Emerging Markets: Slow Growth, High Volatility

This is part 1 of a series on emerging market crises. To download our full 55-page report, please click on the link at the bottom of this research note.

In a 2010 interview with USA Today, Mohammed El-Erian, the former CEO of Harvard Management Company and a notorious emerging markets bull, declared confidently that the world was on the precipice of a “global realignment.” This realignment, he declared, was “accelerating the migration of growth and wealth dynamics from the industrial world to the larger emerging economies.”

At the time, most pundits and investors, particularly those in the developed world, accepted El-Erian’s position as common knowledge. After all, they reasoned, globalized trade policies and an increasingly interconnected world naturally shifted capital away from boring, first-world financial centers and toward new, exciting economies like China, Brazil, and Indonesia. To take advantage of this obvious trend, wealthy investors poured money into emerging market ETFs and mutual funds throughout the late 2000s—in their mind, providing capital that would accelerate the inevitable, hockey-stick growth bound to appear in emerging economies.

It never happened. Perhaps we have experienced some sort of global realignment in the last decade, as El-Erian predicted, but that realignment never translated into equity returns—the buy-and-hold EM investors have never experienced the above-market growth about which they were so confident. The graph below shows MSCI’s Emerging Market Index returns since August, 2010, the month of El-Erian’s interview, plotted against the S&P 500. We believe that EM investors would have been far better suited in traditional, developed economies. In fact, $100 invested in the emerging market index in 2010 would net a measly $47 profit today, compared to a $383 profit from the S&P 500 index.

Figure 1: Returns in Emerging Markets vs. S&P 500 Since El-Erian’s Interview

Source: Capital IQ

This underperformance—and the boosterism of the proponents of this asset class—is far from a recent phenomenon. In their 1995 report, “Trends in Developing Economies,” the World Bank declared “growth in developing country stock markets will be enhanced as policies liberalizing trade and investment regulations, realigning exchange rates, consolidating public finances, and continuing with privatization are implemented.” As with El-Erian, the World Bank’s prediction may indeed have come to pass, as today’s global economy features liberal trade policies, investment deregulation, and aligned exchange rates. But in a key sense, we noticed that the World Bank was wrong: these changes did not drive equity returns. The graph below plots EM equity returns against the S&P 500 since July 1995, the month of the World Bank report.

Figure 2: Returns in Emerging Markets vs. S&P 500 Since the World Bank Report

Source: Capital IQ

Moreover, these EM equities underperformed their developed market equivalent despite a higher historic GDP growth. According to the IMF, the average annual GDP growth in emerging economies was 4.7% versus 1.8% for developed economies from 1989-2020. (See Appendix Figure 5).

The disappointing results for EM equity investors were even worse for investors who specifically sought to invest in EM growth stocks, which, in theory, should have benefitted the most from the sort of realignment El-Erian and the World Bank described. These stocks were in fact the major cause of EM underperformance, we believe, as EM value stocks delivered returns on par with the S&P 500.

Figure 3: US and EM Equity Performance Indicators, 1989–2020

Source: Capital IQ, Ken French Data Library

$100 invested in EM growth stocks in 1989 would have been worth less than half of the same investment in the S&P 500 or in EM value stocks.

Taken together, these insights paint a bleak picture for EM equity investing over the past 30 years. Over this period, EM investors took on more risk for less reward, while being unable to capture the benefits of GDP growth in these economies.

The frequency and severity of EM crises help explain both slow growth and high volatility in EM equity indices. Since 1989, emerging economies have experienced significantly more crises than their developed counterparts, as measured by the percentage drawdown in their equity markets. Not only are these crises more frequent in emerging markets, they’re also more severe.

Figure 4: Number of Crises by Severity of Crisis, 1987–2020

Source: Global Financial Data

When crises occur in developed markets, investors respond with predictions of the apocalypse. Take, for example, Mad Money host Jim Cramer, who screamed on air in late 2007, “It is not the time to be an academic . . . we have an Armageddon!” Yet, these panicked investors succumb to Chicken Little Syndrome: they’ve been hit by an acorn and scream that the sky is falling. After all, an investor in New York or London, even in the midst of financial turmoil, never doubts that a government bond will safely store capital, that his political system is stable, or that water will continue to run from his faucet. Indeed, after every American crisis in the last century, market indices have experienced short-term pain and long-term rebound to even higher values.

The same is not true for an investor living in a developing country. When poorer markets enter times of crisis, there are few certainties. Perhaps a government will default on its debt, or, even more extreme, maybe war has uprooted an established political system. When poor countries enter these same financial crises, the question is not when, but whether, their economy will truly recover. Take, for example, the Philippines, a country which—alongside many others in the developing world—experienced a financial crisis in late 1997. The Philippines’ MSCI index, which tracks overall stock market performance, has never returned to its 1997 peak. In other words, when emerging markets enter crisis periods, some countries never recover.

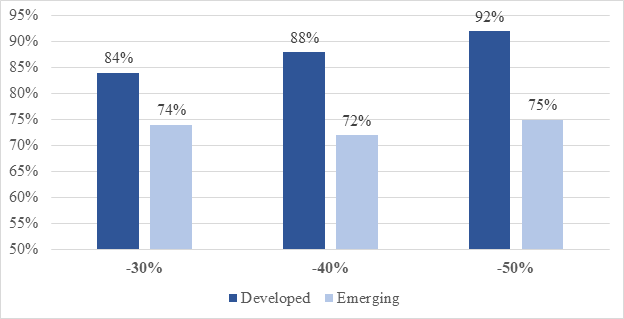

The graph below shows the probability of recovering to pre-crisis levels after 24 months by crisis severity, based on GFD equity data since 1987. For each crisis threshold, emerging economies are significantly less likely to recover, based on our research.

Figure 5: Historic Probability of Equity Recovery after 24 Months by Crisis Severity

Source: Global Financial Data

In his book The Volatility Machine, Michael Pettis delivers a compelling theory explaining both growth and crisis. Pettis proposes a model of economic growth that focuses on liquidity conditions in wealthy countries. Typically, we tend to think of capital flow from developed to emerging markets as a function of growth opportunities in poor countries. Pettis argues that the causality is precisely reversed. Instead, increased liquidity conditions in rich countries lead ambitious investors to make nontraditional emerging market bets. These bets, Pettis argues, drive growth in emerging economies. In this way, growth doesn’t attract investment; rather, investment causes growth.

That’s not to say that conditions internal to emerging markets don’t matter. In fact, it’s quite the opposite. Because EM growth is contingent on foreign investment, conditions internal to a developing country can scare rich investors, who subsequently remove their capital—triggering a financial crisis. Here, Pettis cites Mexico’s 1994 “Tequila Crisis,” a financial panic precipitated by the assassination of a popular presidential candidate. Emerging markets are more prone to these exogenous, market-moving events—political assassinations, tumultuous transfers of power, civil war—and when these events occur, central banks in the developing world often lack the global credibility to comfort wealthy investors. To make matters worse, a disproportionate number of investors in emerging markets are speculators with short time horizons. These investors are often unwilling to ride out a small loss, and their exit further exacerbates existing crises. These structural forces combine to generate more volatility in emerging markets.

Intense liquidity dependence and structural instability combine in emerging markets to generate immense volatility that magnifies both investor optimism and pessimism. In this sense, periods of growth become more lucrative—and periods of crisis become more disastrous. The figure below demonstrates this magnification of gains and losses, showing that emerging markets generally have underperformed the S&P 500 in contractionary environments and outperformed in growth environments.

Figure 6: Boom-Bust Growth in Emerging Markets vs. S&P 500

Source: Capital IQ

If—as Pettis’s research suggests—liquidity plays a more important role in emerging markets than in their developed counterparts, investors should be duly compensated for the value of the cash that they provide. At the same time, it seems that the value of this cash diminishes when a plenitude of investors dabble in EM investment.

But this theory of crisis investing in emerging markets is not the result of Pettis’s book alone. Through the lens of economic development studies, he was exploring something the finance community had already become obsessed with: the relationship between stock market liquidity shocks and associated asset price returns.

It has been well acknowledged in quantitative finance since the 1980s that (all else being equal):

Illiquid assets generally trade at lower prices on the basis of their expected cash flows compared to more liquid assets.

In times of scarce liquidity, investors flee from illiquid assets and toward more liquid safe havens.

The value factor has dramatically outperformed in post-crisis recovery periods globally as well as in emerging markets.

Investors who were present to take the other side of these trades were historically rewarded handsomely, beyond what we can explain using other fundamental risk factors.

The last 20 years of quantitative finance literature have also highlighted that the premium paid to this “contra-flight-to-liquidity” trade was strongest in emerging markets, especially during global liquidity shocks. And researchers have found that these premia are not eliminated by transaction costs or slippage alone (see Appendix Section D for the literature review).

However, few attempts have been made to bridge the gap between academic theory and practical, executable strategies that align with the evidence. What works on paper hasn’t yet been put to work on Wall Street today. We hope our focus here bridges that gap.