An Apology for Noise Traders

Since the Great Depression, academics have wrestled with the excessive volatility of markets. Starting with John Burr Williams and extending to the present date, these scholars have developed progressively more complex models to price financial securities, yet time and again these models fail to explain market volatility. But why?

Andrei Schleifer, the most cited economist of all time, has put forth a simple yet elegant theory. The reason asset pricing models do not work is that the market is not comprised only of “rational arbitrageurs” but also of unsophisticated investors, known as “noise traders.”

Schelifer argues that if the market were composed only of rational arbitrageurs, there would be a linear relationship between the prices predicted by academic models like CAPM and observed prices in the market. But noise traders intervene, trading irrationally and disrupting the linear relationship, as illustrated in the below graph:

Figure 1: Dynamics of Noise Trader Share

Source: Noise Trader Risk in Financial Markets

We won’t bother to explain this graph, other than to admire the perpendicularity of the axes, the intellectual elegance of the Greek lettering, and the arrows that represent the noise traders’ pernicious influence on what would otherwise have been a straight line.

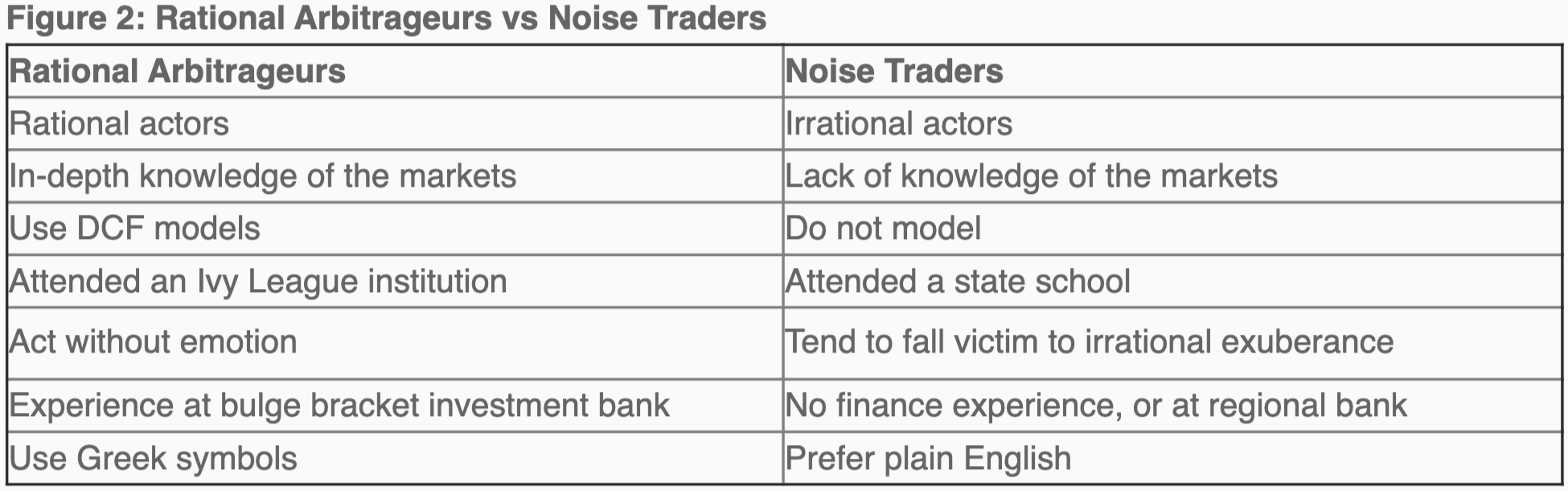

We can summarize Schleifer’s perspective thus: the asset pricing models in use at the University of Chicago and Harvard are dead-on accurate, but their implementation is complicated by the presence of idiots who trade stocks irrationally. He divides the world of market participants into two broad buckets, the labelling of which we have endeavored to complement with more definitional rigor than the paper provides:

Figure 2: Rational Arbitrageurs vs Noise Traders

Most academics love this self-flattering model, and scholars have cited the noise trader paper 5,368 times in academic journals. But is this model right? Is there some set of rational arbitrageurs whose brilliance is only hidden by the irrational behavior of idiots?

Stanford economist Mordecai Kurtz offers an alternative perspective. Kurz contends that all agents lack certain structural knowledge, including the demand function of other agents, which makes it impossible for any investor to compute the true value of a stock: “the beliefs of agents are, in general, wrong in the sense that they are different from the true probability of the equilibrium process. These beliefs are, however, rational.”

The volatility and noise of markets derives not from the irrationality of a set of under-educated actors but rather from the inherent complexity of the world in which we live and the wicked problem of investing in a market that is always changing states and offering new and unpredictable events and sentiments.

Casting aside the models of Williams and Schleifer, we might instead assume that the future is fundamentally unpredictable and entertain the robust empirical observation that “expertise” in the various sub-disciplines of futurology may in fact reduce our predictive accuracy rather than improve it. Under such assumptions, “noise” might be an appellation better ascribed to what we hear coming from the faculty lounge.