Europe: Private Equity's Last Stand

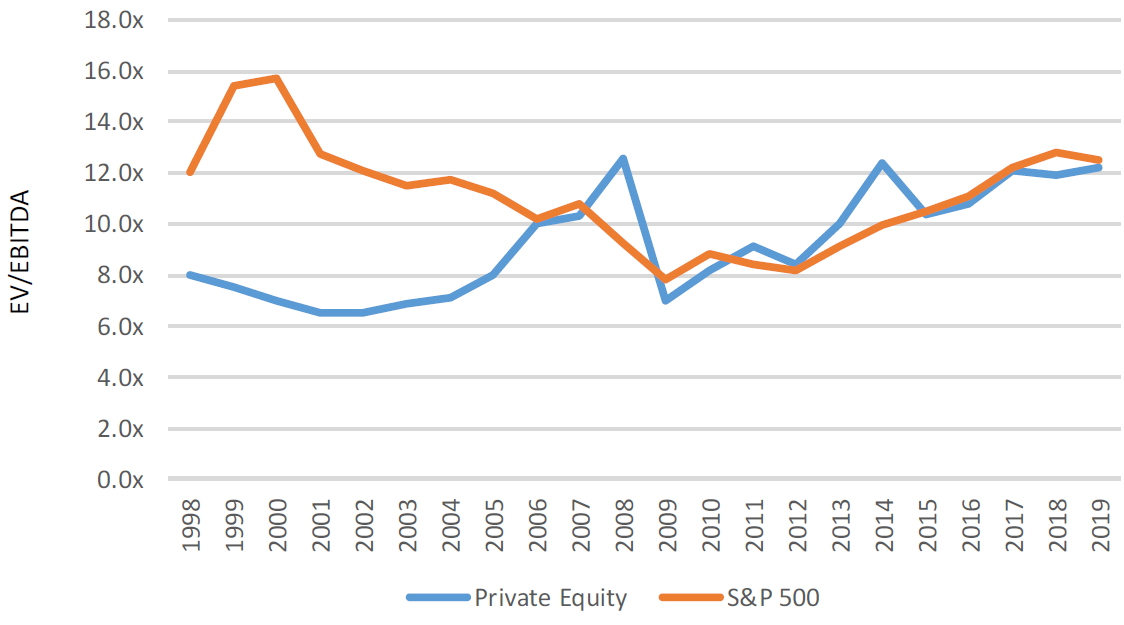

In the 1990 movie Pretty Woman, Edward Lewis—the private equity manager played by Richard Gere—describes how he makes money from the companies he buys: “I don't sell the whole company. I break it up into pieces, and then I sell that off; it's worth more than the whole.” While the movie goes on to compare this description to the operations of a chop shop for car parts, it’s worth noting that Edward had a point. A significant portion of private equity’s historical outperformance came from buying companies at low valuations in private markets, cutting their fat by discontinuing unprofitable operations, then selling the juicy, profitable portions at a higher valuation through an IPO on the stock market. This valuation arbitrage worked as long as private equity could buy companies at a discount to the stock market. Prior to 2006, US private equity firms enjoyed a 30%+ valuation discount on their purchases, relative to public markets. But that valuation gap has since closed as investors have poured more money into private equity, chasing the handsome returns from PE’s gilded age in the 1990s and 1980s.

Figure 1: US Private Equity Valuations vs. S&P 500 Valuations

Sources: S&P Capital IQ and Pitchbook (June 2019).

The closing of private equity’s valuation discount in the US has profound implications for expected returns going forward. For example, Research Affiliates forecasts that, after inflation, US private equity will deliver a measly 0.2% real return over the next decade.

We believe this forecast makes sense since the average private equity transaction in the US is done at a 12x EV/EBITDA valuation, which translates to a heavy debt burden of 6x Debt/EBITDA. As a result, 98% of private equity deals in the US are rated B or below, where the bankruptcy rate is above 20%.

Yet across the pond in Europe, private equity fundraising is booming as PE firms raise record amounts for their European buyout funds. This year alone, Carlyle, KKR, and Permira set records by closing their largest European buyout funds ever.

Is something materially different about leveraged buyouts in Europe versus the US?

It appears the answer is “yes”. The difference is based on the most crucial ingredient for leveraged buyouts: price. Today, the average purchase multiple in European private equity is 9.4x EV/EBITDA versus 12.2x EV/EBITDA in US private equity. In addition to European PE being cheaper than its US counterpart, European PE firms also buy companies at a discount to European public markets, which trade at 11.7x EV/EBITDA.

Cheaper valuations make a big difference for expected returns. Research Affiliates forecasts a 6.8% real return for European PE versus 0.2% for US private equity over the next decade. The components of this return forecast are yield (cash generated by PE-owned companies, which can be used to pay dividends or pay down debt), fundamental growth in earnings, and changes in valuation multiples, as illustrated below.

Figure 2: PE Expected Returns Over Next 10 Years

Source: Research Affiliates, LLC (“Research Affiliates”)© (Nov 2019). Real returns are net of inflation.

Since valuations are lower in Europe, yields today are higher for European PE (4.7%) versus US PE (2.3%). Real earnings growth is expected to be similar across both continents at 2%, in line with long term historical averages. But since US private equity buys levered companies at expensive valuations, it is more vulnerable to multiple compression over the next decade, and this effect is expected to subtract 4 percentage points from expected returns going forward. As we have written before, there are at least two ways for multiple compression to materialize in US private equity.

The first is bankruptcies; buying expensive companies with leverage creates an unsustainable debt burden. According to Moody’s, the credit ratings of PE-owned companies in the US imply an expected bankruptcy rate of around 20% going forward. The second is an inevitable unraveling of the EBITDA “adjustments” that US private equity firms have increasingly resorted to making in order to mask the expensiveness of their deals. S&P Global has found that these adjustments tend to overstate EBITDA by 30%, with the truth being laid bare within two years after a leveraged buyout. Based on this evidence, we believe it is very plausible that valuation multiples in US private equity could compress over the next decade.

It appears Europe is private equity's last stand. While European PE should live to fight another day, it seems US private equity is primed to be a Waterloo.

For the time-being being, it appears European PE managers are sticking to the formula that made private equity great in its early days: buy companies at a discount to public markets. Cheap buyouts only require a moderate amount of leverage, resulting in a manageable debt-to-income ratio.

That is why our Europe fund invests in the very cheapest levered companies in public markets. Today, our portfolio trades at a valuation of 6.5x EV/EBITDA. At the same leverage of 50% Debt/EV as private equity, our portfolio companies have a very manageable debt-to-income ratio of 3.2x Debt/EBITDA.

Figure 3: Valuations in Private Equity and Verdad Europe

Sources: Pitchbook, Capital IQ, and Verdad research (September 2019).

We are able to access the cheapest opportunities in the market because we're disciplined about keeping our fund size below capacity. While we'll never raise record fund sizes, we do have a list of cheap European companies that generate substantial cash flow for deleveraging and could be taken private at a premium—in case the PE managers need to find a home for the billions they’ve raised. It appears some private buyers are beginning to take us up on the offer; two of our UK companies have already been taken private at a 40%+ premium this year.

For investors who don't want to pay “2 and 20” in order to buy companies at a 40% premium, we have a portfolio of 49 European deep value stocks that are cheap (6.5x EV/EBITDA), levered (50% Debt/EV), and paying down debt. Since price and return are related, we believe these public companies should earn higher returns in the stock market than their private counterparts, valued at 9.4x EV/EBITDA.

Figure 4: Characteristics of Verdad Europe

Sources: Capital IQ and Verdad research (November 2019).