Discounting, Death, and the Demand for Growth Stocks

Why are some stocks so expensive? Do low interest rates and rosy growth projections justify today’s historic growth-stock highs?

By: Verdad Research & Kaledora Kiernan-Linn

One of the most popular arguments used to justify the extreme divergence in growth stock valuations over the past years is that lower interest and discount rates make growth more valuable. Free money and lower “risk-free” rates should, in theory, increase the present value of riskier assets like stocks, and do so disproportionately for stocks that have higher long-term growth expectations.

And it’s trendy today in part because the relative valuations of growth stocks reached the 100th percentile of market history at the same time as the cost of cash hit the cheapest in market history.

Figure 1: Interest Rates and Extreme Growth Stock Cash Flow Multiples

Source: FRED for interest rates, Ken French Library for price-to-cash-flow multiples on the extreme 95th percentile breakpoint of all stock valuations in the US market each June.

This simple argument is theoretically very true in terms of the most basic valuation proposition used in asset pricing: the value of an asset is worth the sum of its discounted future cash flows in perpetuity. The most popular application of this asset pricing model is the discounted cash flow (DCF) method, which hinges on two key factors: r (the discount rate) and g (a company’s long-term growth rate). Under the model, valuations are extremely sensitive to small changes in projected discount and growth rates.

Consider, for instance, a company with free cash flow of $1 today, and assume a growth rate of 2% and a discount rate of 5% into perpetuity. Under these conditions, the present value of the firm is $34. A two–percentage point decrease in the discount rate, however, from 5% to 3%, results in a tripling of the enterprise value to $102. Valuations increase exponentially as r and g converge.

Figure 2: Two–Percentage Point Decrease in Discount Rate Triples Price

Note: images cropped for fit; (t) runs 10 years in this model.

This dramatic increase in firm value is almost exclusively due to an increase in the company’s estimated terminal value after 10 years, rather than its cash flows over the next 10 years. This has important implications. Because growth stocks are so disproportionately prized for their future, rather than current, performance, any change in their estimated future performance has an outsized effect on their valuations.

Figure 3: Terminal Period Weight Given Long-Term Growth and Discounting

Source: Verdad Analysis

The combination of low discount rates and high projected growth is a particularly dangerous cocktail: as r and g converge, nearly 100% of the company’s value is based on far-off speculation 10+ years in the future.

This simple model suggests that basic assumptions about future high growth and future low interest rates can explain today’s high prices. Yet the resulting growth multiples are an extreme bet, and almost 100% predicated on what happens beyond the next 10 years.

But it’s not just that forecasts of r and g beyond the near-term future (when it matters in the formula) are likely completely speculative that makes this logic dangerous. Investors are focusing too much on terminal values and not enough on termination rates. Long-term studies show that a substantial percentage of public companies don’t survive for 10 years.

Termination Rates Matter as Much as Terminal Values

If history is any guide, 10 years from now, among seasoned (i.e., not recently IPO-ed) firms, approximately 1.4% of large firms and 19% of small firms will have died a bad death, according to research from Fama and French that matches other long-term studies.

Figure 4: 10-Year De-Listing for Cause Rates for Seasoned Firms

Source: Fama & French

While large stocks de-list for cause infrequently, a fifth of small stocks are de-listed for bad reasons within 10 years (this excludes M&A). We demonstrated earlier that firms with high projected growth in a low interest rate environment have 90%+ of their valuation in this terminal period. For a fifth of small stocks, that value should in reality have been zero.

This is actual risk, and not the proxy for risk based on trailing stock price volatility typically used by bankers and the buyside alike when relying on “Beta” and “WACC” for a discount rate. And, interestingly, this difference in survival rates has historically been priced into markets, with small stocks trading between 15% and 30% below the valuations of large stocks quite consistently, based on our research.

Figure 5: Historical Discount for Small vs. Large Stocks

Source: Capital IQ. All North American Stocks.

The market is, therefore, accurately pricing in the relative risk of small caps relative to large caps: small stocks (in general) have higher termination rates and trade at lower valuations as a result, as we’ve observed. To see where markets perhaps may have gotten things wrong historically under this framework, we need an example of markets paying more to take on more risk…to the world of small growth stocks.

Small Growth vs. Small Value: Do the Valuations Make Sense?

Many may think that growth stocks should survive more often given their more exciting futures compared to value stocks. We associate distress with shrinking firms in outdated and struggling industries. But, in fact, the major study on distress risk predictors among growth and value stocks found that high revenue growth rates and high stock price returns have not historically mitigated that mortality risk. According to the study, growth stocks with blazing trailing returns historically outnumbered value stocks with poor trailing returns in mortality rates.

Indeed, Fama and French argued that, historically, the percentage of IPOs that survive 10 years is strongly predicted by the percentage of those firms that are “low-profitability, high-growth firms” with the probability of a new list surviving its first 10 years falling from “60.6% for the cohort of 1973 to 46.9% for the 1991 cohort.”

But although the market has generally priced the difference between large and small companies correctly, we’ve noticed that it has often gotten the mortality discount wrong when it comes to small growth stocks.

Figure 6: Premium (Discount) for Small vs. Large Growth and Small vs. Large Value

Source: Ken French Library. Small value multiple divided by large value multiple, and small growth multiple divided by large growth multiple. Note: small growth has not typically traded at the discounts we see today and those implied by small-firm failure rates.

This is the opposite of what the survivorship rates would suggest. If greater faith is placed in the future value of growth stocks, and this future value fails to materialize in a significant proportion of cases, then failure-prone, high-expectation stocks should be discounted quite severely. Historically, this has not been the case for small growth pricing.

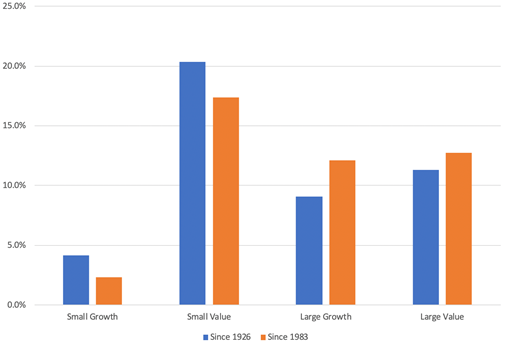

This is one possible explanation for the astonishingly dismal performance of small growth. Since 1983 (when small growth traded at its highest premium to large growth), small growth has grown at a compounded annual growth rate of 2.3%, far less than large growth’s 12.1% and certainly less than small value’s 17.3%. Over the long haul, small growth returned approximately half of what large growth did.

Figure 7: Compound Annual Growth Rates (CAGR) for Factor Portfolios

Source: Ken French Library

Taken together, these data suggest that, while markets do factor in survivorship, they are overly rosy in their appraisal of small growth and pessimistic in their appraisal of small value. Survivorship rates should matter as much, if not more, to the valuation of small growth stocks; especially in a low rate environment where discounted valuations are most predicated on long-term survival.

In the current low interest rate environment, where implied terminal values are high, markets do appear to have better factored reduced survivorship into the relative values of growth stocks than the graphs above show. Today’s -16% discount applied to small growth stocks (as compared to -20% for small value) closely resembles the historical survivorship rates found by Fama and French.

We believe current relative discounts within growth are at a more reasonable level, even if one doesn’t think growth’s sky-high absolute valuations are reasonable.

To assess if the absolute valuations of growth stocks are reasonable under the perpetuity theory, we can only echo Yogi Berra: “In theory there is no difference between theory and practice. But, in practice, there is.” The practice of assigning dramatically higher valuations to growth stocks relative to value stocks under long-term assumptions about r and g in perpetuity has produced some of the worst relative return results in the history of markets. It likely overestimates the long-term stability of g, underestimates the long-term survival risk for small growth stocks, and underestimates the impact of higher purchase multiples on long-term return prospects.

Being at zero rates today would not mitigate these estimation errors, but rather magnify their consequences—and quite dramatically, if the formula is the rationalization. Even in theory, it makes less sense to us going forward, as there is now little hope of a future tailwind for growth returns from multiple expansion through further rate drops past today's zero bound. In Japan, this bet didn’t work. In the 20 years since Japan instituted its zero interest rate policy, large growth has by far performed the worst, returning 0.8% versus small value’s 7.1% on an annualized basis.

In conclusion, we think this discounting theory may help explain why growth stocks have gotten so expensive. And while these arguments may help to explain today’s sky-high valuations, they may yet be useless or tragically counterproductive to forecasting future prices, if thought of as a forward-looking “justification” for current valuations. To the extent this is the rationalization, it is a big, big bet that is 90%+ dependent upon assumptions about what the 2030s and 2040s will look like for r and g.

Acknowledgment: Kaledora Kiernan-Linn is a rising junior in Neuroscience and Economics at Harvard College. Prior to her studies, she spent five years as a professional ballerina with the Royal Danish Ballet. She loves neurobiology, financial history, moral psychology, and is interested in pursuing a career in biotech and/or investing. If you would like to connect with Kaledora, please reach out.