Flipping the Script on FX

This is the final installment of our three-part series exploring the underperformance of currency markets and strategies since the great financial crisis. This week, we propose a multi-factor portfolio that shorts the highest-carry currencies when they are most likely to crash.

By: Verdad Research

Our year-long investigation of systematic currency strategies turned up three strategies that turned out to be almost completely unprofitable, highly correlated with one another, and to carry a crash risk that coincides with equity drawdowns. Nassim Taleb artfully describes certain Wall Street strategies as “picking up pennies in front of a steamroller.” The FX strategies we studied all seem to fit this profile.

And so, perhaps, the better strategy is to bet on the steamroller and let others pick up the pennies. Or, to mix metaphors, if classic systematic FX strategies go up by the stairs and down by the elevator, why not go down the stairs and up the elevator by shorting these strategies?

After all, returns have been meager and seem to crash at the worst times, so wouldn’t the reverse offer zero returns in good times, until suddenly returns start coming in just when you needed them to offset losses in equities? The chart below shows a hybrid short index of high-carry emerging-market currencies with a history of crashing (the Mexican peso, Brazilian real, Russian ruble, South African rand, Thai baht, and Indonesian rupiah) plotted with the MSCI Emerging Market equity index. Equities are on the left axis and currencies are on the right axis.

Figure 1: Short EM FX vs. Long MSCI EM

Source: Thomson Reuters Datastream, Capital IQ

Over this period, this illustrative short carry strategy returned 1.7%, the MSCI EM returned 8.6% compounded, and the two series were -77% correlated. While the short EM currency strategy doesn’t appear attractive on its own, even with perfect hindsight, this chart illustrates the appeal of a risk-off FX strategy as a hedge for equity investors.

Figure 2 helps us consider the merits of a short currency position relative to other common volatility hedges like gold and treasuries. The regression panel highlights the relationship between volatility and 11 asset categories. Assets with negative beta values (e.g., small-cap value) are short volatility and perform poorly when volatility increases. Conversely, assets with positive beta values (e.g., a long USD short EM FX strategy) perform well when volatility increases. While the short EM carry strategy’s absolute beta values are not considerably high, they are in a similar territory as gold and 10-year Treasurys, underscoring the efficacy of the strategy as a hedge against volatility.

Figure 2: Relationship with Volatility

Source: Thomson Reuters Datastream, Capital IQ, Bloomberg

After concluding that shorting traditional FX strategies might be more interesting than going long, we set out to identify how to pick out the worst performing of these crash-prone currencies. To do this, we analyzed six distinct crash events: Mexico 1994, Thailand and Indonesia 1998, Russia 1998, Brazil 1999, and South Africa 1999.

We found that each of these six currency crashes were preceded by decreases in current account (signaling an increase in a country’s imports relative to exports), increases in depository rates, and decreases in spot rates. We also looked at trends in industrial production, foreign direct investment, and consumer price indices, but found these measures had less reliable relationships with forward returns, which is not surprising given the academic literature.

Figure 3: Return Spreads for Mexico, Brazil, Russia, South Africa, Thailand, Indonesia (1980–Present, or Earliest Available)

Source: Thomson Reuters Datastream, Trading Economics

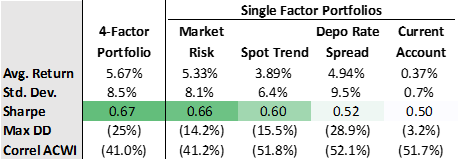

We subsequently created a multi-factor model that incorporated insights from our study of crashes together with our understanding that currency drawdowns are most severe for the highest interest rate currencies and tend to coincide with local market drawdowns (which is why we included equity market risk in the model, a signal also identified in the academic literature). Figure 4 shows the results of combining these signals in a multi-factor portfolio. The portfolio shorts currencies when any three of the following four criteria are met: the currency is in top quartile of depository rate spreads to the USD, exhibits a negative trend in its exchange rate, exhibits a negative trend in its current account, or exhibits a negative trend in its local stock market.

Figure 4: Factor Portfolio Performance (1992–Present)

Source: Thomson Reuters Datastream, Trading Economics

The four-factor portfolio generates 5.67% average returns with an 8.5% standard deviation and a 0.67 Sharpe ratio. The strategy has a -25% max drawdown and a -41% correlation with MSCI EM.

As we highlighted in our emerging markets crisis investing whitepaper, markets of developing countries tend to crash frequently. As a result, long-term investors employing buy-and-hold strategies haven’t fared well. We think the short currency strategy illustrated here, or a version of it, could be successfully coupled with an EM equity portfolio. Shorting emerging market currencies should provide investors with liquidity at the exact moment the assets in these markets become most attractive.

Figure 5 illustrates how adding a currency short can add drawdown protection to an otherwise long-only EM equity strategy. Across four drawdown events since 2000, a 60/50 levered portfolio of EM equities and a four-factor FX short strategy averaged drawdowns of -18.5% versus -41.5% for the equity-only portfolio.

Figure 5: Drawdown Protection Provided by 4-Factor FX (2000–2020)

Source: Thomson Reuters Datastream, Capital IQ

In sum, the carry trade is akin to going up the stairs and down the elevator. Gains come incrementally and crashes come swiftly and coincide with equity market drawdowns. In this instance, we think it is much more interesting to go down the stairs and up the elevator. Paying incrementally to bet against the riskiest and most crash-prone currencies offers equity investors an attractive hedge in moments of crisis. Data indicate that fundamental and time-series-based factors can improve our ability to select the best short positions and capture the greatest upside at the precise moment we need it most: when equity markets are drawing down.