Beating the Index in Bonds

Beating the index in equities is extremely difficult. Over the last 10 years, only about 15% of large-cap US equity managers beat the S&P 500.

Bonds are different, with a big divergence between investment-grade and high-yield indices. Half the investment-grade bond managers beat the investment-grade index while only 3% of high-yield managers beat the index.

Figure 1: Percent of Funds BeatingTheir Benchmark over 10 Years

Source: SPIVA U.S. Scorecard. Year-end 2018.

In its case for low-cost index-fund investing, Vanguard shows the same story in greater detail. The charts below compare active funds (blue dots) and index funds (red dots) to their benchmark (horizontal line). The diagonal line represents the regression line of expenses versus returns.

Figure 2: Ten-Year Annualized Excess Returns vs. Expense Ratio

Source: Vanguard. Y-axis ranges from -15% to 15% for equities and -5% to 5% for credit. X-axis ranges from 0% to 3%. Data as of December31, 2018.

The results for equity and high-yield bonds are largely what we’d expect: fund performance is below the index, driven primarily by fees (high yield looks worse than equity because the y-axis scales are different). But for investment-grade bonds (intermediate-term credit), performance is well above the index. In fact, the index funds that track the index seem to represent the floor on performance.

Why do investment-grade bond managers seem to consistently beat the index, and why do high-yield managers so consistently fail? And what lessons should investors take away from this data about how to win in bonds?

The story of why investment-grade bond managers win so consistently is simple: the index is full of very low-returning AAA and AA assets. Managers who underweight those assets in favor of A and BBB bonds do better over time. Both AQR and Vanguard have written lengthy white papers explaining this in depth. We can see this phenomenon in the chart below—A and BBB bonds do significantly better than AAA and AA bonds.

Figure 3: Returns by Rating 2008–2018 and 2009–2018

Source: Bloomberg Barclays.

The same is not true for high-yield managers. CCC and B bonds do not reliably beat BB bonds. In fact, over long periods, BB bonds actually outperform the lower rated B and CCC bonds, a phenomenon we call “fool’s yield.”

So what should investors who want the higher returns available in high yield do? The solution for equity investors has been to use index funds and ETFs to achieve performance in line with the index. As our friend Preston McSwain sometimes jokingly says, equity index funds should be called Relative AlphaTM funds as they consistently outperform relative to their peers (and yes, he has received approval for a trademark for this phrase). We agree with Preston on this point and also share a common view on high-yield bonds.

Index ETFs have not been a good answer for high-yield bond investors. Whereas index funds that track the S&P 500 achieve returns almost perfectly in line with the index, high-yield ETFs have a 1% to 1.5% performance drag. That’s massive underperformance.

Figure 4: Equity ETF (SPY) vs. S&P 500 and High-Yield ETF (HYG) vs. Benchmarks

Source: Capital IQ.

This underperformance is due to liquidity and fees. By necessity, due to their promise of daily liquidity, high-yield ETFs track a liquid high-yield benchmark which itself underperforms the index. In addition, the fees on the high-yield ETFs are relatively high. While SPY has an expense ratio of 9 basis points, HYG has an expense ratio of 49 basis points. In short, investors are giving up a lot in terms of performance and fees for the high-yield ETF.

Unlike in equity, the right answer has been to use actively managed funds to access high yield. These funds are not constrained to the most liquid issues, and in general they have significantly outperformed the ETFs, despite charging 75bps versus an average of 45bps for the two ETFs.

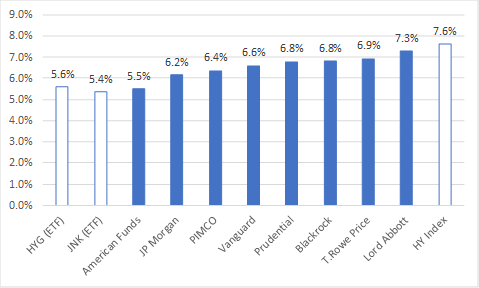

Figure 5: Returns for ETFs, Large Actively Managed HY Funds, and the HY Index, 12/31/2007–7/31/2019

Source: Capital IQ. Fund returns are for retail share classes.

Active funds beat passive ETFs in high yield, but they still trail the index after fees. Are investors forever limited to earning index minus fee returns in high yield?

We think not. There are three things we believe high-yield investors should do to improve returns.

The ETFs underperform partially because they focus on the most liquid bonds. Funds able to take more illiquidity risk due to smaller capacity and less liquid redemption terms should be able to outperform passive ETFs.

A small amount of leverage could compensate for the drag from trading costs. We estimate that with 1.25x margin leverage, every one of the active funds we show above would have beaten the high-yield index.

High-yield bonds offer decreasing incremental returns for more risk. To outperform, investors should seek a higher quality skew than the index. At the outset, this looks like lower yield, but this is the path to higher returns.

The high-yield index has been very hard for managers to beat, but we believe this difficulty is a feature of an interesting asset class. The investment-grade index is easy to beat but has only returned 5.5% since 12/31/2007. The high-yield index is harder to beat, but it has returned 7.6% over the same period while the BB portion of the index returned 8.0%, just behind the S&P 500 total return index of 8.6% over the same period. High-yield returns come with lower drawdowns and volatility, so even modest leverage can make a high-yield fund an attractive equity alternative.

By owning less liquid bonds, focusing on higher quality bonds, and using a modest amount of leverage, we think it is possible to beat the high-yield index.