A Tale of Two Bankruptcy Regimes

Early English bankruptcy statutes in the 17th and 18th century were viciously punitive by modern standards. Even when the concept of discharge from debt was introduced in 1705, allowing a debtor to keep 5% or residual assets, the penalty for a noncooperative debtor was that they would “suffer as a felon without the benefit of clergy”—a pre-Victorian euphemism for the death penalty.

By contrast, America began as a debtor’s nation. Virginia in 1642, facing a labor scarcity, promised five years of debt protection to lure settlers; James Oglethorpe created Georgia as a debtor’s refuge in 1732 for those headed to English debt prisons; even Jefferson and Washington owed considered amounts to foreign merchants—Jefferson, notoriously delinquent, had to pawn his Monticello estate to settle his debts.

Instead of enslavement or imprisonment, the United States decided to allow debtors—corporations and individuals alike—to declare bankruptcy. Early American insolvency law reform started slow, with such liberal initiatives as allowing debtors to choose involuntary servitude rather than prison. However, with the 1898 Federal Bankruptcy Act, the concept of a “fresh start” for unfortunate debtors was solidified in US law.

Our loose bankruptcy laws shape our economy. They encourage borrowers to take chances with others’ money, knowing that failure won’t lead to a lifetime of indentured servitude. Bankruptcy encourages businesses and individuals to look forward, to take chances with new investments, to conduct research and development, to make daring bets on future growth. And if these projects fail, as some inevitably do, insolvency regimes determine how to deal with it.

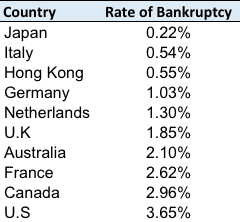

This system creates a volatile market for equity owners. Compared to other G20 nations, the United States rate of bankruptcy is the highest.

Figure 1: Bankruptcy Rates among G20 Nations (Commercial Bankruptcies, 1990–1999, Divided by Total Number of Firms)

Source: Claessens and Klapper, “Bankruptcy around the World: Explanations of its Relative Use”

Japan, by contrast, has the lowest rate of corporate bankruptcies.

Unlike in the US, where Wall Street banks will securitize and sell on the corporate debt they originate, Japanese banks have long-term relationships with the companies they lend to. This is called the keiretsu system. The banks provide financial services as well as debt and will often invest in the equity of the companies to which they lend.

Because of this close relationship, when a company is struggling, the Japanese banks are far more likely to evergreen the loans than to declare bankruptcy. This was most obvious when the Japanese real estate bubble burst in the early 1990s. The banks, afraid that a capital write-down would force them below Basel-ordered minimum capital levels, began offering loans to their weakest borrowers to keep them solvent. The banks wanted to keep de-facto dead firms alive (hence the term “zombie company”) to avoid having to write off capital when the impaired loan turned nonperforming. The Japanese regulators encouraged this practice.

Japan’s economy is far healthier and larger than it was in the 1990s, but these banking practices are still in place and Japanese bankruptcies remain extremely rare.

We see in the US and Japan a tale of two bankruptcy regimes. In America, culture and institutions believe in creative destruction, offering bankruptcy as a way out. America prioritizes growth and innovation over stability. Japan, in contrast, frowns on bankruptcy and prefers a patient approach to dealing with troubled companies that makes the economy more stable and the market less volatile.