Diversification or Di-worse-ification?

How many stocks are required for a diversified portfolio?

When it comes to diversification of an equity portfolio, the conventional wisdom seems to be that 15-20 stocks can provide ~90% diversification relative to the market index. In his 1962 annual shareholder letter, Warren Buffett cited only needing 15-20 positions for adequate diversification. Today, the CFA Institute preaches the diminishing marginal improvements to portfolio diversification beyond 15 stocks, and CNBC pundit Jim Cramer advocates for an even more limited 5-10 stocks. A new word, “di-worse-ification” was even coined as an admonishment against the sin of owning too many stocks in pursuit of eliminating unsystematic risk. But where did this number come from, how did it come to be generally accepted wisdom, and is 15-20 stocks truly sufficient?

The original and oft-cited source was a 1968 paper by John Evans and Stephen Archer titled “Diversification and the Reduction of Dispersion: An Empirical Analysis”. In the paper, Evans and Archer simulated returns of a portfolio containing n stocks from 1958 to 1967 and calculated the standard deviation of each portfolio. The paper concluded that “the results raise doubts concerning the economic justification of increasing portfolio sizes beyond 10 or so securities.” This conclusion has been debated in academic literature (Statman 1987, Domian & Racine 2006, Surz & Price 2000), but none of these papers have received comparable attention.

In testing the Evans and Archer conclusion, we performed a similar analysis from 1995 to 2022 with 1000 simulations of portfolios comprised of n stocks. The results of our simulations are shown below in Figure 1.

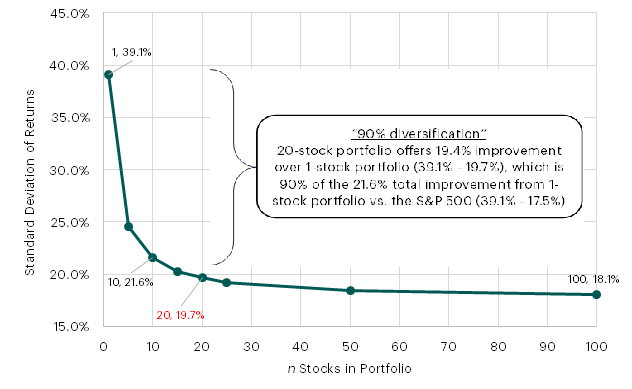

Figure 1: Standard Deviation of Simulated Portfolios with n Stocks

Source: Capital IQ, Verdad research

To us, this chart shows that a portfolio of 10, 15, or 20 stocks was significantly more volatile than the market. If the objective is to reduce systematic risk within a portfolio, or reduce tracking error, we believe a 10-stock portfolio falls short of these goals. From the chart above we can see that the S&P 500 has a standard deviation of 17.5%, and the 10-stock portfolio has a standard deviation of 21.6%. If the S&P 500 had a -1.5 standard deviation return (-26.25%), we could expect a 10-stock portfolio to return -32.5% (-1.5 standard deviation). The difference in these returns is much greater than we might expect from a “90% market diversified” portfolio.

When looking at the Evans and Archer paper, we noticed they define percentage diversification as the improvement between a one-stock portfolio and the market portfolio. As outlined in Figure 2 below, we can see that by this definition, a 20-stock portfolio does indeed achieve 90% of the potential diversification benefits of going from a 1-stock portfolio to a 500-stock (market) portfolio. However, a 20-stock portfolio is still considerably more volatile than the market.

Figure 2: The “90% Diversification” Referenced by Evans and Archer

Source: Capital IQ, Verdad research

Instead of standard deviation, we believe two more useful metrics would be R2 and tracking error, as suggested by Surz and Price. R2 measures the percent of portfolio variance that is explained by the market, and tracking error measures the standard deviation of the difference between portfolio and market returns.

As shown below in Figure 3, a 20-stock portfolio does achieve a 90% reduction in standard deviation relative to a one-stock portfolio, but falls short in both R2 and tracking error. An R2 of 0.75 would imply that the market can only explain 75% of the variation in portfolio returns, and a tracking error of 10.4% would be a failing grade for an index fund, in our opinion. Visually, the color gradient shows that standard deviation (the metric used by Evans and Archer) decreases faster than tracking error and R2 change as n increases.

Figure 3: Risk and Diversification Measures of Simulated Portfolios with n Stocks

Source: Capital IQ, Verdad research

If the goal is to construct a portfolio with an R2 of 0.90, where 90% of the variation could be attributed to the market, we believe a portfolio would need ~75 stocks, considerably more than advocated by Evans and Archer or preached by today’s financial luminaries. In fact, direct indexing solutions that track the S&P 500 tend to use about 350-400 stocks in trying to match index performance.

It’s worth noting that any strategy that attempts to beat the market will, by definition, need to have a tracking error greater than 0. One way this could potentially be achieved is with a very concentrated (10- to 20-stock) portfolio, as employed by many actively managed hedge funds. Another way could potentially be through a quantitative approach that seeks to capture factor premia while diversifying away unsystematic risk through larger portfolios.

Either way, if the objective is to eliminate or reduce unsystematic risk, we believe the 15-20 stock portfolio heuristic is probably too low and could leave investors with more volatile portfolios than expected.