Reversals

Eugene Fama won the Nobel Prize in Economics in part for his work finding that small-cap value stocks outperformed the broader market. Harry Markowitz won the Nobel Prize in Economics in part for his work advocating diversification.

But attempting to follow this seemingly sound advice—and strong empirical work—has not exactly benefitted investors of late. Based on our research, small-cap value stocks have lagged the broader US market by a massive margin. International stocks have lagged US stocks by a massive margin. And international small-cap value has been a wasteland from a return perspective. Below is a chart comparing the annualized returns for the last five years through August of 2019 for funds investing in the US market, international market, US small-cap value, and international small-cap value.

Figure 1: Five-Year Annualized Equity Returns through 8/31/2019

Source: Capital IQ. US Market is Vanguard’s Total Stock Market fund. International Market is Vanguard’s Total International Market. US Small Value is Vanguard’s Small Cap Value fund. International Small Value is Dimensional Fund Advisor’s International Small Cap Value fund.

The small-cap value premium and the benefits of international diversification might be Nobel Prize–winning ideas—and the empirical research might be highly statistically significant and brilliantly done—but a high-IQ approach to investing has severely lagged the S&P 500 for a decade now.

Yet a curious thing has happened in the last two months: a sharp shift in momentum. Recently, egghead investing seems to have come back into fashion. Below are the returns for these four styles over the past two months.

Figure 2: Returns from 8/31/2019 to 10/31/2019

Source: Capital IQ. US Market is Vanguard’s Total Stock Market fund. International Market is Vanguard’s Total International Market. US Small Value is Vanguard’s Small Cap Value fund. International Small Value is Dimensional Fund Advisor’s International Small Cap Value fund.

Will this trend continue? Will high-IQ investing make a comeback? Or is it past time to fire the eggheads and go all in on the S&P 500?

Some of the most insightful quantitative analysts on Wall Street believe this reversal has legs and that international and small-cap stocks could be set for serious outperformance. Though each of these firms uses a slightly different methodology, the basic idea is to look at what has predicted long-term returns in the past (most significantly valuations) and then compare where we are today to history. Below is a table summarizing the perspectives of multiple quantitative analysts on return expectations of these major asset classes (none of these firms specifically forecast small-cap value, so I have included their broad small-cap forecasts). Vanguard and Morningstar forecast nominal returns, while AQR, Research Affiliates, and GMO forecast real return. To make them apples-to-apples, I added the breakeven inflation rate to the real forecasts so all numbers are nominal.

Figure 3: Nominal Return Forecasts

Source: Vanguard, AQR, Research Affiliates, GMO, Morningstar

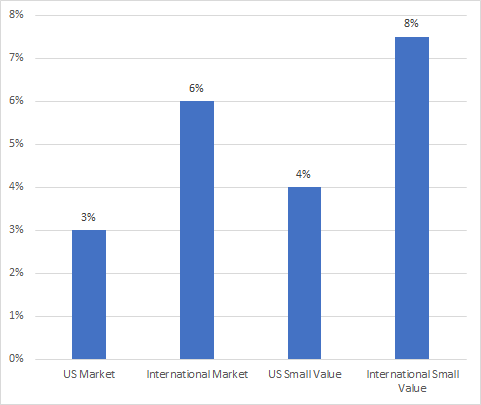

Based on our analysis, all five firms believe that international equity markets will outperform the US equity market over the next decade, with an average forecast of 3% annual returns for the US market and 6% for international markets. There were no specific forecasts for small-cap value, but the two firms that projected small-cap returns both assumed that small caps would beat large caps, on average by 1.5%. So if we average the forecasts, their return expectations for the next decade look something like the below.

Figure 4: Average Nominal Return Forecast

Source: Vanguard, GMO, Research Affiliates, AQR, Morningstar, Verdad

This would mark a sharp reversal from the past decade. In fact, it would represent a near perfect mirror image of the last decade’s returns. This is consistent with the work of Nobel Prize–winner Richard Thaler, who famously found that portfolios of prior losers outperform those of prior winners over a long horizon.

We believe the best predictor of future returns isn’t the last 5–10 years of experience. Rather, markets tend to be mean reverting, with yesterday’s winners being tomorrow’s losers. Just examine the below chart by decade of US versus international growth and value stocks.

Figure 5: Style Returns by Decade

Source: Capital IQ

Returns have been atrocious for small-cap value and international stock portfolios over the past decade. Investors may well be tempted to give up on international and small-cap value completely. But a recent reversal in trends, and the forecasts of multiple different but empirically based quantitative models, suggest that betting on a reversal could be the better course.