companies’ fundamentals stabilize in years two to four of a hold period, their valuation continues to re-rate through multiple expansion. This multiple expansion begins in advance of a robust improvement in fundamentals, with the steepest re-rating occurring in the first 12 months of a hold period. Therefore, the initial return boost from multiple expansion generally offsets the earnings weakness in the first 12 months prior to stabilization.

We expanded on this US research by testing it on data from international developed markets. Our findings in Europe and Japan were broadly similar to the original US research: multiple expansion tends to offset earnings weakness during the first 12 months of holding international value portfolios. A novel finding in our study is that deleveraging is also very important for returns in deep value strategies. And the magnitude of return contribution from deleveraging is economically meaningful at around 3 to 4 percentage points per year in deep value.

Our analysis is based on a regression of one-year forward returns in international deep value companies against three explanatory factors:

Deleveraging over the next year

Multiple expansion over the next year

EBITDA growth over the next year

The regression seeks to explain one-year forward returns according to these three drivers over the same time period. The portfolios are rebalanced annually every June, so the regressions explain international deep value returns over a one-year hold period.

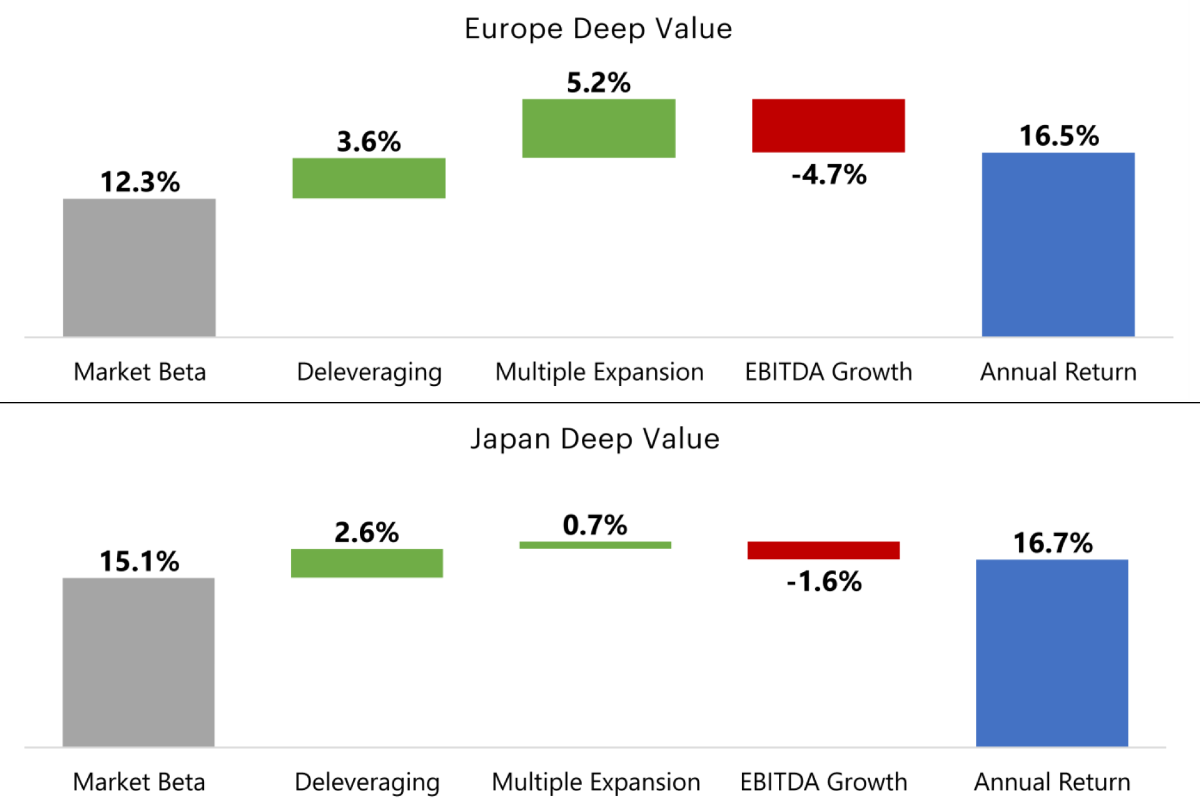

A summary of the return contribution from these drivers is presented below. In each geography, the baseline return labelled “Market Beta” is the intercept from the regressions; this is the total return (including dividends) that comes simply from holding stocks that are more volatile than the market. Return contributions from the three return drivers—deleveraging, multiple expansion, and EBITDA growth—are shown over a one-year hold. Together, these components add up to the average annual return across all stocks in our deep value sample from June 1997 to June 2020.

Figure 1: Return Bridge in International Deep Value (Jun 1997 – Jun 2020)

Source: Capital IQ and Verdad research.

As expected, deleveraging and multiple expansion tend to contribute positively to returns in deep value, while earnings growth tends to be a negative contributor over a one-year hold. Consistent with the US research from OSAM, this is because value strategies buy into uncertainty at each rebalance, and it takes about 12 months for earnings to stabilize. In anticipation of that stabilization, forward-looking investors begin to re-rate the companies’ valuation multiple within those first 12 months, providing a return boost through multiple expansion. At the same time, companies that are facing economic uncertainty have every incentive to pay down debt and strengthen their balance sheet. Hence, we also see a positive return contribution from deleveraging in the first 12 months of holding a deep value portfolio.

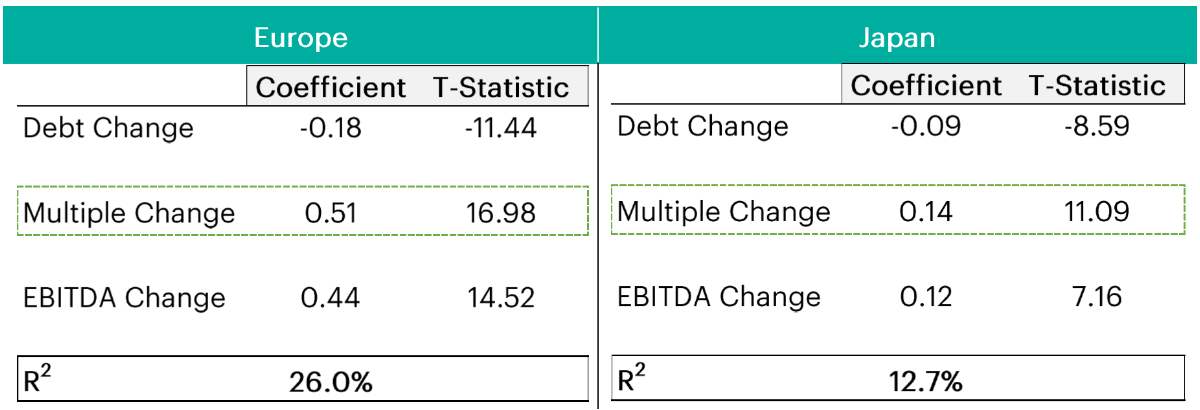

To evaluate this process more closely, we can look at the regression coefficients, which are summarized in the figure below. These coefficients represent the sensitivity of deep value returns to each driver: the larger the magnitude of a coefficient, the more important it is in determining return outcomes in deep value. The return contributions we saw in Figure 1 were obtained by multiplying these coefficients by the average value of each variable in our sample. For example, in the European sample, the average change in net debt was a -20% reduction and multiplied by a coefficient (i.e., sensitivity) of -0.18, this gave a positive return contribution of 3.6% from deleveraging over a one-year horizon.

In the figure below, notice that in both geographies, forward returns have the highest sensitivity to changes in the valuation multiple. In addition to being the most economically important variable, the change in valuation multiple is also the most statistically significant factor in both geographies.

Figure 2: Regression of International Deep Value Returns (Jun 1997 – Jun 2020)

Sources: Capital IQ and Verdad research

Looking ahead, we believe these regression results contain good news for value investors.

First, in an environment potentially characterized by rising interest rates, companies with leverage have an incentive to pay down their debt (or at least, not borrow a lot more) to contain interest expenses. And as we have written before, companies that are likely to deleverage can be systematically identified with around 65% accuracy, based on information in their financial statements relating to their track record of paying down debt in the past and their capacity to continue deleveraging going forward. This driver is particularly attractive for European deep value where levered companies dominated the universe in the data shown above and continue to do so today. By contrast, the Japanese deep value universe shown above contains a 50% mix of net-cash companies.

Second, after the last two decades, European and Japanese deep value are cheaper on a relative and absolute basis. After over a decade of widening valuation spreads between growth and value, we’ve reached a point where value is near its cheapest point on record relative to growth in almost all geographies. Since valuation multiples are mean reverting, we would expect some amount of multiple expansion in deep value over time. This driver is very attractive in Europe, and especially attractive in Japan, as deep value stocks are now 19% and 43% cheaper on Price/Book in Europe and Japan (respectively) than they were at the beginning of the horizons shown above.

And third, there is one exception to the general rule of earnings growth being a drag on deep value returns: during recoveries from recessions, value stocks grow like growth stocks, as we’ve shown both in Japan and Europe.

While value can earn handsome returns over long horizons with only two out of three cylinders firing, the combination of all three of these drivers working in a positive direction during economic recoveries makes crisis periods a particularly good time to consider doubling down on deep value.