Market Share & Profitability

The empirical problem with competitive strategy

By: Daniel Rasmussen

There is no empirical evidence that a company's market share predicts its profitability. But that hasn't stopped academics, business school curricula, and management consulting firms from promulgating the idea for decades.

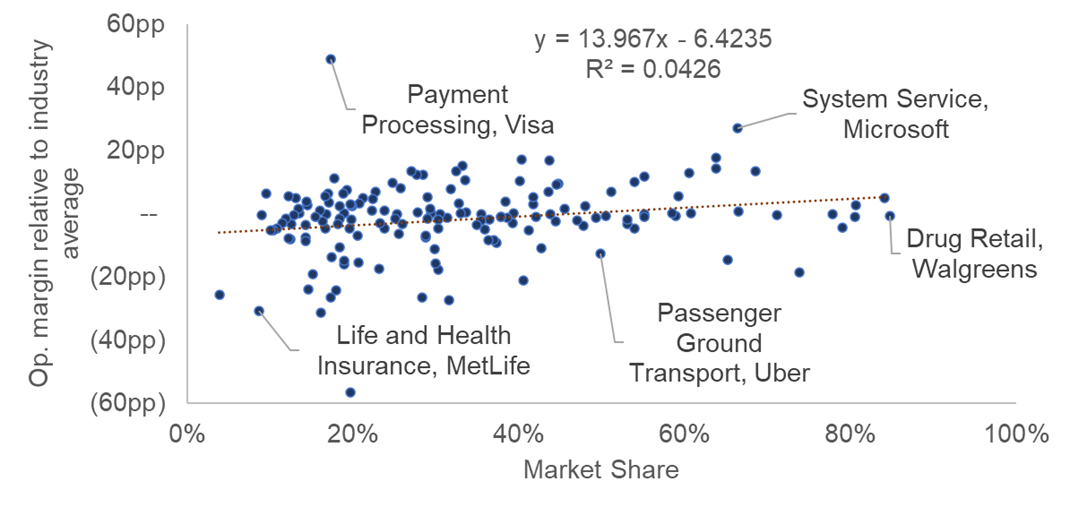

We looked at all US and Canadian public and private firms with >$10M in sales across Capital IQ’s 11 sectors and 160 industries—a total of ~6,600 firms. We compared the operating margins of the largest firm in each industry to the industry average. This corrects for margin differences between industries and attempts to isolate over- or under-performance by the market leader. Market share is computed as firm revenue divided by total revenue generated by businesses within a specific industry. The chart below shows a scatter plot of market share for public and private companies relative to their profitability versus the industry average.

Figure 1. Impact of Market Leadership on Industry-Relative Profitability

Source: Capital IQ, Verdad analysis

This chart shows that market share is not a consistent indicator of firm performance. And this finding holds true across industries, with many illustrating a negative relationship between market share and profitability.

Take broadline retail. In this industry, firms with large market shares tend to run lower margins, perhaps reflecting the fact that lower prices tend to attract more customers.

Figure 2. Broadline Retail Profitability vs. Market Share

Source: Capital IQ, Verdad analysis. Note: Top ten firms by revenue shown for ease of visualization.

Lina Khan might find this to be an "antitrust paradox,” but it’s actually firm strategy operating exactly as her Chicago School opponents would envision. Consumers choose Amazon because of the low prices, driving Amazon’s market share, and allowing Amazon to invest more in lowering prices and improving service. Khan worries that focusing only on consumer costs and benefits has led the FTC to ignore the rise of powerful companies like Amazon. Implicit, of course, in Khan’s arguments is the idea that the relationship between market share and profitability doesn’t hold water—if the relationship held there wouldn’t be an antitrust paradox.

The non-relationship holds true across industry after industry, some with positive-sloping trendlines, others with negative, but all with sub-25% determination coefficients (and many with 1-5%). We also tested other performance metrics. The chart below shows the market leaders across industries by market share and their associated ROA.

Figure 3. Market Share vs. Return on Assets

Source: Capital IQ, Verdad analysis

Note, again, the virtually non-existent relationship between market share and financial performance, as well as the presence of firms with low market share within their industry but high ROA, like Visa, or high market share but relatively low ROA, like Best Buy. The chart below shows ROE.

Figure 4. Market Share vs. Return on Equity

Source: Capital IQ, Verdad analysis

Anti-capitalist academics would love to believe that profits derive from companies exploiting their market power, but the reality is companies earn their market share through a better product, better pricing, better service, or a litany of other firm-specific strategic decisions. It's actually quite rare to see the number-one company in an industry earning far above-market profit margins. In our dataset, 90 companies—or 56% of the industry-leading public firms—have margins below the industry median.

Simply buying a competitor and then squeezing customers might be a strategy that worked in the age of Vanderbilt and Rockefeller—or it might have been a myth even then. After all, those titans of industry sought market share as an end in and of itself, pursuing vertical and horizontal integration often at the expense of robust profit growth. Standard Oil, for example, generated roughly flat profits from 1882 to 1890 at the zenith of its market share, ~90% in the US. Today, we continue to see virtually no relationship between market share and operating margins in the energy industry, as the chart below shows.

Figure 5. Energy market share vs. profitability

Source: Capital IQ, Verdad analysis. Note: Top 25 firms in the industry plotted for ease of visualization.

We believe companies looking to generate high margins would be best off focusing on targeting those high margins directly by cutting costs, raising prices, or producing higher-margin products. It’s odd that strategy theory says that the best path to obtaining profitability is by growing market share. Shouldn’t strategy be teaching you to define your aims more clearly?

The most robust study to claim a relationship between market share and profitability is a 2018 meta-analysis in a marketing journal that finds a single percentage point of market share generates a ~13% increase in profitability (a result unsupported by our own data analysis). But even if you believe this suspect finding, this meta-analysis assesses seven marketing variables associated with profitability, and market share was fifth on the list. So maybe strategy should be teaching managers to pursue any of the higher-elasticity variables like customer satisfaction, brand equity, or better marketing analytics and forecasting capabilities.

We wrote about the hollowness of market share–based strategies in “The Gospel According to Michael Porter.” But little has changed in academia or consulting since the study. Harvard Business School continues to teach Michael Porter and his ideas as the fundamental theory of modern strategy in its first-year “Strategy” course, and you would be hard-pressed to avoid mention of his ideas in business school classrooms around the world. The market-share conception of strategy finds purchase in major consulting firms, too, with BCG’s continued celebration of Bruce Henderson’s growth share matrix or McKinsey’s studies that tout market share gains as important strategic aims independent of other performance outcomes.

In the absence of an alternative, Porter’s dominance in strategic thought—from academics, to business schools, to consulting firms—is likely to remain uncontested. Unless, of course, we dare to think more critically about what drives firm performance. “A foolish consistency is the hobgoblin of little minds,” as Emerson wrote. We worry that a single-minded focus on market share hobgobbling the minds of business schools and corporate leaders.