Quality or Value – Why Not Both?

High quality doesn't come cheap in large caps, but the story is different in small caps

By: Chris Satterthwaite and Lionel Smoler-Schatz

Would you rather own a portfolio of cheap, low-quality companies or a portfolio of expensive, high-quality companies?

When it comes to owning US large-cap equities, those are essentially your choices. Higher quality companies should command a premium valuation, and the top of any simple value screen is often filled with highly asset-intensive or cyclically sensitive businesses. It’s often easy to see why these sorts of companies don’t command a premium valuation.

However, this trade-off between value and quality primarily seems to be a large-cap phenomenon. In small caps, discerning investors can have their cake and eat it too, buying high-quality companies at cheap prices.

To illustrate this point, we scored the equity universe on the value factor (EV/sales, EV/EBITDA, P/E, P/B) and the quality factor (GP/assets). We then looked at the correlation between value and quality factor scores, separating the universe into large and small caps (defined as having a market cap <$1B) for both the US and international equities.

Figure 1: Value and Quality Correlation

Source: Capital IQ, Verdad analysis

Interestingly, US and international large caps seem relatively efficiently priced, in the sense that higher quality companies are less cheap, and cheap companies tend to be of lower quality. We can see this with a few examples below.

Figure 2: Cheap and Expensive Large-Cap Equities

Source: Capital IQ, Verdad analysis

NVIDIA, Recruit Holdings, and On Holding all command premium valuations but simultaneously boast very impressive gross profit to asset conversion. The cheaper large-cap companies can often be more capital-intensive businesses, like Southwest Airlines, Nippon Steel, and BT Group.

For small caps, we find that this relationship does not hold. In fact, the inverse is true. Value and quality tend to be positively correlated, which is unintuitive on the surface, unless you believe that small caps are less efficient.

An illustrative sample of global small, cheap, and high-quality companies (as measured by GP/assets) is shown below:

Figure 3: Cheap and High Quality

Source: Capital IQ, Verdad analysis

While the analysis shown above only looks at quality as measured by GP/assets, we also looked at quality as measured by a blend of ROE, ROA, ROIC, and EBITDA margin and saw the same trends emerge.

Buying small, cheap, high-quality companies isn’t just an interesting or prudent thing to do. It can also translate into higher returns, as shown below.

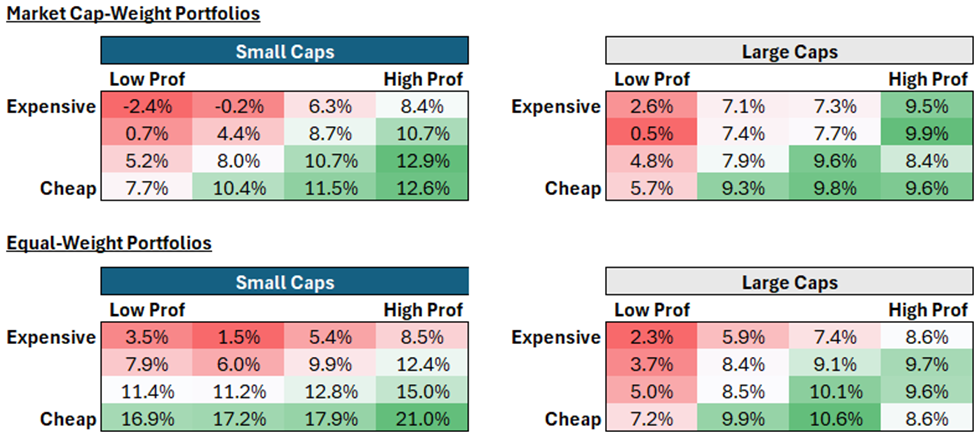

Figure 4: Global Annualized Returns for Portfolios Sorted by Value and Profitability

Source: Ken French Data Library

The highest return portfolios were cheap, high-quality small caps, with the equal-weighted portfolio outperforming the market-cap-weighted portfolio. In our opinion, a capacity-constrained strategy that can pursue the intersection of small, cheap, and high quality will have more success in capturing the returns presented here.

For investors unwilling to compromise on both value and quality, we believe small caps are likely to present the most compelling opportunities.