Is South Korea the next Japan?

Looking for value in "Value-Up"

By: Daniel Rasmussen & Anne Lee

South Korea’s equity market looks like an exaggerated version of the Japanese stock market. Japan has a massive pool of companies trading at below 1x price-to-book, but South Korea has an even larger share. And while Japan is famous for its “lost decades,” the Japanese market has taken a sharp upward turn, while the South Korean market continues to languish.

But Korean regulators are trying to imitate Japan’s success. Last year, the Financial Services Commission (FSC) and the Korea Exchange (KRX) introduced the “Corporate Value-Up Program,” modeled after Japan’s successful Tokyo Stock Exchange reforms. Much like the Japanese equivalent, this initiative encourages Korean companies to voluntarily disclose plans to enhance shareholder value.

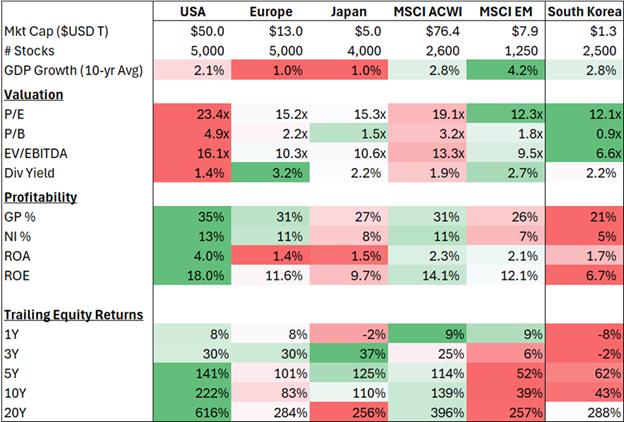

The Korean market’s problems are obvious. Over 70% of Korean stocks trade below a price-to-book (P/B) ratio of 1. This value gap is known colloquially as the “Korea Discount.” This is largely a result of a long period of terrible equity market returns. The chart below compares the South Korean market to global peers on valuation, profitability, and trailing returns.

Figure 1: Comparative Equity Market Statistics

Source: Bloomberg, Verdad analysis

Significant international attention to the potential for reform is building. FTSE Russell recently announced Korea's pending inclusion in its developed market indices, and Korea continues actively working to meet MSCI's stringent market accessibility criteria—a move that could inject approximately $44 billion of additional foreign capital into Korean equities. South Korea has a larger market capitalization than 14 of the 23 countries in the MSCI Developed World Index (second only to Japan in Asia), meeting all of the quantitative criteria to be included.

However, South Korea ranks low in some of the qualitative characteristics, most notably openness to foreign investors. Foreign investors require an Investor Registration Certificate issued by Korea's Financial Supervisory Service (FSS) as well as other procedures not typically required in comparable developed markets. However, regulators are now attempting to address these issues and abolish some of these requirements.

And corporate South Korea is dominated by family-owned conglomerates called chaebols. Samsung, SK, Hyundai Motor, LG, and POSCO are five of the largest chaebols today, accounting for an impressive 50% of South Korea’s GDP. While these chaebols were effective in leading Korea's “Miracle on the Han River” period of rapid industrialization, the chaebol’s opaque governance, insular and rigid management structures, and misaligned incentives are now starting to be seen as an obstacle to equity market value creation. One particular challenge is that Korea’s high inheritance taxes mean Korean chaebols are incented to keep share prices low to ensure they can pass their companies onto the next generation.

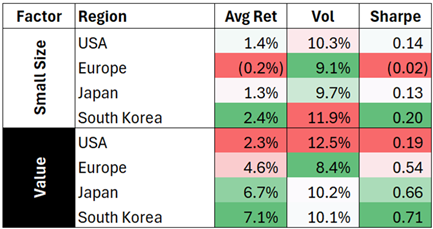

But despite these obstacles, and the underwhelming performance of South Korean equities, factor portfolios have actually performed quite well in South Korea. Since 2000, the return to the size and value factors in South Korea has exceeded the US, Europe, and Japan.

Figure 2: Comparative Style Factor Performance

Source: Ken French Data Library, JKP Factor Library

South Korea’s Value-Up Program could be a continued driver of these premiums if the reforms are able to capture the same momentum as in Japan. A presidential election is set for June 3rd. The leading liberal candidate, Lee Jae-myung—well known for his support of chaebol reform—has expressed commitment to revising the Commercial Act. Proponents argue the revisions would better protect minority shareholders and align with the goals of Value-Up. Detractors in the corporate world fear they are too extensive and might undermine chaebols more than support shareholders.

As South Korea continues to wrestle with such debates, these challenges might also represent the very opportunity investors seek. With continued reform, increased foreign accessibility, and growing corporate accountability, the "Korea Discount" could reward patient investors willing to stomach near-term uncertainties.

Acknowledgments: Anne Lee is a rising senior at Yale University studying history with a concentration in global economics. She is interested in the intersections of finance, geopolitics, and law. Beyond the classroom, she spends her time with the Yale Political Union and hopes to join the polo club next year. She will be interning this summer at Goldman Sachs.