Japan's Dividend & Buyback Surge

Japan Exchange Group says the market reform is only 20% complete

By Naoki Ito

Public companies in Japan have made unprecedented strides in returning capital to shareholders over the past few years. As the Tokyo Stock Exchange (TSE) continues to pressure firms toward greater capital efficiency, dividends and buybacks have hit record highs. It is a transformation long overdue in corporate Japan, where bloated balance sheets and inadequate capital allocation decisions have dragged down shareholder value creation.

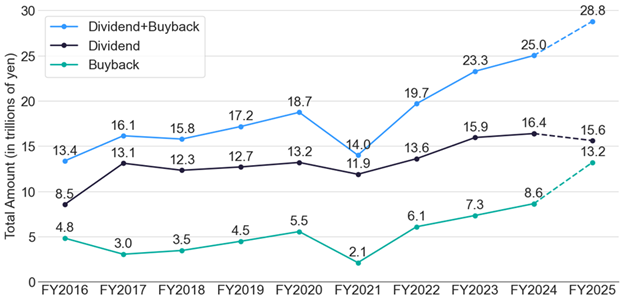

As shown in Figure 1, total annual shareholder payouts have more than doubled over the past decade. TSE-listed companies are on pace to deliver a fourth consecutive year of record dividend payments. More notably, executed share buybacks in FY2025 have already largely surpassed last year’s level, putting Japan on pace for its fourth straight year of record repurchases.

Figure 1: Total Dividends and Buybacks of TSE-listed Companies by Fiscal Year

Source: IR BANK, Verdad analysis. Note: FY2025 only includes companies that posted full fiscal year results by July 2025 (~70% of total number of companies).

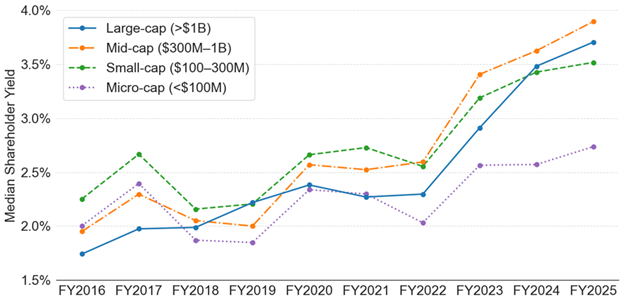

This trend isn’t confined to large-cap firms. Small- and mid-cap firms are participating just as actively and at scale. Figure 2 illustrates the historical median shareholder yield—dividends plus buybacks as a percentage of market capitalization at the start of the fiscal year. The upward trend is clear across the size spectrum, reflecting a nationwide pivot toward shareholder payouts.

Figure 2: Historical Median Shareholder Yield of TSE-listed Companies by Market Cap

Source: IR BANK, S&P Capital IQ, Verdad analysis. Note: FY2025 only includes companies that posted full fiscal year results by July 2025 (~70% of total number of companies).

In a capital market long characterized by deep value traps and corporate inertia, the embrace of shareholder returns signals improving capital discipline and seems to be reshaping investor perception. As we highlighted in our research in April, firms committing to higher payouts tend to have experienced greater stock price appreciation than others over the past two years.

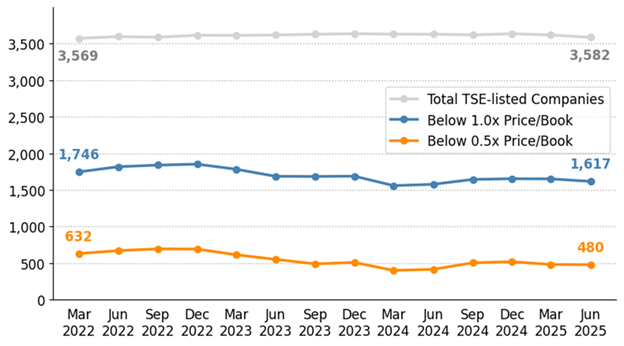

Valuations are gradually improving as a result. Since the TSE restructured its market segments in 2022 to direct companies to achieve better capital efficiency and corporate governance, the number of listed firms trading below book value has declined by 7%, while those trading below half book value have dropped by 24%, as shown in Figure 3.

Figure 3: Number of TSE-listed Companies with P/B below 1.0x and 0.5x

Source: S&P Capital IQ, Verdad analysis.

Yet this nationwide transformation is far from over. Japan Exchange Group CEO Hiromi Yamaji recently remarked that the reform effort is only 20% complete.

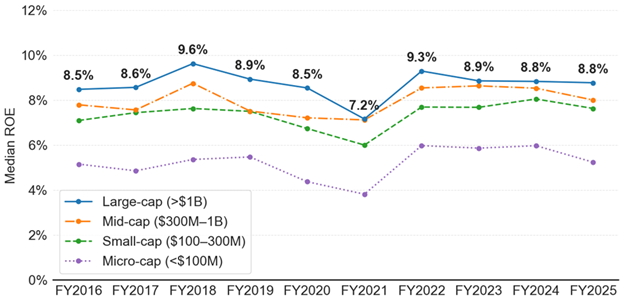

In our interpretation, his view underscores an important point: the goal is not merely to boost payouts but to reshape how companies think about using capital at hand. Dividends and buybacks are tools, not strategies in and of themselves. Their purpose is to return excess capital that cannot be productively deployed within the business. We believe the movement is in the very early stages of realizing its intention: improving capital productivity to generate stronger bottom-line results. Figure 4 reveals that return on equity (ROE) has remained stagnant across all market-cap segments for over a decade.

Figure 4: Historical Median ROE of TSE-listed Companies by Market Cap

Source: S&P Capital IQ, Verdad analysis. Note: FY2025 only includes companies that posted full fiscal year results by July 2025 (~70% of total number of companies).

Despite record payouts, there has been no median improvement in firms’ ability to convert equity into earnings. This suggests that the true objective of capital efficiency reform—earning more with less—remains largely unmet.

Although increasing shareholder payouts and preventing further balance sheet bloating is prudent, management teams need greater scrutiny and must take bold action to dispose of idle assets and redistribute the capital to improve earnings per unit of capital deployed. Obvious measures include unwinding cross-shareholdings and selling rental real estate, but more drastic actions—such as selling off underperforming business segments—may well be worth considering.

Take Mitsubishi Chemical (4188.T), for example. It is executing a decisive management plan to focus on its Chemicals segment, the core business where management is both passionate and confident about driving growth. As part of the “selection and concentration” of its business portfolio, the company decided this year to sell its sizable Pharma segment (Mitsubishi Tanabe Pharma), which accounted for 30% of total EBIT last year, for $3.4 billion. It plans to use the proceeds from the sale to accelerate the growth of its core business segment.

The purpose of corporate reform is not simply to hit a payout target but to embed an enduring discipline in capital allocation, one that supports the long-term compounding of strong operational returns. Dividends and buybacks have their place when a company lacks superior internal investment opportunities, but they shouldn't be deployed reflexively. What drives sustainable growth is not the volume of cash returned to shareholders but the quality of the returns the business generates. This era’s success will hinge on how fully management embraces the principle of capital efficiency.